TODAY’S S&P 500 SET-UP - April 29, 2011

As we look at today’s set up for the S&P 500, the range is 34 points or -1.99% downside to 1333 and 0.51% upside to 1367.

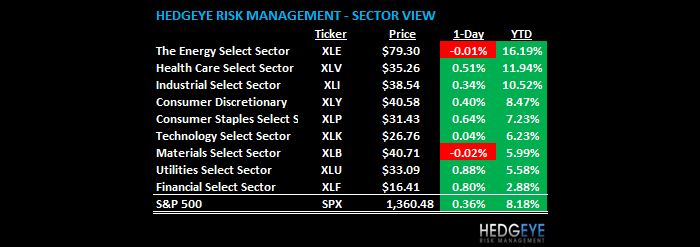

SECTOR AND GLOBAL PERFORMANCE

The Financials remain the only sector broken on both TRADE and TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 691 (-141)

- VOLUME: NYSE 961.53 (+0.06%)

- VIX: 14.37 -6.38% YTD PERFORMANCE: -19.04%

- SPX PUT/CALL RATIO: 1.21 from 1.15 (+5.28%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 22.25

- 3-MONTH T-BILL YIELD: 0.06% -0.01%

- 10-Year: 3.39 from 3.34

- YIELD CURVE: 1.96 from 1.21

MACRO DATA POINTS:

- 8:30 a.m.: Personal Income, est. 0.4%, prior 0.3%

- 8:30 a.m.: Personal Spending, est. 0.5%, prior 0.7%

- 8:40 a.m.: Fed’s Bullard to speak on community development in Virginia

- 9:45 a.m.: Chicago Purchasing Manager, est. 68.2, prior 70.6

- 9:55 a.m.: U Michigan Confidence, April final, est. 70.0, prior 69.6

- 10 a.m.: NAPM-Milwaukee, est 63.0, prior 66.0

- 12:30 p.m.: Bernanke speaks at Fed Community-Affairs Conference

- 1 p.m.: Baker Hughes rig count, prior 1800

WHAT TO WATCH:

- Russia Unexpectedly Raises Benchmark Interest Rate Quarter Point to 8.25%

- PPC facing at least $500 million in higher feed costs this year

- Berkshire Hathaway annual meeting this weekend

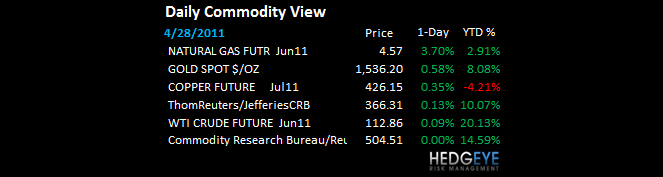

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Gold-Buying Central Banks May Signal Bullion Extending Record Price Rally

- Copper Futures in Shanghai Heading for Second Monthly Loss on China Curbs

- Gold Heads for Best Monthly Gain Since November 2009 on Inflation, Dollar

- Crude Oil Falls From Highest in 31 Months; Heads for Eighth Monthly Gain

- Coffee May Climb 40% on Brazil Frost Risk as Kraft, Smucker Raise Prices

- India Said to Consider Freeing Urea Price to Reduce Spending on Subsidies

- Corn Demand in China to Outstrip Supplies on Livestock Feed

- Naphtha’s Rally Not Over as Japan, Korean Demand Rebounds: Energy Markets

- Wheat Futures Gain as Rains in U.S. May Have Come Too Late for Harvests

- China May Face Power Shortages in Summer as Demand Beats Growth in Supply

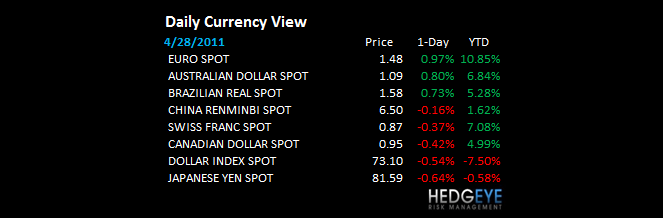

CURRENCIES

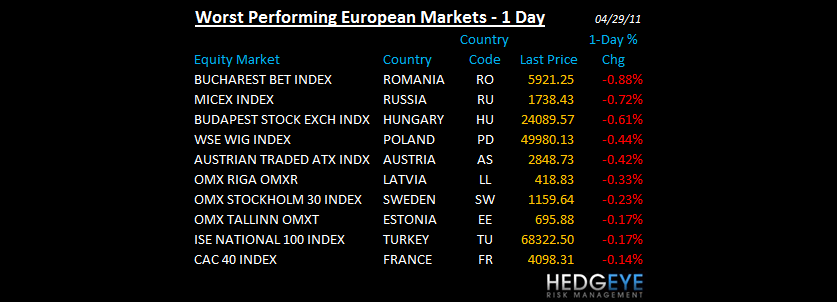

EUROPEAN MARKETS

- U.K. markets closed for the Royal Wedding. Also closed Monday

- Inflation Accelerates in Europe on Oil Surge as Business Confidence Wanes

- European Stocks Are Little Changed; Yara, SSAB Rise on Earnings, YIT Sinks

- Euro Zone April CPI 2.8% y/y vs 2.7% consensus

- France Mar PPI +6.6% y/y vs. consensus +6.4%

ASIA PACIFIC MARKTES:

- Asia stocks mixed as US economic growth slows

- Yuan strengthens to post-’93 high against dollar as China fights inflation

- Taiwan’s economy grows more-than-estimated 6.19%, adding pressure on rates

- Japan was closed for Showa day.

MIDDLE EAST

Howard Penney

Managing Director