MCD reported 1Q results this morning and, while the initial glance was encouraging, the upward revision in the firm’s FY11 commodity inflation outlook is weighing heavily on the stock.

MCD is an impressive organization that creates value for its shareholders, jobs for the economy, and serves billions of people globally. I have been bearish on the stock since December and released a Black Book to that effect in January. While March comps in the U.S. exceeded my expectations, as well at consensus, concerns about margin sustainability – concurrent with a likely slowdown in comparable restaurant sales growth – are coming to the forefront.

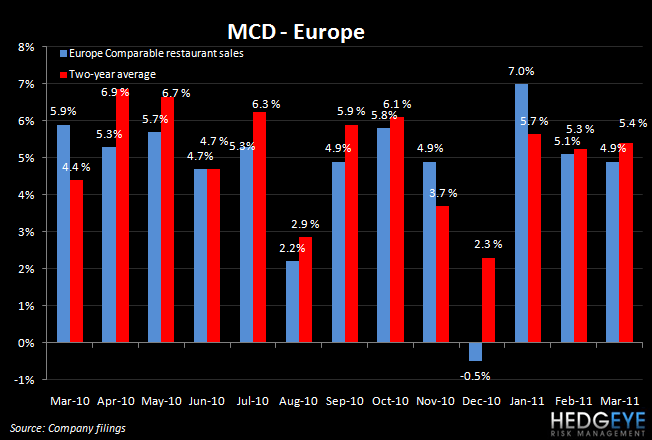

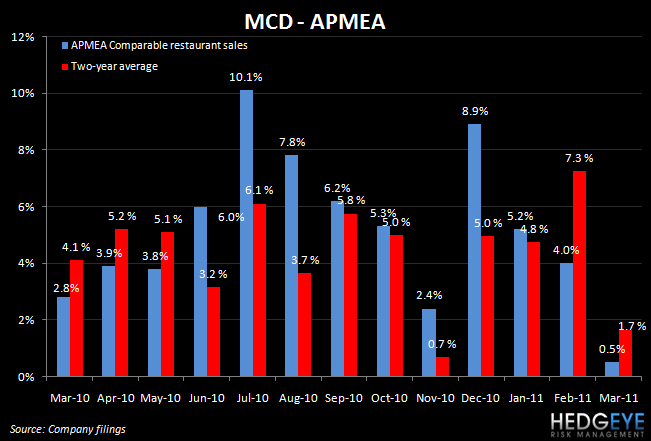

MCD reported global comparable restaurant sales growth of 3.6% for 1Q11. The March numbers showed strength in the U.S. with comps coming in at +3.0% versus consensus at 1.7%. MCD took a 1% price increase in early March and will likely take more this year. Europe, in spite of austerity measures being implemented across the continent, saw comparable restaurant sales growth of 4.9% in March (consensus +3.2%) and 5.7% in the quarter. The company also took a 1% price increase in the first quarter. APMEA was slowed somewhat by the impact of the disaster in Japan as March comparable restaurant sales eked out a 0.5% gain year-over-year (+2.0% consensus), rounding out 3.2% growth for the first quarter.

While comps exceeded expectations, on aggregate, restaurant level margins declining for the first quarter since 1Q09 (prior to that it had been 3Q05!) was what generated the most attention. With compares becoming more difficult as the summer progresses, gaining leverage over operating costs will be difficult. In addition, management raised its FY11 guidance for its food cost basket from +2 to 2.5% in the U.S. and +3.5 to 4.5% in Europe. It seems almost certain that a significant price increase will be necessary to absorb this inflation. While MCD pointed to its track record of not having raised prices since last 2009, it is important to note that commodity costs were deflating until recently for MCD; a price increase will be necessary at some point in 2011. As the chart below shows, the decline in margins brings MCD out of the “Nirvana” quadrant – positive comps and margins – for the first time since 1Q09.

On the ability to “manage through an inflationary environment”, management assumed a defensive tone on the call, referencing 2008 as an example of the company successfully navigating an inflationary environment. While this is true, I believe the point I made regarding the overdependence on beverages is applicable in this instance. Frappes and smoothies in 2Q and 3Q proved to be high-margin items for MCD and, coupled with year-over-year commodity favorability, were highly accretive to the company’s bottom line. Furthermore, the beverages were highly effective sales drivers. Per our MCD Black Book, we estimate that frappes and smoothies counted for 5.7% and 5.9% of the 2Q and 3Q10 comps, respectively. For reference, 2Q and 3Q10 comps for the MCD U.S. business were 3.7% and 5.3%. If our estimates are correct, MCD U.S. excluding frappes and smoothies, declined on a same-store sales basis in 2Q and 3Q10. The initiatives being rolled out this summer, namely strawberry lemonade and an additional flavor of smoothie, have big shoes to fill.

The MCD franchise system is more robust than any other in the business. However, as was pointed out on the earnings call, it is easy to keep a franchisee happy with growing market share and increasing margins. It will be interesting to see how franchisees will react to the ever-expanding menu and increasing commodity costs, all the while attempting to maintain the low prices that corporate aligns the brand with.

The sentiment around this stock shows just how high expectations are for the stock. These expectations are difficult to meet and, in 2Q and 3Q of 2011, McDonald’s has a tough few months ahead of it. Guest counts, long the lifeblood of the company’s comparable sales growth, are likely to be negatively impacted by any steep price increases. Inflation looks like it is almost certainly going to require a steep price increase on the part of the company. This is certainly the most interesting period for this stock in the last seven years.

Howard Penney

Managing Director