Last week the theme from the companies that reported earnings was those management teams universally underestimate the impact of inflation on margins and earnings in 2011. Top line trends remain intact for the better positions companies, outside of one-off events like what happened at Taco Bell.

CAKE and MCD generated the most buzz as they both struck cautious tones, lowering guidance (from core operations), clearly surprising investors somewhat judging by the stock price action.

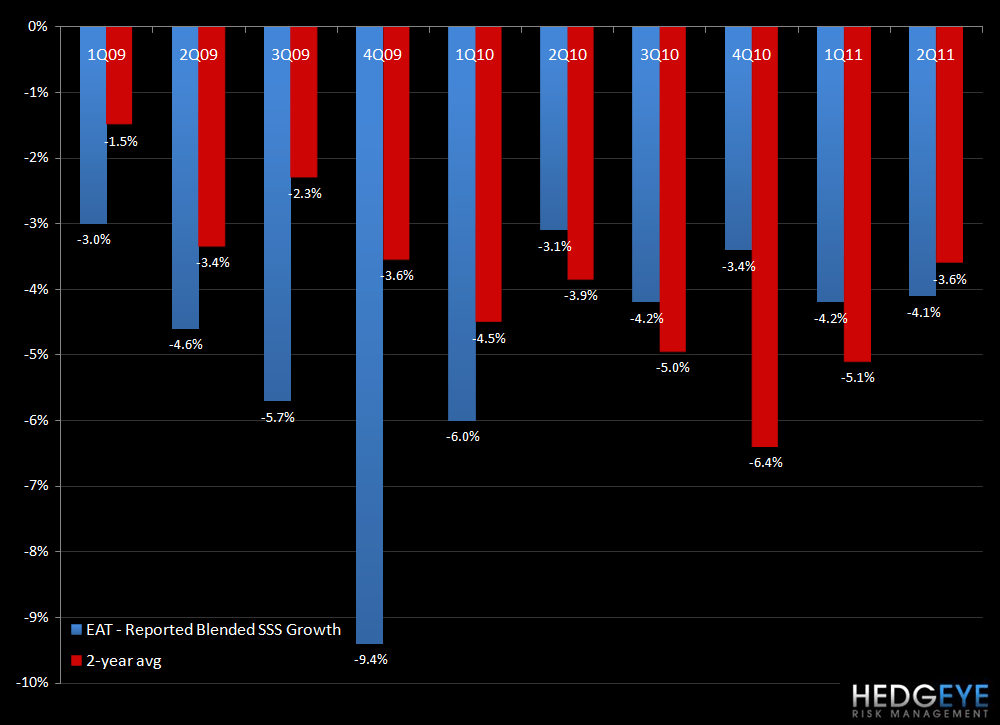

EAT (reporting 4/27 BMO): I continue to believe the EAT story. I see three key components to the story. First, the entire enterprise continues to benefit from the focus on the margin initiatives being put in place. Second, I am looking for continued improvement in top line sales for the Chili’s brand. Finally, I believe the street continues to underestimate the power of the margin initiatives and the improvement in sales trends at Chili’s, thus it appears that F3Q EPS estimates are low.

Key themes:

- Same-store sales: The Street will zero in on Chili’s sales trends. I think sales trend trended toward 0 to-1% at the end of the quarter. Key topics will include results from Oklahoma City (the first reimaged market) and the performance of the new value lunch initiative.

- Margin improvement: Importantly, any update on the kitchen technology initiatives.

- Demand Destruction Update: DRI and RT have talked about demand destruction. It will be interesting to see whether or not it will be a topic on the EAT call. My guess is that this theme will not be used as an excuse for why expectations for the quarter were not met.

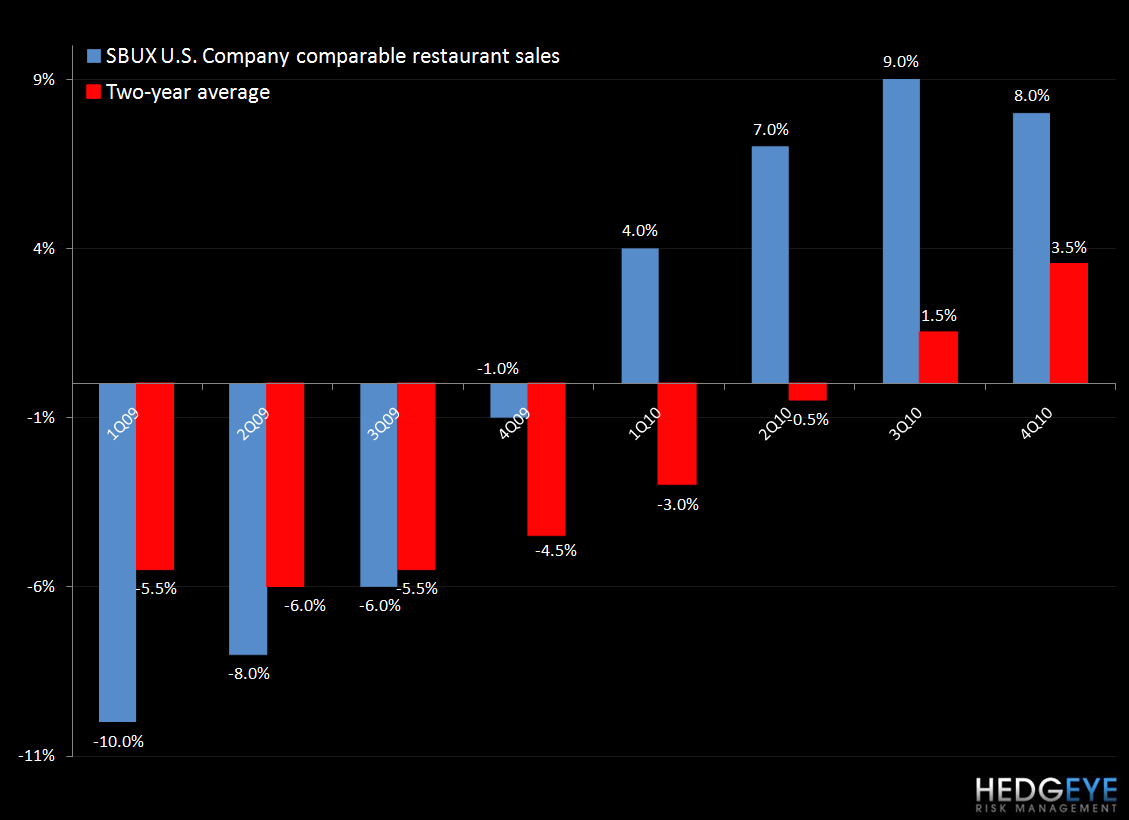

SBUX (reporting on 4/27 AMC): At roughly11.1x NTM EBITDA, SBUX is trading at a fairly rich valuation. I remain positive on the long-term trend of the business, with some reservations around near-term issues. The company continues to transition through momentous changes in the overall business model as new growth channels are developed and more control is asserted over distribution and other facets of the enterprise. The increased focus on higher-margin, low capex areas of the coffee industry – particularly CPG – and the increases in efficiency that should follow will drive higher returns over time.

Key Themes:

- Coffee prices will be under the spotlight: The most recent guidance includes a $0.20 hit from commodity pressures, primarily coming from coffee which is now locked for FY11.

- Limited upside to EPS: The significant increase in coffee prices and other commodities is limiting the upside in EPS outlook.

- I expect same-store sales in the USA to be 5-7%. This represents a marginal slow down on a one-year basis, but a continued acceleration on a two-year basis.

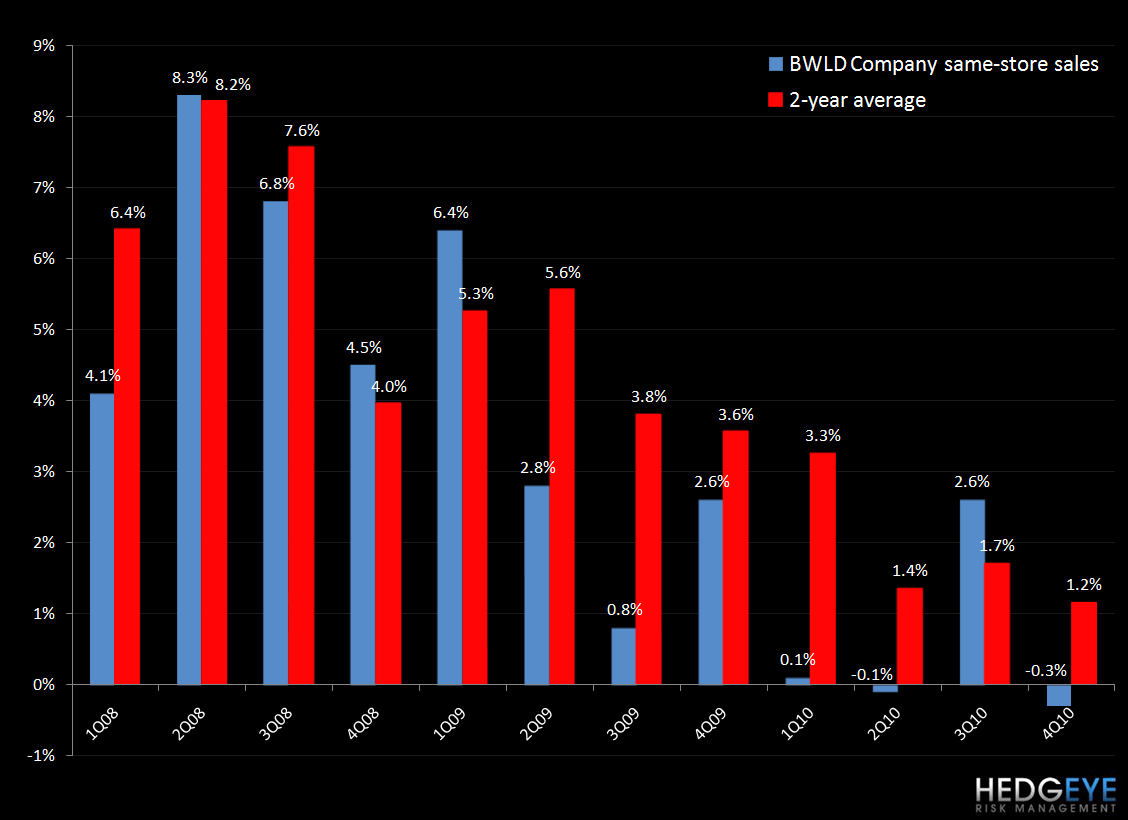

BWLD (reporting 4/26): Looking at the stock price performance alone, one could conclude the BWLD is having a great quarter. Relative to the rest of the industry, BWLD does not have commodity cost issues, so any up-tick in same-store sales will fully flow through the P&L and be a significant positive for earnings. The uncertainty surrounding the NFL player-owner dispute has not slowed the stock’s performance.

Key Themes:

- Top line trends: The Company is facing an easier 1Q comparison and I would expect a slight acceleration in trends with same-store sales of 3-to-4%. At the time of the 4Q10 earnings call, same-store sales were up 3.8% at company-owned restaurants.

- Commodity costs remain favorable: Since the 2Q call on 2/8/11, chicken wing prices are down 20%.

- Margin trends: Investors will be keen to learn of the impact, if any, from the January price increase and the trend in alcohol sales.

PFCB (reporting 4/27 BMO): PFCB needs to post a good quarter; I just don’t think this is the one. As I wrote in February, I think the company’s fiscal 2011 guidance is going to be hard to achieve. I’m wary of the company’s ability to pull off a 1-2% comp growth at the Bistro, which implies a significant acceleration in two-year average trends from where the company was tracking early in the quarter. Although the +1% comp at the Bistro signals that company is on the right track toward achieving +1-2% growth for the full year, it is important to note that the company faced its easiest monthly comparison from 2010 in January when comps declined 4.4%.

Key Themes:

- Margin improvement: PFCB’s FY11 guidance assumes a year-over-year improvement in restaurant level margins. The bulk of this favorability is expected to fall in 1Q11 as the company laps the nearly 220 bp decline in margin that occurred in 1Q10 as a result of inefficiencies associated with last year’s Happy Hour rollout. Margins should be helped in FY11 from the growing contribution of PFCB’s global brands business, which is a high-margin business (management guided to a nickel more of earnings from this business alone in 2011 relative to its reported $0.01 per share earnings contribution in 2010). Offsetting this benefit, however, is the expected inflationary headwinds which are expect to hit the COGS, labor and operating expense lines of the P&L. Specifically, management guided to a 3-4% increase in its total commodity basket, higher wage rates and healthcare costs and increasing energy and supply costs.

- Traffic Trends: Traffic declined for the first time in 2010 during the fourth quarter when average check increased, not surprisingly, also for the first time in 2010. Traffic declined 0.9% during 4Q10 versus negative traffic growth in 4Q09. Traffic turned positive in 1Q10, up 0.8% and remained positive in 2Q10 and 3Q10, up 2.6% and 2.8%, respectively.

- Sentiment: With 22% of the float held short, the buy-side is decidedly bearish on PFCB. Only 52% of the analysts that cover PFCB are positive and there are 12% that have an outright sell on the stock.

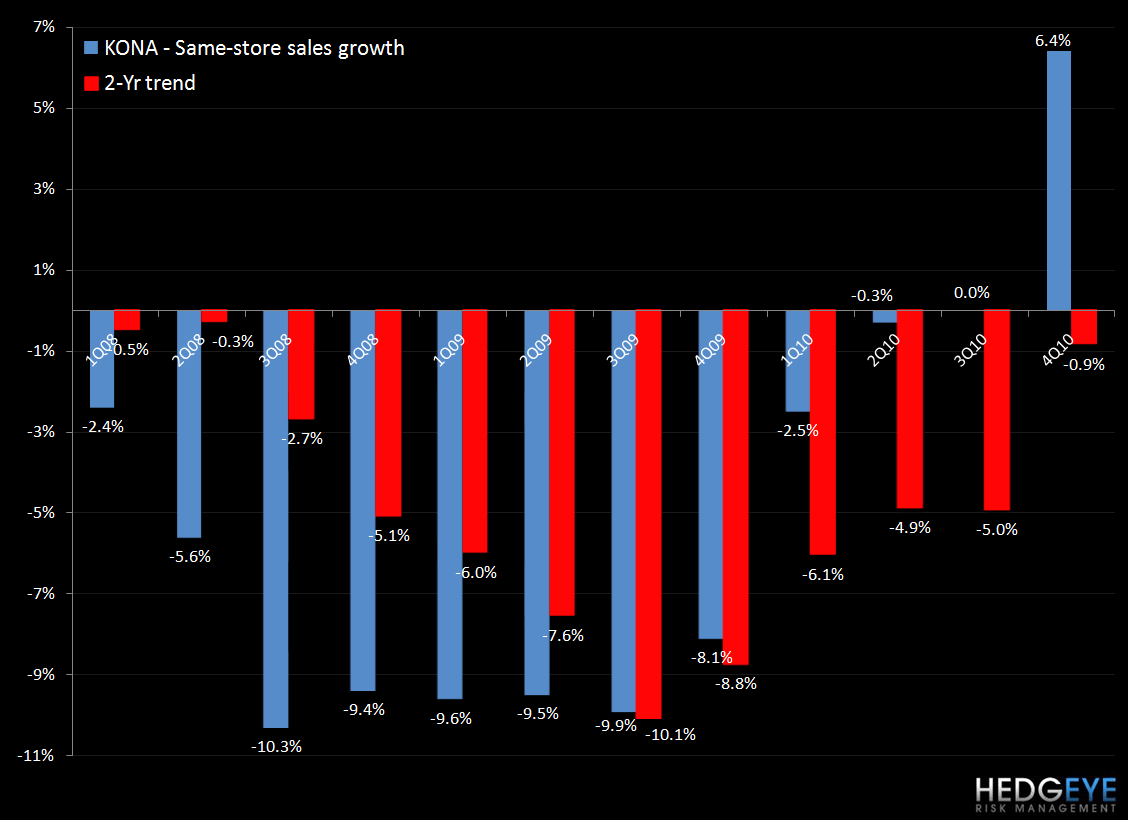

KONA (reporting 4/27): is a name that is generating plenty of attention of late. As the recent Knapp Track data for March illustrates, casual dining performed strongly through 1Q despite rising gas prices. The Knapp Track report highlighted the inverse relationship between income level and share of wallet spent on gasoline. The implication here is that higher-end concepts, such as KONA, will be less impacted by rising gasoline prices than will lower-end concepts. With this in mind, as I wrote on 4/14 in my note titled, “KONA – GAIN ALPHA ON THE KONAVORE DIET”, I estimate that comparable restaurant sales were trending at approximately +4% in 1Q11, bringing an acceleration in two-year average trends to 0.8% for the quarter. Operational initiatives are also set to add earnings power to a stock that I think will print its first profitable quarter as a public company in 2011. These factors, along with a relatively low valuation versus peer companies, should attract investors over the coming quarters.

Key Themes:

- Same-store sales: The Street will want to see continuing momentum after a strong 4Q10. We know from management commentary that the same-store sales bounce in 4Q10 was broad-based; the key at this juncture for investors is whether or not it is sustainable.

- Margin initiatives and inflation: Improving comps will go a long way towards offsetting inflation on the food line for KONA in 1Q11. Exposure to seafood remains an issue and what management says on this subject during the earnings call will be of interest. The company is targeting rent, G&A, and labor as areas of focus where margin can be gained to offset commodity inflation.

- The road to profitability and growth: If comparable restaurant sales come in strong and management has positive news to report in terms of operational initiatives, I would expect that the earnings call may focus, in part, on returning the company to profitability and – ultimately – growth over the intermediate term.

PNRA (reporting 4/26 AMC): PNRA has been a standout stock during 1Q; its stock gained appreciably on 4Q10 earnings results in February and the company, fortunately, has wheat prices locked roughly flat with 2010. Early indications from this earnings season are that commodity outlook is going to be a central theme for the restaurant space. Last quarter, PNRA raised the mid-point of its margin guidance 25 bps which, based on the maintained same-store sales guidance, implied an upward revision to EPS. With sentiment as positive as it is, the company needs to both print a strong quarter and provide robust outlook for this stock to continue on its 2011 to-date trajectory.

Key Themes:

- Same-store sales: Consensus is calling for an acceleration in two-year average trends for PNRA company stores and, given the generally strong/stable trends in restaurants of late and PNRA’s recent performance, I would expect the company to meet expectations of a +3.9% comp for 1Q.

- Margin performance and outlook: PNRA currently has its commodity inflation guidance for the year set at 3% and, while wheat is locked for the year roughly flat versus 2010, it will be interesting to see if management raises its inflation outlook. Furthermore, to the extent that contracts are coming up for renewal, particularly the wheat contract, and the company could see pressure on margins over the intermediate term.

- Sentiment: Sentiment on this one is as dovish as dovish gets. Any deviation from the script that sentiment implies could see a meaningful swing in sentiment and – more than likely – the stock price.

Howard Penney

Managing Director