Brinker reported a great quarter this morning which exceeded consensus expectations. I think I have been one of, if not the most bullish analysts on this name yet Chili’s reported comps still beat my expectations also.

Brinker reported earnings this morning and reported diluted EPS of $0.46 came in slightly above consensus at $0.45. EPS from continuing items came in at $0.45 cents, 22% higher than 3QFY10. Chili’s company-owned same-store sales declined -0.7% during 1Q, on a calendar/53 week-adjusted basis. The reported comp was -0.3%. Consensus was anticipating a decline of -1.2%. At Maggiano’s, company-owned same-store sales grew +4.1% during 1Q, on a calendar/53 week-adjusted basis. The reported comp was +3.4%. Consensus was anticipating a print of +3.0%.

Guidance for 4QFY11 may have been somewhat of a disappointment, given that consensus is at the high end of the range, but looking past the fourth quarter, the direction of the business is positive.

Same-store sales

The improvement of same-store sales, relative to competitors in the casual dining space, was a key crux to my bullish thesis for Brinker and this quarter obviously further solidifies my confidence in the sustainability of the story. As the chart above shows, the trend in comps at Chili's – particularly when one looks at the two-year trend – is clearly pointing higher. Management has emphasized the importance of value and a high-quality guest experience for the health of the company’s top-line and, it seems, the customer is responding well to initiatives ranging from “Team Service”, improved speed of service thanks to food preparation initiatives, and new lunch menu items at affordable price-points.

The company highlighted the substantial impact on comps from the new line of combos on the lunch menu. While traffic at lunch moved from negative mid-single digits to positive, there was also an expected impact on mix resulting from a lower check. Preference for these $6/$7/$8 items were higher than anticipated based on test results and management said that it will continue to work to balance top-line growth and profitability. In my view, as the company continues what is ultimately a reintroduction of the new Chili’s to the casual diner, traffic growth is paramount so as to raise awareness of a much improving restaurant chain. When asked about the prospect of raising prices during the Q&A, the company reiterated its prioritization of traffic which, I believe, is the correct strategy for Chili’s at this point in time.

Besides the trend, merely comparing the language and tone of Brinker’s earnings call versus the earnings calls of peer companies that have reported of late underscores the progress Brinker is making. As I wrote in my restaurants earnings preview on Monday, Brinker would not point to gas prices as an excuse and that alone sets it apart for the earnings season so far.

Operating Margin

Restaurant operating margins grew 152 bps year-over-year. Cost of sales decreased 127 bps driven by a more profitable value offer in January and menu improvements. There was also a 50 basis point improvement due to a favorable impact from menu pricing and other items. Commodity costs were unfavorable in the quarter to the tune of 10 basis points. Labor improved 60 basis points in 1Q. Team service continues to perform well, contributing roughly 100 basis points in savings. 1Q included the first phase of the kitchen retrofit program which will optimize the labor component of food preparation. This should reduce labor costs and cost of sales through food waste reduction.

Reimaging program

The company estimates that the reimaged restaurants are seeing a lift of approximately 100 basis points from a margin perspective. Changes in the kitchen were rolled out late last quarter and it is expected that the impact of that will gain additional traction over time. In terms of the margin enhancements that are projected to come from the kitchen retro-fits, it will take time – perhaps into FY13 – for the benefit to flow through the system. The Oklahoma City reimage test has been encouraging for management and has prompted a move to expand the reimaging program to additional markets.

Share Repurchases/Capital Expenditure

During the 3QFY11, the company completed an additional $107 million share repurchase (4.5 million shares). Year-to-date, the company has spend $357 million on share repurchases (18 million shares). Total fiscal 2011 capital expenditure is expected to by approximately $80 million. Capex in 2012 is projected to be $170 million.

Outlook

- The company offered conservative EPS guidance of $0.43 to $0.47 but remains confident in doubling EPS in five years.

- From a commodity perspective, the company is currently 92% contracted through the end of the year. 4Q is expected to bring slightly unfavorable cost of sales. The company is 54% contracted through the end of calendar 2011 and anticipates roughly 100 basis points in commodity pressure for fiscal 2012.

- Beef remains the most significant inflationary pressure in EAT’s commodity basket. In August, the current contract expires and, if renewed at current prices, a new contract would likely involve a significant increase in inflation.

- The company is hoping to renew its chicken contract at a more favorable rate given deflationary pressures in the chicken market.

- Dairy costs are contracted and management believes that the company could expect favorability in fiscal 2012 if the contract was renewed.

Sentiment and Valuation

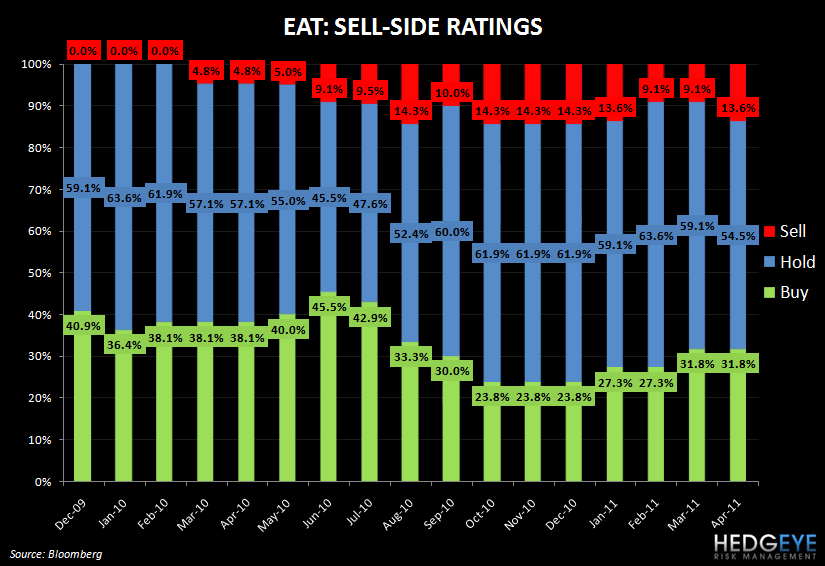

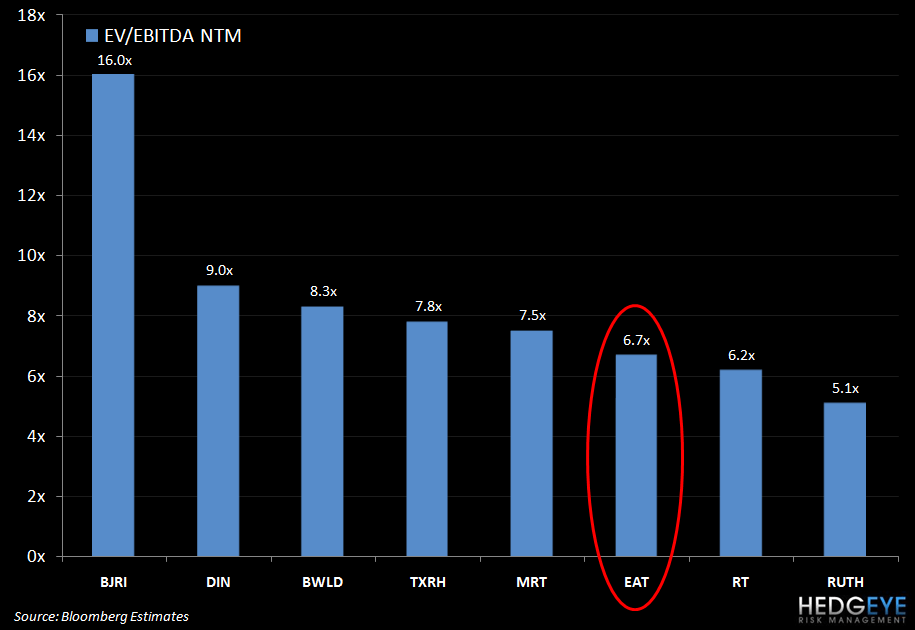

A conversation I had last year with Guy Constance comes to mind. “A badge of honor” is how he described the label of being the least favored casual dining company from a sentiment monitor I wrote in November (“EAT – A BADGE OF HONOR”, 11/14/11). Below, I am including a chart on sell side sentiment for Brinker. I expect this to change markedly in the coming quarters. From a valuation perspective, EAT remains attractive. At 6.7x EV/EBITDA NTM, I believe there is room for that multiple to expand.

Howard Penney

Managing Director