TODAY’S S&P 500 SET-UP - May 3, 2011

While it’s proactively predictable to see Geithner politic his way around our “reported” fiscal position, even for him this is impressive. The Republicans were allegedly waiting until mid-May to put the Democrats feet to the fire on the debt ceiling debate. The US Currency Crash is starting to price this in. As we look at today’s set up for the S&P 500, the range is 33 points or -1.27% downside to 1344 and 1.16% upside to 1377.

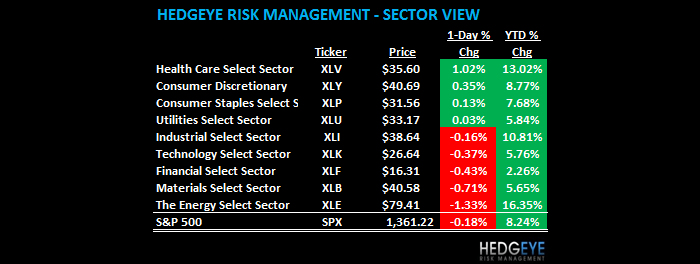

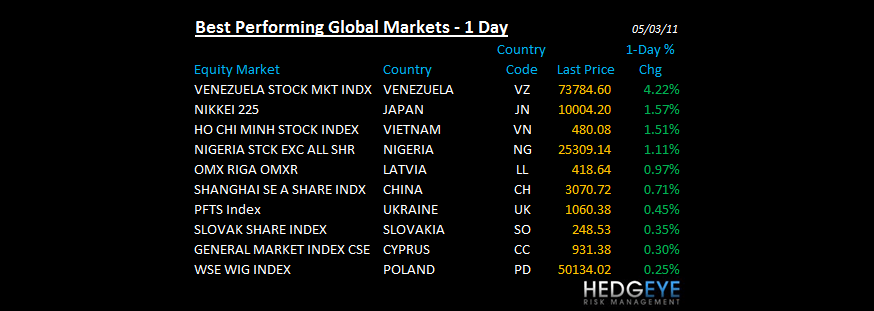

SECTOR AND GLOBAL PERFORMANCE

The Financials remain the only sector broken on both TRADE and TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -511 (-1428)

- VOLUME: NYSE 935.18 (-4.11%)

- VIX: 15.99 +8.41% YTD PERFORMANCE: -9.92%

- SPX PUT/CALL RATIO: 1.38 from 1.75 (-21.37%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 23.75 -0.507 (-2.090%)

- 3-MONTH T-BILL YIELD: 0.05% +0.01%

- 10-Year: 3.31 from 3.32

- YIELD CURVE: 2.70 from 2.71

MACRO DATA POINTS:

- 8:30 a.m.: Fed’s Hoenig speaks to bankers in Washington

- 10 a.m.: Factory orders, est. 2.0%, prior (-0.1%)

- 11:30 a.m.: U.S. to sell $24b 52-wk bills, $28b 4-wk bills

- 4 p.m.: Treasury’s Geithner at U.S.-China Business Council

- 4:30 p.m.: API inventories

WHAT TO WATCH:

- Renren, China’s biggest social-networking website by page views, aims to raise as much as $743.4m in U.S. IPO

- Greek Finance Minister Says Debt Restructure ‘Huge Mistake’ - Finance Minister George Papaconstantinou said a restructuring of Greece’s debt, causing losses for bondholders, would lock the country out of markets for a decade or more.

- Canada’s dollar rose, stocks and bonds may rally after Conservative Prime Minister Stephen Harper won a majority government for first time.

- Goldman Sachs Lloyd Blankfein likely to remain CEO for at least two years - NY Post

- US steel companies using price escalator clauses in longer-term contracts - WSJ

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Gold, Silver Advance as Signs of Inflation Spur Increased Investor Demand

- Oil Drops on Economic Growth Concern as Bin Laden Death Boosts Volatility

- Copper in London Declines for Fourth Day on China, U.S. Manufacturing Data

- Soybeans Drop For a Second Day as Favorable Weather May Aid U.S. Planting

- Sugar Falls to Seven-Month Low on Thai Production; Cocoa Prices Decline

- S. Korea to Boost Tarriff-Free Pork Imports After Foot-and-Mouth Outbreak

- Dodd-Frank Rules on Swaps and Ratings Targeted by U.S. House Republicans

- Rail Access to Australia’s Fremantle Port Is Cut After Accident, ABC Says

- Palm Oil Advances as Gain in Malaysian Exports May Curb Inventory Build-up

CURRENCIES

EUROPEAN MARKETS

- European equity markets opened mixed before drifting lower in choppy trading.

- UK Apr Manufacturing PMI 54.6 vs consensus 56.9; now at a 7 month low

- EuroZone Mar PPI +6.7% y/y vs consensus +6.6% and prior +6.6%; EuroZone Mar PPI +0.7% m/m vs consensus +0.6% and prior +0.8%

ASIA-PACIFIC MARKETS

- Australia keeps main cash rate unchanged at 4.75%

- India’s central bank raised benchmark interest rates by a more-than-estimated 0.5 percentage point after forecasting inflation will stay at an “elevated level” until at least September - Bloomberg.

- China Home Prices Rise; Wen ‘Determined’ to Lower Them - Bloomberg

- Japan was closed for Constitution Day and will remain closed until 6-May.

MIDDLE EAST

Howard Penney

Managing Director