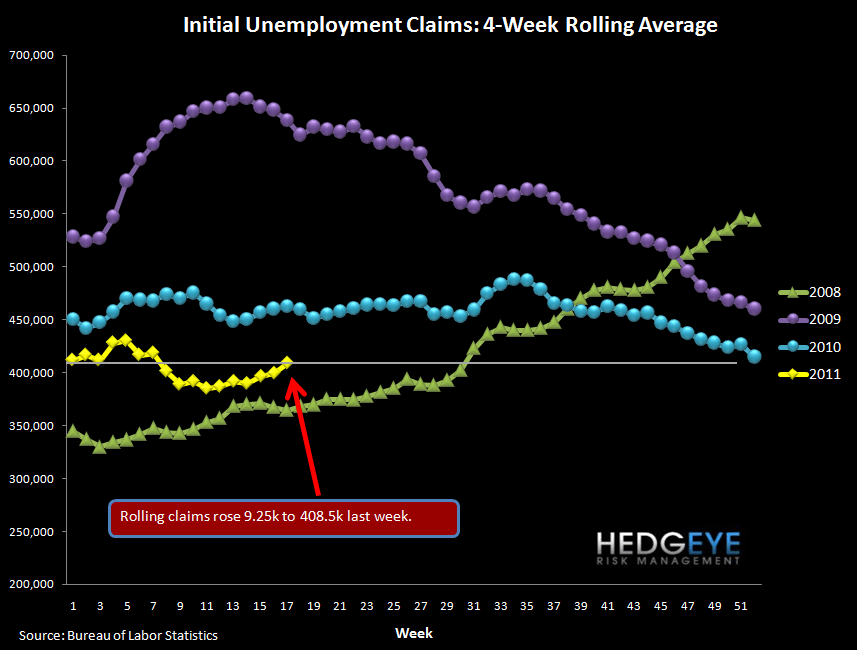

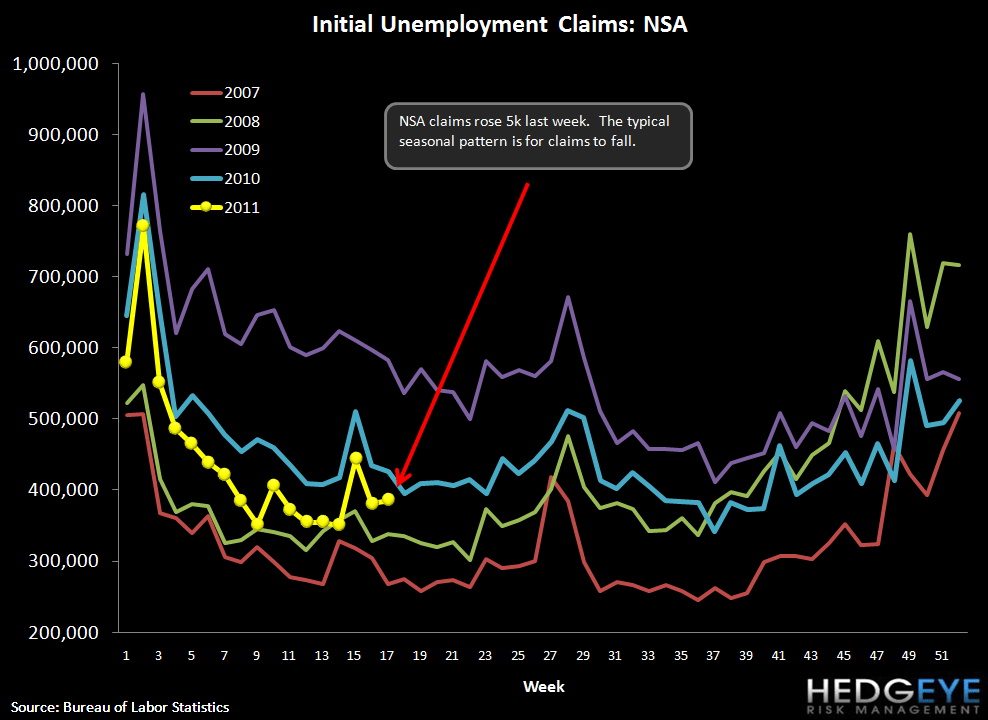

Initial Claims Rise 25k ... Give Back All YTD Improvement

The headline initial claims number rose 26k WoW to 429k (25k after a 1k upward revision to last week’s data). Rolling claims rose 9.25k, breaking up through the 400k line to 408k. Reported claims, which are volatile, are now at the same level they were in January 2010. Rolling claims are at the same level they were in January 2011, translating to no improvement in claims in the last four months. On a non-seasonally-adjusted basis, reported claims rose 5k WoW.

We consider rolling claims the best leading indicator for consumer-related loss frequency for lenders. A failure to realize further improvement in this series will put the brakes on ongoing credit improvement in credit card lending. Mortgage and auto lending are similarly affected. What troubles us is that claims are failing to improve in the midst of strong corporate earnings and ongoing QE2. While much of the rest of the market seems unconcerned about the end of QE2, we think it may lead to a cessation of improvement in claims based on the fact that we observed just that at the end of QE1.

Putting claims in context: we have been looking for claims in the 375-400k range as the level that can begin to bring unemployment down. If this level is held, we expect to see unemployment improve. We consider unemployment to be ~200 bps higher than the headline rate due to decreases in the labor force participation rate. In other words, if the labor force participation rate were at the long-term average level of the last decade, unemployment rate would be 10.8% rather than 8.8%. So when we say that claims of 375-400k will start to bring down the unemployment rate, we are actually referring to the 10.8% actual rate.

Two relationships that we are watching closely are the tight correlation between the S&P and claims and between Fed purchases (Treasuries & MBS) and claims. With the end of QE2 looming, to the extent that this relationship is causal, it is quite concerning.

Yield Curve Remains Wide

We chart the 2-10 spread as a proxy for NIM. Thus far the spread in 2Q is tracking 4 bps tighter than 1Q. The current level of 271 bps is 2 bps tighter than last week.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur