THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - April 25, 2011

The Inflation trade remains in place; US Dollar down (down 13 of the last 17 weeks); continued signs of growth slowing with copper down -1.2% this morning (bearish TREND); while monetary inflation skyrockets (gold and silver hitting new highs). As we look at today’s set up for the S&P 500, the range is 20 points or -1.37% downside to 1319 and 0.12% upside to 1339.

SECTOR AND GLOBAL PERFORMANCE

The Financials remain the only sector broken on both TRADE and TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 952 (-1033)

- VOLUME: NYSE 812.78 (-15.44%)

- VIX: 14.69 -2.52% YTD PERFORMANCE: -17.64%

- SPX PUT/CALL RATIO: 1.60 from 2.17 (-26.33%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 22.30

- 3-MONTH T-BILL YIELD: 0.06%

- 10-Year: 3.42 from 3.43

- YIELD CURVE: 2.74 from 2.74

MACRO DATA POINTS:

- 10 a.m.: New Home Sales, est. 280k (up 12%), prior est. up 250k (down 16.9%)

- 10:30 a.m.: Dallas Fed Manufacturing, est. 13.4, prior 11.5

- 11 a.m.: Export inspections, grains

- 11:30 a.m.: U.S. to sell $29b 3-mo., $27b 6-mo. bills

- 4 p.m.: Crop progress (winter wheat, cotton, corn)

WHAT TO WATCH:

- Average pump price climbed 11.5c to $3.88 thru April 22: Lundberg survey. Obama said last week a task force will examine if oil, gas prices driven higher by market manipulation.

- Nike (NKE) may be poised to climb as it works to control rising materials and labor costs, Barron’s

- China’s 2011 trade surplus may narrow to 2% of GDP because of rising commodity prices, Reuters says, citing a report from the State Council’s Development Research Center.

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Silver Surges to All-Time High as Investors Seek Protection From Inflation

- Crude Oil in New York Rises a Fourth Day as Middle East Violence Escalates

- Copper Drops in New York on Signs of Ample Supplies in China, Biggest User

- Palm Oil Declines as Lower Malaysian Exports Threaten to Boost Inventories

- Corn Advances as Rains Delay Seeding in U.S.; Wheat Jumps to 2-Month High

- China's Corn Imports May Expand This Year to 2 Million Tons, Baize Says

- Rubber in Tokyo Declines as Demand May Weaken on Reduced Car Production

- Hedge Funds Bullish on Natural Gas as Nuclear Output Falls: Energy Markets

- Corn, Soybeans May Rise as Cold, Weather Slows U.S. Seeding, Survey Shows

- India Gold Imports May Fall for Third Month on Prices, Industry Group Says

- Tsunami Quickens ‘Terminal Decline’ of Northern Japan’s Fishing Industry

- Most China Aluminum Capacity Lacks State Approval, Business News Reports

- Corn Seen Topping Wheat on Demand, Raising Tyson's Costs, Helping Syngenta

CURRENCIES

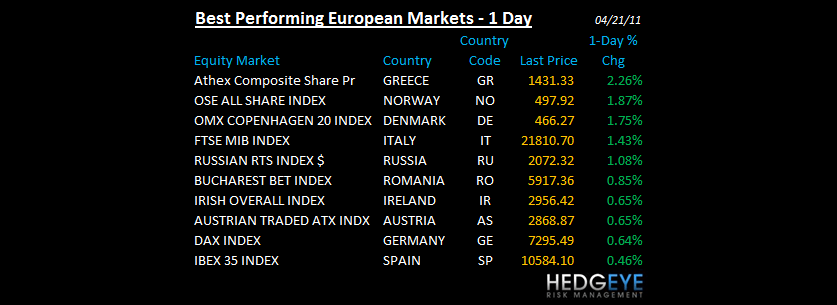

EUROPEAN MARKETS

- European markets are closed in observance of the Easter holiday

ASIA PACIFIC MARKTES:

- Asian stocks were mixed overnight on earnings concerns and China declined on increased inflation concerns.

- Japan March corporate services price index +0.4% m/m, (1.2%) y/y.

- Japan March supermarket comps +0.3% y/y.

- Hong Kong’s market is closed for a holiday.

MIDDLE EAST

Howard Penney

Managing Director