“The main question is where this movement will lead us.”

-F.A. Hayek

Today is his big day. Today is the 1st day in US economic history that the Almighty Central Planner of US Monetary Policy will hold a press conference with the media immediately following his decision to pander to the political wind. Currency Crashers and Yield Chasers, unite!

As Hayek predicted 70 years ago in “The Road To Serfdom” (which Keynes himself called “a grand book” that he agreed “morally” with), this is the long hard road towards socialism that traverses many political conflicts and compromises. Before you watch The Bernank today, take a step back and really think about how Big Government Intervention in our markets has become; you’ll see this certified gong show of Gaming Policy for what it is.

“Where these common beliefs of our generation will lead us is a problem not for one party, but for every one of us – a problem of the most momentous significance… Is there a greater tragedy imaginable than that? In our endeavor consciously to shape our future in accordance with high ideals, we should in fact unwittingly produce the very opposite of what we have been striving for?” (Hayek, “The Road to Serfdom”, page 60)

As the Monkey Movement hustles us toward prime time advertising dollars, please don’t listen to what storytellers of the Keynesian Kingdom say – watch how they get paid. If there’s any lesson we’ve learned from the Greeks by now it’s that markets don’t lie – politicians do (Greece’s stock market is down another -1.6% this morning, taking its straight down decline since February 18th to -18.3% as Greek bond yields hit record highs).

So what do you do with that today?

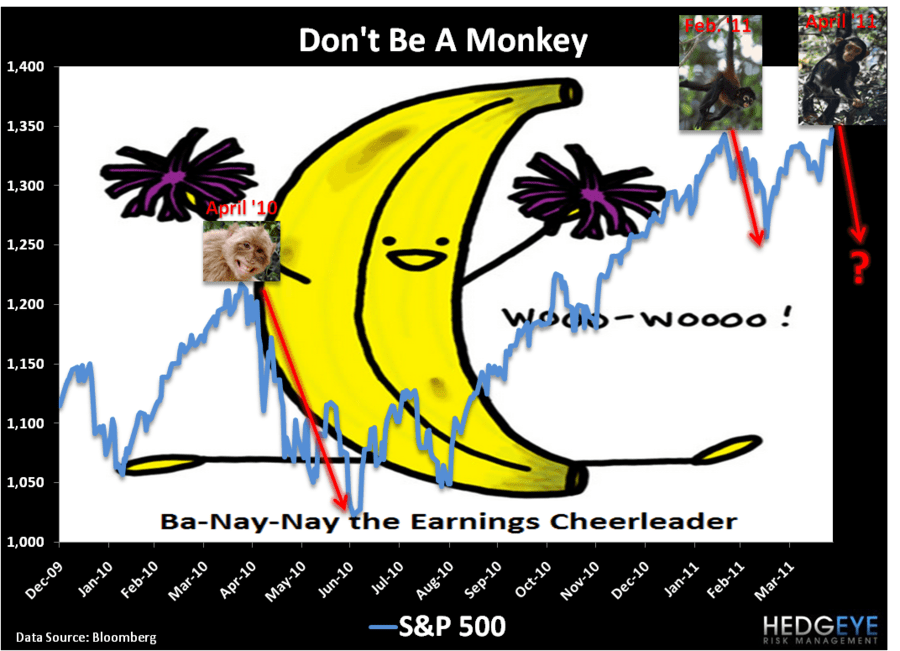

My risk management strategy into the Fed presser is very simple – don’t chase returns; take down your net long exposure; sell high.

I made this call in April of 2010 (SP500 dropped -15% to its August low). I made this call again in November of 2010 (November was down, and I got crushed in December). And again in February of 2011 (another -6.5% correction to mid-March where I covered at the YTD low)… again!

Two for three in calling for corrections from blow-off US Dollar Debauchery driven tops isn’t good enough. So I am looking at improving upon that … with my longest of long-term risk management calls not changing – BURNING YOUR CURRENCY AT THE STAKE will not end well.

If you want to get the US Dollar right, you need to get policy right – and The Bernank, sadly, will remain Indefinitely Dovish.

So what do you do with that? I usually start with the what not to do’s:

- Don’t go ideological in your portfolio (I’m leaning long ahead of the Fed today – 15 LONGS, 9 SHORTS in the Hedgeye Portfolio)

- Don’t sell The Inflation trade (it’s outperforming every global equity market other than maybe Russia for the YTD)

- Don’t be a monkey

What are the intermediate to long-term TREND and TAIL implications of the Monkey Movement perpetuating a US Currency Crash?

- It perpetuates The Inflation priced in US Dollars

- It structurally impairs the sustainability of long-term economic growth

- It dares institutional investors to chase “yield”

What am I seeing in the Global Macro Grind this morning that confirms any or all of these realities related to inflation and/or growth?

- Chinese stocks closed down for their 4th consecutive day (we’re long them) as the USD hits new lows, inspiring global inflation risk

- Brazilian stocks remain down -3.1% for the YTD and bearish from an intermediate-term TREND perspective = inflation risk

- Copper continues to breakdown (bearish TRADE and TREND) as global growth slows in the face of USD perpetuated inflation

- US Equities are rallying to lower-long-term highs (like Japan’s have for 20 years) on anemic volume and very concerning skew signals

- US Financials (XLF) are bearish TRADE and TREND (worst S&P Sector YTD) as a Currency Crash will enforce counterparty and haircut risks

- US Treasury Yield Spread continues to narrow (we are long a UST Flattener – FLAT) as US Growth Slows and long-term yields decline

All the while, US Housing is turning into the train wreck (double dip) that we have been calling for in the last year (Case Shiller Home Price Index saw prices drop on a year-over-year basis in 19 of the top 20 US markets yesterday - Washington, DC was the only bull market in housing – long live Julius Caesar’s Roman Empire that plunders its citizenry by clipping their coins).

US Housing Demand? The MBA mortgage applications index (our best high-frequency data gauge for demand) plummeted by -13.7% week-over-week this week. Apparently Americans aren’t dumb enough to take on The Bernank’s dare to lever themselves up with a “cheap” long-term liability. Short-term Central Planning, press conferences, and marketing events be damned!

My immediate-term support and resistance levels for Oil are now $109.98 and $114.11, respectively (we are long). My immediate-term support and resistance levels for Gold are now 1491 and 1524, respectively (we are long). My immediate-term support and resistance levels for the SP500 are now 1324 and 1350, respectively (we are short).

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer