TODAY’S S&P 500 SET-UP - April 29, 2011

As we look at today’s set up for the S&P 500, the range is 39 points or -1.88% downside to 1333 and 0.98% upside to 1377.

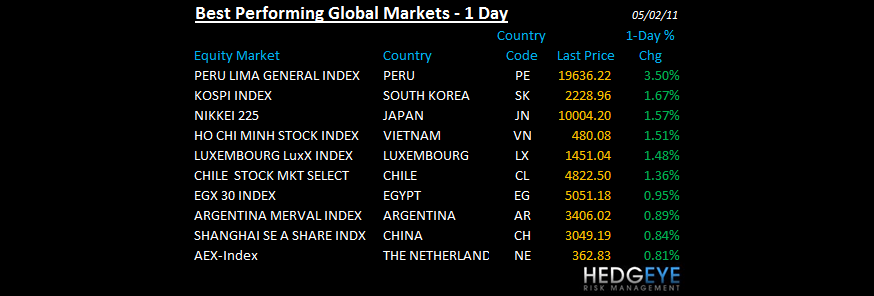

SECTOR AND GLOBAL PERFORMANCE

The Financials remain the only sector broken on both TRADE and TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 917 (+226)

- VOLUME: NYSE 975.24 (+1.43%)

- VIX: 14.75 0.89% YTD PERFORMANCE: -16.90%

- SPX PUT/CALL RATIO: 1.21 from 1.15 (+5.28%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 22.25

- 3-MONTH T-BILL YIELD: 0.06% -0.01%

- 10-Year: 3.39 from 3.34

- YIELD CURVE: 1.75 from 1.96

MACRO DATA POINTS:

- 10 a.m.: Construction spending, est. 0.4%, prior 1.4%

- 10 a.m.: ISM Manufacturing, est. 59.5, prior 61.2

- 11 a.m.: Export inspections: Corn, soybeans, wheat

- 11:30 a.m.: U.S. to sell $29b 3-mo. bills, $27b 6-mo. bills

- 4 p.m.: Crop progress: Winter wheat, cotton, corn

WHAT TO WATCH:

- India’s manufacturing grew at the fastest pace in five months and exports climbed to a record, increasing pressure on the central bank to raise interest rates

- Silver futures plunged as much as 13% after CME boosted margins

- Ralcorp said it received unsolicited takeover proposal in March, board determined wasn’t in best interest; CNBC reported Friday that ConAgra had expressed interest

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Oil Drops Most in Two Weeks After U.S. Says Bin Laden Killed in Pakistan

- Copper Declines to 7-Week Low as Chinese Manufacturing Declined in April

- Corn Slips as Dollar’s Gain Cuts Demand for Commodities as Store of Value

- India Said to Consider Ending Four-Year Ban on Wheat Exports on Stockpiles

- Rubber Falls as China’s Manufacturing Index Declines More Than Forecast

- South Korea Seeking to Boost Wheat, Soybean Production to Reduce Imports

- Commodities Beat Financial Assets for Fifth Month in Best Streak Since ’97

- Cocoa Bean Exports From Indonesia’s Sulawesi Slump as Sales Suffer Delays

- Korea Investment Corp. Buys Noble Group Stake to Partner in Infrastructure

- Funds Slash Bullish Sugar Bets to Two-Year Low as Thailand Supplies Climb

- Codelco Waning Copper Pressures $17.5 Billion Bet to Catch Boom for Metals

- Bolivia President Morales to Overturn Laws on Mining, Banking, Investments

CURRENCIES

EUROPEAN MARKETS

- European indices are trading higher a few hours after the announcement of Osama bin Laden's death.

- UK markets are closed for a bank holiday.

- Eurozone April final manufacturing PMI 58.0 vs consensus 57.7

- Germany April final manufacturing PMI 62.00 vs consensus 61.7

- France April Final Manufacturing PMI 57.5 vs consensus 56.9

ASIA PACIFIC MARKETS:

- Most Asian markets that were open rose today.

- China, Hong Kong, Taiwan, and Thailand were closed for Labour Day.

MIDDLE EAST

Howard Penney

Managing Director