TODAY’S S&P 500 SET-UP - May 4, 2011

The mechanism driving most Correlation Risk across asset classes in the market remains the USD. So watching where the USD might stop crashing is a critical risk management exercise in play yesterday (USD flat on day = XLE (Energy stocks) down -2.5%; Brazil down -1.8%, etc…).

The Hedgeye immediate-term TRADE line of resistance in the USD developing at $73.52 – watching that very closely as resistance becoming support could easily trigger a much larger move in the hedge fund community’s largest net long position since 2007 - long the Inflation trade. As we look at today’s set up for the S&P 500, the range is 24 points or -0.56% downside to 1349 and 1.21% upside to 1373.

SECTOR AND GLOBAL PERFORMANCE

Yesterday, Energy broke the TRADE duration leaving 7/9 sectors broken on TRADE and 8/9 broken on TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -911 (-400)

- VOLUME: NYSE 1003.11 (+7.26%)

- VIX: 16.70 +4.44% YTD PERFORMANCE: -5.92%

- SPX PUT/CALL RATIO: 1.84 from 1.38 (+33.87%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 25.00 -0.200 (-0.794%)

- 3-MONTH T-BILL YIELD: 0.03% -0.02%

- 10-Year: 3.28 from 3.31

- YIELD CURVE: 2.67 from 2.70

MACRO DATA POINTS:

- Quarterly Treasury debt sales announcement

- 7 a.m.: MBA Mortgage Applications, prior (-5.6%)

- 7:30 a.m.: Challenger job cuts, prior (-38.6%)

- 8:15 a.m.: ADP employment, est. 198k, prior 201k

- 10 a.m.: ISM non-manufacturing, est. 57.5, prior 57.3

- 10:30 a.m.: DoE inventories

- 3:30 p.m.: SF Fed President John Williams makes first policy speech

- 4 p.m.: Fed’s Fisher speaks in New Mexico

- 4:15 p.m.: Geithner speech on economy in Washington

- 7 p.m.: Fed’s Lockhart speaks in Atlanta

WHAT TO WATCH:

- Treasury Secretary Tim Geithner speaks in Washington on the economy.

- Conagra makes a $86/share cash bid for Ralcorp for a takeover that would acquire $2.5b of debt.

- Applied Materials agrees to buy Varian Semi for 55% premium at $63/share.

- Richard Branson says no deadline for decision on whether to sell airline.

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Silver Slumps on Higher Margins; Gold Drops on Report of Soros Fund Sales

- Rice May Drop on ‘Abundant’ Thai Supply, Aiding World’s Poor as Corn Gains

- Cocoa Poised to Tumble as Maersk Cargo Signals Price Peak: Freight Markets

- Glencore Seeks $61 Billion Value in London, Hong Kong Initial Share Offer

- Crude Oil Halts Two-Day Decline in London Before U.S. Employment Report

- Copper Drops to Seven-Week Low on Concern China May Tighten Credit Further

- Corn, Soybeans Drop for a Third Day as Price Rallies May Cut Into Demand

- Sugar Falls for a Fifth Day on Thai Output, China Inflation; Coffee Drops

- Cash-Copper Premium in China Signals Demand May Increase: Chart of the Day

- Gasoline ‘Bubble’ May Grow Past 2008 Record on Supply Drop: Energy Markets

- Palm Oil Drops to Two-Week Low as Demand for Soybeans Weakens, Crude Falls

- Coal Stocks ‘Alarming Low’ in China, ‘Critical’ in India: Chart of the Day

- Cocoa Arrivals From Bahia Boost Brazilian Production to Most in 16 Years

CURRENCIES

EUROPEAN MARKETS

- Euro approaches 18-month high versus dollar before interest-rate decision

- Portugal financial rescue medicine may be just a first taste - euro credit

- German 2-year notes drop on ECB tightening bets; Portuguese bonds advance

- Spain’s thousands of illegal homes sour development minister’s sales pitch

- BMW profit advances more than estimated on demand for 5-series, x3 models

- new deutsche bank CEO turns on Krause vying with Weber for power with Jain

- European stocks fluctuate; Holcim drops while shares of Actelion advance

- Europe retail sales drop most in 11 months on rising oil, government cuts

- UK house prices drop for first time in three months as cuts deter buyers

- UK Mar mortgage approvals 47.6k vs consensus 48.0k and prior revised to 46.7k from 47.0k

- Uk Apr Construction PMI 53.3 vs consensus 55.5 and prior 56.4

- Eurozone April Services PMI 56.7 vs consensus 56.9 and prior 56.9

- Germany April Services PMI 56.8 vs consensus 57.7 and prior 57.7

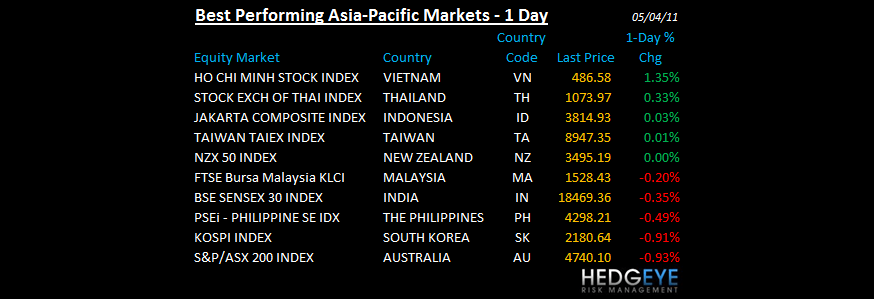

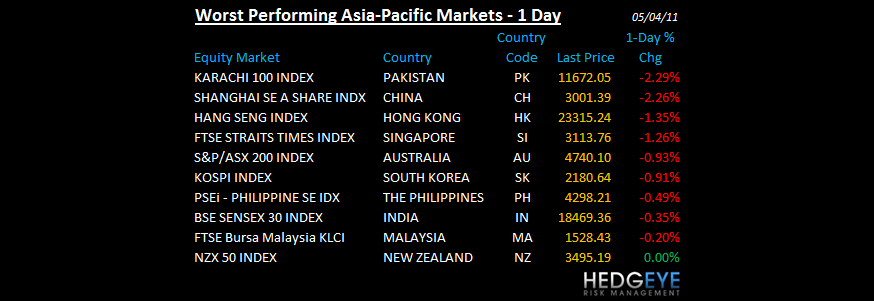

ASIA MARKETS

- China and Hong Kong fell on fears of further monetary tightening in china.

- Most Asian stocks decline as raw material producers, Australian banks retreat

- Hong Kong home sales fall to two-year low on government curbs, loan rates

- Shinhan profit little changed as Korea property slump drives up bad loans

- Vietnam raises repurchase rate for fifth time this year in inflation fight

- Philippines, Malaysia will consider rate rises as oil fuels Asia inflation

- Asia seeks to boost use of local currencies in trade, reduce dollar’s role.

- Japan was closed for Greenery Day and will remain closed until 6-May.

MIDDLE EAST

Howard Penney

Managing Director