“A national debt, if it is not excessive, will be to us a national blessing.”

- Alexander Hamilton

Like Keith, I’m a born and bred Canadian. Despite my nationality of birth, after living in the United States for upwards of the last fifteen years, I can quite confidently say this is a great country. At Hedgeye, we spend a lot of time critiquing the political leadership in Washington, DC in our research, but that shouldn’t be confused with a general critique of the United States. I’ll say it again, this is great country.

In 1999, the 106th Congress passed a bill that allocated federal funds to renovate the Hamilton Grange, which was Alexander Hamilton’s family home. In that bill, Congress indicated that this preservation was to “honor the man who more than any other designed the Government of the United States.” At times, we’ve sided more with the Jeffersonian philosophy as it relates to governing, but there is no disputing Hamilton’s influence on the founding of this nation. Indeed, as the first Secretary of the Treasury his words continue to have relevance in fiscal and monetary policy discussions.

Setting aside the discussion of the extent to which the government should be involved in our lives, I think we would all agree that government does have its place and can, with the right leadership, do great things. In fact, to Hamilton’s point, based on a government’s ability to tax and borrow (if done prudently these don’t have to be bad words!) it can build infrastructure and provide appropriate social services, which make the outcome of any government debt a “national blessing.” That is, if its use is not “excessive”.

Late last week in our Q2 quarterly theme call, we called for a potential crash in the U.S. dollar. Once again, we didn’t make this call because we lack American patriotism, but rather because of the fundamentals. Stepping back for a second, though, we should frame up what exactly a crash means for a currency.

In the last 30 years, the largest annual decline in the U.S. dollar index was -18.5% in 1985, while the average decline for that period was 0.11%. In the year-to-date, the U.S. dollar index is down -6.6%. So, we are four months into 2011 and the U.S. dollar is already down close to 1/3 of its largest annual decline ever. Our view is that the U.S. dollar could decline potentially another -5% through the course of the quarter and roughly -10%-ish through the course of the rest of the year. If this occurs, it would be the largest annual decline for the U.S. dollar index in 30-years and that, my friends, is a crash.

This morning, we are seeing a continuation of this move with many currencies, once again, trading up close to a percent versus the dollar. Interestingly, even in Europe, where sovereign debt woes continue to accelerate, the currencies are strong this morning with the British Pound up +0.92% versus U.S. dollar and the Euro up +0.73%.

We certainly get that being bearish on the U.S. dollar at this point isn’t exactly a contrarian call, but, to be fair, we’ve traded the U.S. dollar in the Virtual Portfolio 20 times since the firm’s inception and have been right 20 times. In addition, of the 46 currency positions we’ve taken in the Virtual Portfolio over the same duration, we booked a gain on 41 of them. Clearly, this isn’t our first Currency Rodeo. That said, according to a recent survey by Bank of America, all but 6% of their global clients are bearish on the U.S. dollar, which is not inconsistent with some of our internal surveys. In addition, Barclays reported the commodity assets under management have reached an all-time high at $412BN.

Being long commodities is in many respects the same trade as being short the U.S. dollar, and we’d be remiss to not at least factor into our models that the investment community is leaning hard in one direction. But the question remains: is consensus bearish enough on the dollar? Our answer on this, until the facts change, is “no”.

As we analyze the U.S. dollar versus global currencies, we focus on three key factors: debt, deficit, and interest rates. Currently, the U.S. dollar lines up negative on all three of these fronts, specifically:

1. Excessive debt – In the last couple of years, it has become cool to quote Reinhart and Rogoff and bandy about sovereign debt-to-GDP ratios, so this isn’t new, but according to usdebtclock.org, the United States has a debt-to-GDP ratio of 96%. This is negative for GDP growth, which is negative for the U.S. dollar as slower growth leads to longer term accommodative monetary policy and higher than expected fiscal deficits. Further, the United States’ future debt trajectory is much steeper than any of its “AAA” peers (Canada, United Kingdom, Germany and France) due to a lack of a credible deficit reduction plan. To add insult to injury, the politicians in Washington will once again debate increasing the debt ceiling in mid-May while global currency traders watch real-time;

2. Long term deficit – This year the United States federal government will run a deficit north of $1.5 trillion dollars, which is more than 10% of GDP. (This is slightly better than Sierra Leone.) The real issue with the deficit is a lack of a credible plan to reduce the deficit going forward. While many nations globally have already begun austerity programs, the United States has no plan and the recently approved $38 billion spending reduction for the duration of this year is only likely to have a real benefit of some $380 million. President Obama has given June as the time frame by which he hopes to have an agreement on a long term budget, but our view is that based on how far apart the Democrats and Republicans are on the tenets of the plan, this time frame will be blown threw;

3. Monetary policy bifurcation - Simply put, interest rates and perceived future interest rates move currencies. Almost every major modern nation in the world has either tightened policy (witness Sweden and China most recently) or is reporting data that suggests tightening is imminent. In contrast, not only is the United States still implementing Quantitative Guessing Part II, but recent signals out of the Federal Reserve suggest we could see a version of QE-lite after June, so we think the U.S. Dollar will fall victim to additional easing in the face of the world tightening.

In order to shift our investment view on the U.S. Dollar we need to believe that these factors will improve absolutely and relatively and, as of yet, it is hard to make that case. Meanwhile, the U.S. dollar index continues to be in a bear market in our quantitative models.

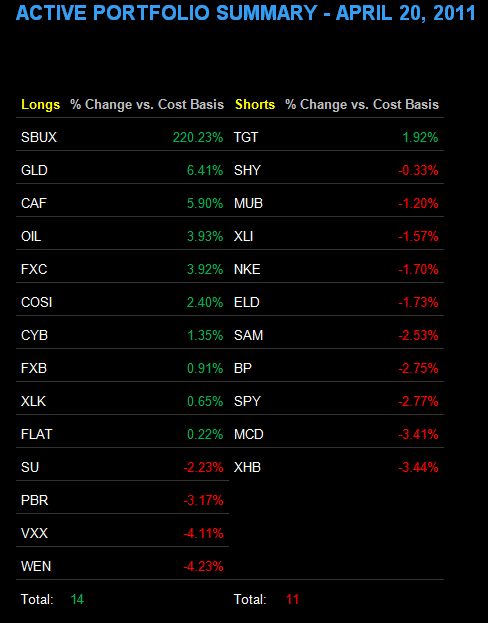

Currently in the Virtual Porfolio we are long the Canadian dollar, long the Chinese Yuan, and long the British Pound. We covered our short position in the U.S. dollar (UUP) yesterday. This isn’t about politics or patriotism, but risk management.

Enjoy the long weekend with your families.

Keep our head up and stick on the ice,

Daryl G. Jones

Managing Director