1Q11 is proving to be a strong quarter for the pizza category. DPZ reported $0.42 versus consensus $0.34. Domestic comparable restaurant sales slowed -1.4% versus street expectations for a -4% print versus last year’s blowout first quarter. Domestic company and franchise comparable sales slowed -2.3% and -1.3% versus consensus at -4.3% and -3.9%, respectively. International comparable restaurant sales grew 8.3% versus consensus 6.5%.

Management shirked away from providing guidance, reverting back to their normal practice after providing sales commentary on 1Q during the 4Q10 Earnings Call. Management’s discussion, if a little light on forward-looking details, certainly seemed positive in tone. The domestic and international businesses are performing well and management is “comfortable” with the +3-5% commodity cost outlook. Given that inflation in 1Q11 was 5%, the higher end of the range seems more conservative.

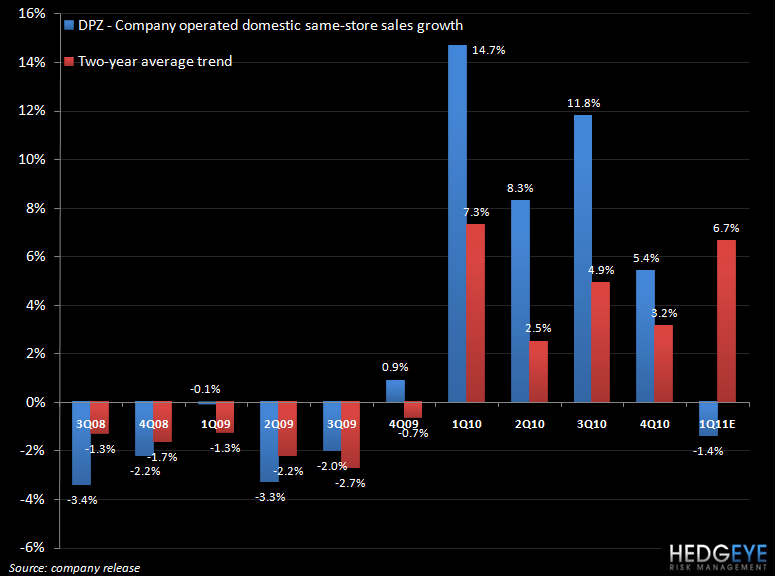

Comparable-restaurant sales growth

The chart of company-operated domestic same-store sales below shows clearly that DPZ’s domestic business is trending very well. Despite a negative comparable-restaurant sales number for the first quarter, the two-year average trend is encouraging. On a sequential basis, from 4Q10, two-year average trends accelerated by 350 basis points. Media spending in the quarter was in line with the one year ago and the last few quarters, and management stressed that media spend should remain at a fairly constant level for the foreseeable future.

International markets are providing robust returns for the company with Turkey (promotions and TV) and Malaysia (new menu items) two of the standout markets. The company began its recap of the quarter with commentary on international markets so that, according to management, it might be highlighted that Domino’s is an international company that derives one-third of its profit from international operations.

By way of an explanation for the upside surprise in the company’s top-line performance, management reiterated its comments from a quarter ago; the company views its brand and equity as having been enhanced far past where it was pre-2010. The U.S. business continues to perform well as the company added pizza and chicken promotions to the menu during 1Q11. While management wouldn’t give specific numbers on the impact of chicken on average check, or what average check was during the quarter, it was explained that chicken was ordered with high frequency as an add-on, and did not cannibalize pizza sales, so we can infer, from a traffic and average check perspective, that the chicken promotion was a net positive. Chicken was only rolled out for the last 5 weeks of the quarter so the impact on the current quarter may be more significant.

Restaurant Operating Margins

Food costs are certainly rising for every company in the restaurant business, with the exception of BWLD, but DPZ is managing the challenge well. The structure of the company, being 90% franchised, is a great help in this regard but DPZ feels that inflation has been managed and the company’s supply chain system has put the company in a good position in terms of negotiating contacts. Commodities, according to the company, have been in line with their expectations. As I wrote in my note titled “DPZ – 1Q11 INFLATION COMMENTARY”, DPZ has been maintaining a far more realistic inflation outlook than many of its peers.

Cheese prices were a huge concern for DPZ at the time of the past earnings call on March 1st. Ten days later, cheese prices fell off a cliff and for the quarter, DPZ paid an average price of $1.60 per pound versus $1.44 last year. Considering that cheese was trading at $2.00 before its precipitous decline in mid-March, investors are far more at east at the present time than one quarter ago.

From here, I think this name has plenty of momentum. Some of the key reasons for my stance include: robust sales growth, a heavily franchised system, a supply chain business that benefits from higher commodity costs, and a management team that is managing investor expectations, as well as the business, very well.

Howard Penney

Managing Director