TODAY’S S&P 500 SET-UP - April 26, 2011

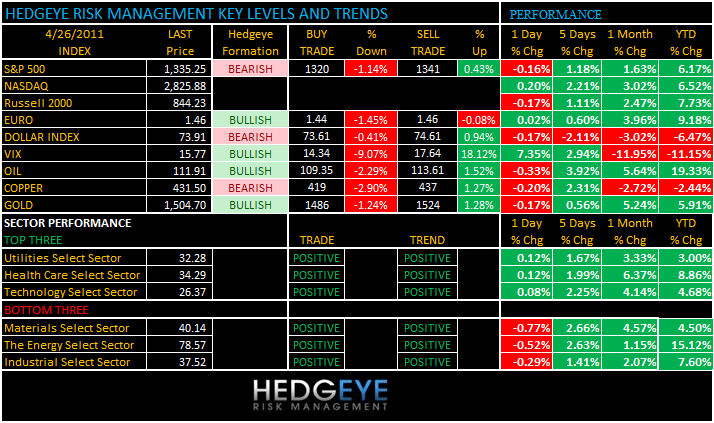

Europe continues to be more right leaning on policy than America; a Bloomberg story says ECB “must solidly anchor inflation expectations.” As we look at today’s set up for the S&P 500, the range is 21 points or -1.14% downside to 1320 and 0.43% upside to 1341.

SECTOR AND GLOBAL PERFORMANCE

The Financials remain the only sector broken on both TRADE and TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -259 (-1211)

- VOLUME: NYSE 697.93 (-14.13%)

- VIX: 15.77 +7.35% YTD PERFORMANCE: -11.15%

- SPX PUT/CALL RATIO: 1.30 from 1.60 (-18.48%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 21.29 -1.521 (-6.669%

- 3-MONTH T-BILL YIELD: 0.07% +0.01%

- 10-Year: 3.39 from 3.42

- YIELD CURVE: 2.72 from 2.74

MACRO DATA POINTS:

- 9 a.m. S&P Case-Schiller, est. (-3.30% Y/y)

- 10 a.m. Consumer Confidence, est. 64.5, prior 63.4

- 10 a.m. Richmond Fed Index, est. 20, prior 20

- 11:30 a.m.: U.S. to sell $30b in 4-week bills

- 1 p.m.: U.S. to sell $35b in 2-yr notes

- 4:30 p.m.: API inventories

WHAT TO WATCH:

- Peru was the worst performing global market overnight after former Peruvian military rebel Ollanta Humala opened a six-point lead in a presidential poll before a June 5 runoff vote. Concerns are he will strengthen ties with Venezuelan President Hugo Chavez.

- FDA says it will not appeal ruling that it must regulate ecigarettes as tobacco products, not drug-delivery devices - WSJ

- Tokyo Financial Exchange considering connecting its computer network with NYSE Euronext's - NQN

- YouTube to launch movie-on-demand service charging users to stream - The Wrap

- China raised capital adequacy ratios for its five largest banks in March - Bloomberg

- US, China to resume strategic, economic dialog 9-10-May in Washington - wires, citing US Treasury statement

- Yahoo Board Now More Open to Offers: WSJ All Things Digital

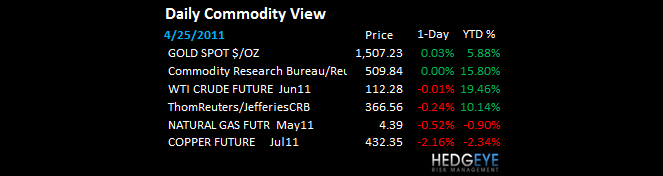

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Platinum Funds Expanding Fastest in Metals as Lonmin Seen Doubling Profit

- Copper, Zinc Demand in Japan to Climb on Evacuee Housing, Power Generation

- China May Buy More Sugar to Curb Fastest Inflation in Almost Three Years

- Commodities Snap Four-Day Winning Streak on Fed Speculation, China Credit

- Copper Drops Most in Seven Weeks on Concern China Tightening to Sap Demand

- Oil Supply Climbs in Survey on Forecast for Higher Imports: Energy Markets

- Gold, Silver Decline From Records as Investors Seek Cash to Protect Gains

- Wheat, Corn Drop as Some Investors Sell Following Rally; Soybeans Decline

- Sugar Falls as India May Allow Further Exports; Coffee Drops, Cocoa Gains

- Copper-Alloy Product Output in Japan Declines 3.7% After March 11 Disaster

- Investor ‘Euphoria’ to Drive India Silver Demand This Year, Exchange Says

- Rubber in Tokyo Reaches One-Month Low on China Rate Concern, Car Output

CURRENCIES

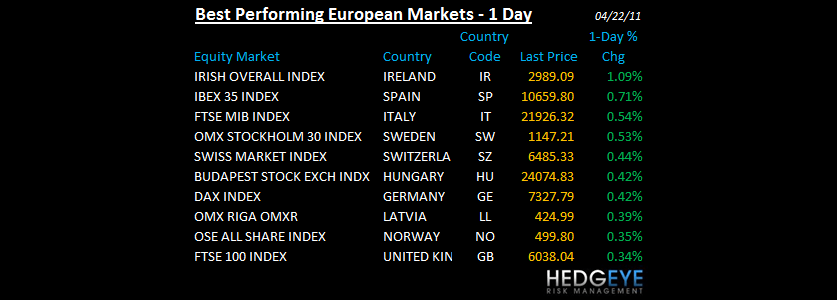

EUROPEAN MARKETS

- European markets are mixed and quiet with the holiday shortened week.

- Greek 2010 budget gap wider than estimated as euro-area debt hits record

- Indebted Spanish states pay Portugal-sized bond penalty rate: euro credit

- Trichet says policy makers must avert any jump in inflation expectations

- Dollar falls on speculation fed may keep supporting economy after qe ends

- Greece, Ireland, Portugal yields hit records on default concern

ASIA PACIFIC MARKTES:

- Asian Stocks Drop as Earnings Disappoint; Australia, Malaysia and Pakistan were higher on the day. Japan and China were the two worst performing markets

- China Said to Raise Capital-Adequacy Ratios for Biggest Banks to Curb Risk

MIDDLE EAST

Howard Penney

Managing Director