Notable news items and price action from the past twenty-four hours along with our fundamental view on select names.

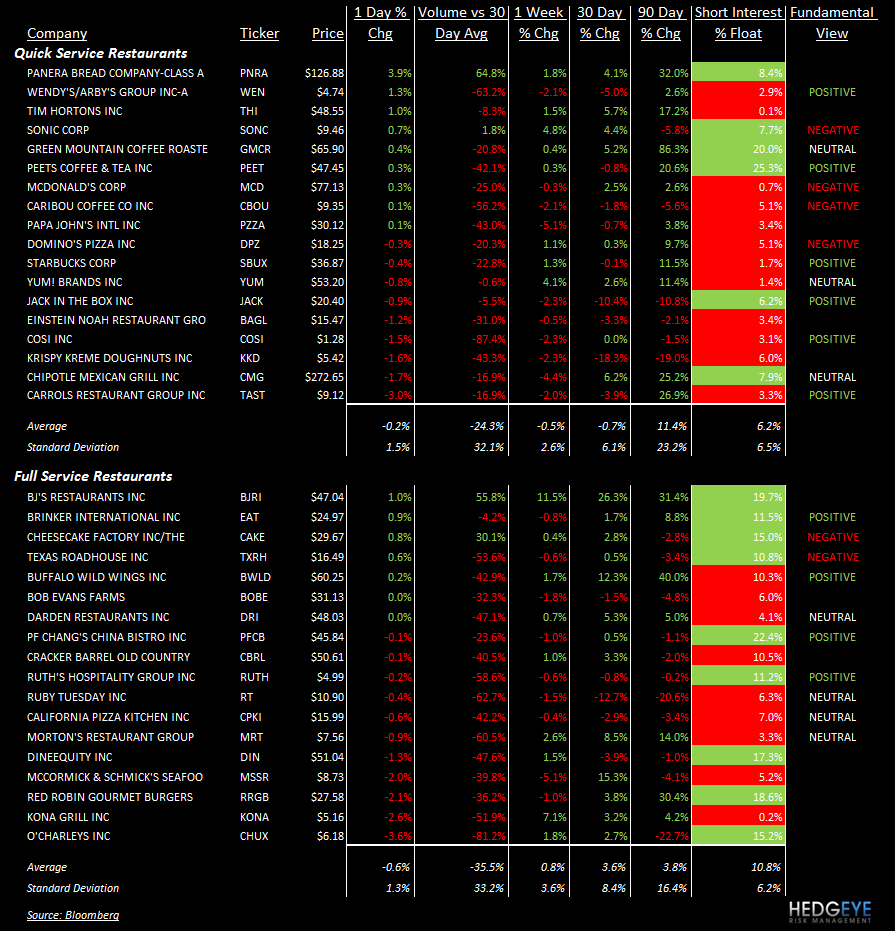

- PNRA shares gained 3.9% on accelerating volume. Next to BWLD, PNRA is the best performing restaurant stock over the past thirty days.

- PNRA and BWLD report earnings today after the close.

- PEET was downgraded to “Neutral” from “Outperform” at Robert Baird. The twelve-month price target is $48 per share.

- SBUX CEO Howard Schultz, responding to questions regarding his succession at a press briefing in Shanghai, said that he is “not going anywhere soon”. He also stated that he expects the Via brand instant coffee to be a “billion-dollar” business in a “short number of years”, according to Bloomberg News.

- CAKE traded higher on accelerating volume while EAT gained 0.9% on flat volume.

- SONC, BJRI, CAKE, and PNRA were the only four stocks that traded with a gain in volume versus the thirty-day average. In general, there was little volume in the restaurant space – or broader market for that matter.

- KONA and CHUX traded down -2.6% and -3.6%, respectively, on accelerating volume.

- MCD - raises prices by 2% in HK on wages: HKET

Howard Penney

Managing Director