If you want a textbook example in when to buy and sell retail names, check out TBL. Sometimes the best call is to do nothing.

The Timberland quarter is such a great lesson for anyone who cares about any company touching the retail supply chain. While we love to dig into the nitty gritty details more than anyone, sometimes you simply need to look at the calendar, a stock chart, and understand the motivational drivers behind what makes the company tick. This is one of those instances.

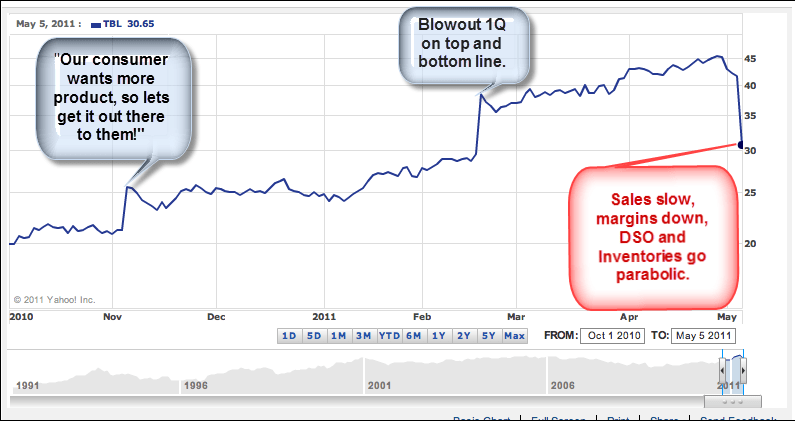

Specifically, recall that on the company’s 2Q conference call, CEO Schwartz altered the revenue strategy for the company. After years of pulling distribution (voluntary and involuntary) of its classic ‘yellow boot’ business, and then restricting distribution further as it tiered product to build demand under Gene McCarthy (who now heads UnderArmour’s footwear business), he said something to the tune of “our consumer wants our product, so we’re going to give them the product!!!” The triple exclaimation point there is to try to capture his tone, which was more cocky than it was aggressive. The market liked it, and the stock popped 20% in a week.

Then when TBL printed 4Q results, it blew away growth expectations. The stock was up another 25% in just 2 sessions.

But today’s results resulted not only in a miss, but in a flat-out horrible earnings/cash flow algorithm. Revenue growth of 10% was de-levered to operating profit decline of -29% with receivables and inventories up 13% and 37% (!), respectively. We won’t debate the company’s assertion that this is needed to hit their growth plans, but we will question the margins that will be realized to achieve such growth.

Simply put, this is just a great case of management behaving badly.

I’ll be the first to admit how I kicked myself for missing that positive move in the stock on that mid-February day. But I’d have kicked myself harder for participating in the “capital destruction gong show” that was TBL’s 1Q.

Yes, we want to be right all the time. Every quarter, every month, and every day. But sometimes the best strategy is to sit back, stick to your guns, and do nothing.

This is the gnarliest looking SIGMA we've seen all year.Let us know if you need help interpreting.