“The dove descending breaks the air with flame of incandescent terror.”

-T.S. Eliot, Little Gidding (1942)

“Little Gidding” was the final of four brilliant poems in T.S. Eliot’s “Four Quartets” which helped him win the Nobel Prize for Literature in 1948. Each of the four poems considers the lessons of history within the context of one of the four elements: air, earth, water, and fire.

The element of fire in the aforementioned quote is an important metaphor to consider when watching what the US Government is doing to the US Dollar. Through a deliberately dovish monetary policy to inflate, the US Federal Reserve is Burning The Buck.

Since the unaccountable bureaucrats at the Fed and their friends who are working for Groupthink Geithner at the US Treasury will be the last to call up a chart of the US Dollar Index (career risk management), we’ll do it for you, weekly, until this Currency Crash looks less likely:

- Week-over-week, the US Dollar Index was down another -0.91% last week to close at $74.11 = a fresh 2-year low

- Closing down for 13 out of the last 17 weeks, the USD Index has lost -8.6% of its intermediate-term value in the last 4 months

- Since President Obama and Treasury Secretary Geithner strapped on the accountability pants in 2009, the US Dollar is down -16.8%!

So who cares?

Evidently our Almighty Central Planners don’t. They don’t even talk about it… and neither do the kowtowing “blue chip” economists who allegedly analyze their Keynesian policies.

But, The People do…

With the US stock market up +97.8% from its March 2009 low, you’d think that the policy to get us paid with some equity market performance would make this country really happy about all of this. Not.

Why not?

Alongside last week’s Crashing Currency, here’s what the price of other things that trade predominantly in US Dollars did last week:

- Oil = +2.1% to $112.29/barrel

- Gold = +1.1% to $1503/oz

- CRB Commodities Index (19 Commodities) = +1.4% to 367

Nice. If you are long of The Inflation, that is…

If you aren’t, well – I guess the message for you from The Bernank is too bad. Take it in the pump – and like it.

Ben Bernanke’s incompetent forecasts will be center stage on this week’s Macro Catalyst Calendar with following events:

- Tuesday – New Home Sales (trending at record lows despite Bernanke begging you to lever yourself up with a “cheap” mortgage)

- Wednesday – FOMC interest rate decision (Indefinitely Dovish); and Case/Shiller Home Prices for FEB (train wreck)

- Thursday – Q1 US GDP (running at least 30% below Bernanke’s initial forecast - almost all of Wall St has cut their estimates)

- Friday – Michigan Consumer Confidence for April (making lower-highs); and April month-end markups (US equities)

How will The Bernank spin alchemy’s free money spool into an Indefinitely Dovish message on Wednesday?

He’ll flip the switch from saying there is no inflation to worrying the world about Growth Slowing As Inflation Accelerates. At $112/barrel oil (up +180% since Obama and Geithner took office in 2009), The Inflation at the pump is almost 2x that of the US stock market. Meanwhile, gold and silver are trading at all-time highs this morning (all-time is a long time) – so he’s going to admit he sees that, I hope…

And while hope is not an investment process, watching marked-to-market expectations in both the US currency and Treasury markets is. Both the US Dollar crashing and UST yields breaking intermediate-term TREND support of 0.71% this morning are signaling Bernanke will remain dovish. He’ll blame growth slowing (Q1 GDP report Thursday) and US housing being the train wreck that he and Greenspan helped perpetuate.

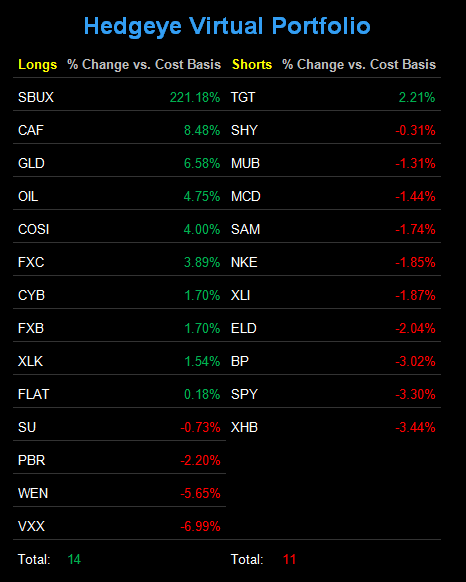

In terms of asset allocation, this still leaves me long of The Inflation (Gold and Oil), and long of relatively unlevered growth where I can find it (China and US Tech). Since the week of March 28th, I’ve taken down my Cash position from 52% to 40% - the updated Hedgeye Asset Allocation Model has the following composition:

- Cash = 40% (down from 43% week-over-week)

- International Currencies = 30% (Chinese Yuan, Canadian Dollar, British Pound = CYB, FXC, and FXB)

- International Equities = 9% (China = CAF)

- Commodities = 9% (Gold and Oil = GLD and OIL)

- US Equities = 6% (Technology = XLK)

- Fixed Income = 6% (US Treasury Flattener = FLAT)

Understanding full well that the US Dollar correlation-risk to just about everything that I am long is surreal at this point, I’ll just call this positioning out for what it is – an explicit bet that the Fed remains Indefinitely Dovish until the US Government is forced to face a US Currency Crash and all of the understood consequences embedded therein.

My immediate-term support and resistance lines for oil are now $109.12 and $112.91, respectively. My immediate-term support and resistance lines for the SP500 are now 1319 and 1339, respectively.

My personal thanks to Big Alberta for riding shot-gun for the team last week, and best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer