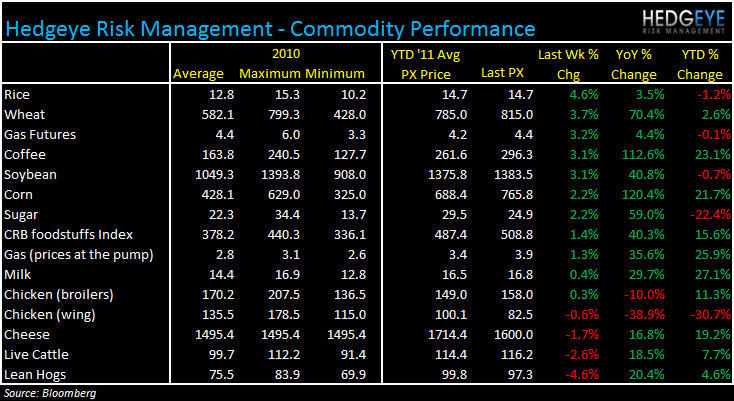

As the buck goes lower and lower, inflation is still an issue for consumers and corporations alike.

Commodities continue to be a key focus for management teams as they react to significant downticks in gross margins due to inflation. Some companies, in our view, are deciding to extend and pretend in the hope that the back half of the year presents a more favorable commodity environment where costs can be recouped. Last week we noted the poor performance of MCD and CAKE following their respective earnings releases.

This week, PNRA and TXRH are examples of companies that are moving their inflation targets higher in the face of rising food costs. As we wrote yesterday, BAGL, CBOU and CPKI are two companies that we believe will increase their inflation outlook over the next few days. Rice gained almost 5% over the last week but prices are up a mere 3.5% year-over-year. PFCB has its rice needs contracted for the year.

BWLD is currently escaping the effects of inflation and should continue to do so for the foreseeable future. Tellingly, excluding chicken wings and broilers, the commodities in our commodity monitor table are up an average of 44% versus last year while chicken wing prices are down 39% year-over-year.

Below, I call out a select few commodities and the respective week-over-week moves, alongside some additional company-specific commentary.

Wheat

Wheat is a commodity that is widely used in the restaurant space but generally does not take up a large percentage share of any one company’s basket, with the exception of PNRA. The pizza concepts generally play down the significance of wheat prices for their overall basket (DPZ have it hedged out for the year) but, clearly, for PNRA wheat is a big driver of margin. PNRA raised its inflation target to 5% for the second quarter and an average of 4% for the year, which is approximately 75 basis points higher than the full year estimate from the prior earnings call.

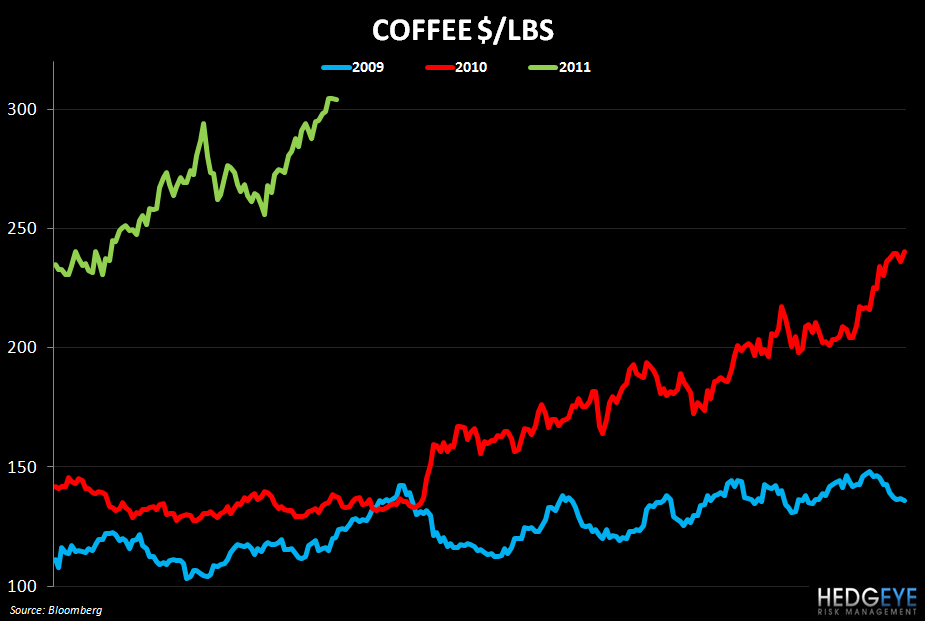

Coffee

Coffee is a commodity that is generating headlines. GMCR and PEET reported last night and PEET’s, in particular, had some interesting commentary on coffee inflation and the significant impact management expects on gross margin in the second quarter. PEET also raised its beverage prices by between $0.10 and $0.15 in retail stores.

Chicken wings

Chicken wings continue to March lower week-over-week. As I wrote earlier, BWLD is in a unique position as a restaurant company because its commodity costs are down 39% year-over-year. Excluding chicken wings and broilers, the commodities in our commodity monitor table are up an average of 44%.

Howard Penney

Managing Director