This note was originally published at 8am on April 18, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“A good hockey player plays where the puck is. A great hockey player plays where the puck is going to be.”

-Wayne Gretzky

Late last week Keith and I were in Boston meeting with clients on the eve of the beginning of the Boston / Montreal first round playoff series. While Bostonians and hockey fans around the world are gearing up for the beginning of the NHL playoffs, money managers, as usual, are contemplating portfolio positioning for the upcoming months.

Whether your strategy involves bottom-up company analysis, top-down economic analysis, or a healthy dose of both, the objective is the same: to anticipate where the Investment Puck is going ahead of the competition. To borrow from Mr. Gretzky, good money managers play the market where it is, great money managers play the market where it is going to be.

Currently, from a macro perspective, the primary focus of many money managers is attempting to determine the timing of the next move in monetary policy. Given the high correlation between U.S. monetary policy, the U.S. dollar, and many global asset classes, this is the key area to focus.

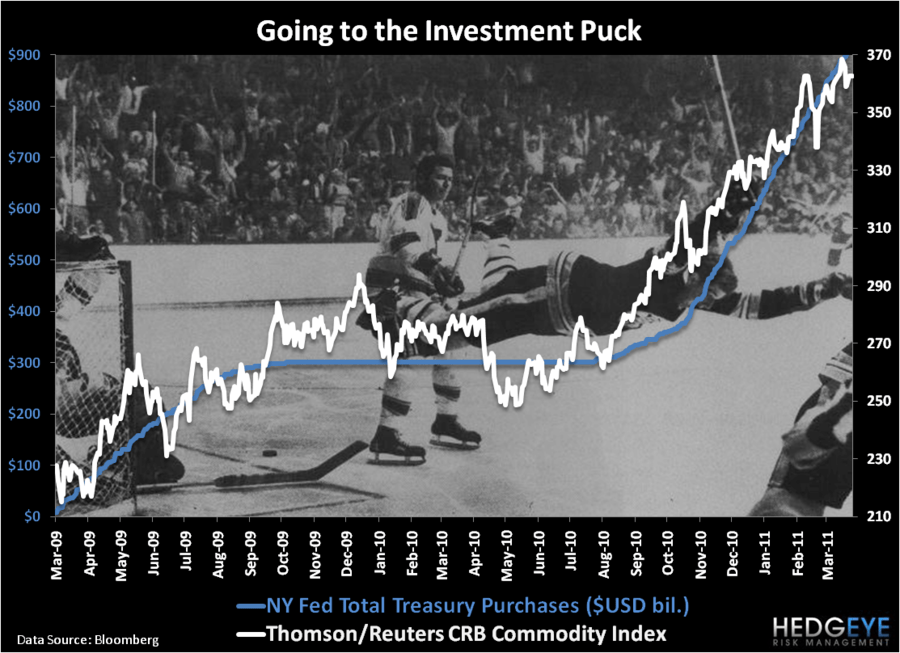

To emphasize this point, in the Chart of the Day attached below, we show the correlation of Federal Reserve Treasury Purchases with the CRB index, which highlights the high correlation to loose U.S. monetary policy and inflation of many U.S. dollar-based commodities.

While “fundamental” supply and demand certainly matters, if you are invested in oil, or oil related equities, keep one market quote front and center: the U.S. Dollar Index. Over the past three months, the correlation between the U.S. dollar index and WTI Crude Futures is -0.86, while the correlation between the U.S. Dollar Index and Brent Crude Futures is -0.91. Dollar down continues to equal oil up, and decidedly so.

In our presentation late last month titled, What’s Next For Oil?, we highlighted turmoil in the Middle East as a key factor supporting the price of oil. Indeed, violence in Libya continued to escalate this weekend as the recent U.S. led NATO intervention so far seems largely ineffectual. According to British Prime Minister Cameron this weekend:

“We have to ask ourselves, what more can we do to protect civilian life and to stop Qaddafi’s war machine unleashing such hell on his own people.”

With an unknown outcome Libyan oil production remains well below its full output of 1.8MM barrels per day, which supports oil prices.

On the other side of the ledger for oil, there are mounting bearish supply and demand data points. Specifically, according a recent report from the International Energy Administration, oil consumption grew 2.6% year-over-year in Q1 2011. This was a sequential slowdown from 4.1% year-over-year growth in consumption in Q4 2010. Further, the IEA now expects oil consumption to grow 1.6% year-over-year in all of 2011 versus 3.4% for 2010. In addition, crude oil stocks in the United States grew 0.5% year-over-year, which is near decade highs. With the price of gasoline up 24.6% year-over-year, oil stocks should continue to build.

If you don’t believe the oil market is oversupplied in the short term, take it from the Saudis. This weekend the Saudi Oil Minister said the following in a press conference:

“The market is overbalanced ... Our production in February was 9.125 million barrels per day (bpd), in March it was 8.292 million bpd. In April we don't know yet, probably a little higher than March. The reason I gave you these numbers is to show you that the market is oversupplied."

This morning China increased the reserve ratio for their banks by 50 basis points to 20.5% and pledged there is more to come. So unlike The Bernank who attempts to manage monetary policy via a press conference (according to the top article on Bloomberg this morning), the Chinese continue to proactively combat inflation.

Chinese tightening is incrementally bearish for commodities, to argue different is simply story telling. (Interestingly, the Chinese equity market closed up +23 basis points despite this incremental tightening, which is positive for our long Chinese equity position in the Virtual Portfolio.)

As bearish supply and demand data points continue to mount for oil and other U.S. dollar based global commodities, the increasing focus is on determining the direction of the U.S. dollar, which will be driven by U.S. monetary policy. So, where do we stand on the direction of monetary policy? To some extent, it will depend on the data.

We are quite confident housing has another leg down (email sales@hedgeye.com if you are an institutional prospect and want to talk to our Financials Sector Head Josh Steiner about his 100+ page negative thesis on housing). Further, employment is seeing anemic improvement, which is mostly being driven by people leaving the workforce and will not see much improvement with U.S. GDP growth likely to come in lower than expected this year. On both of these key fronts, Chairman Bernanke will have plenty of cover to keep rates low for an “extended period”.

Ironically, government CPI, which is not the best proxy for inflation in our estimation, may actually be the thorn in The Bernank’s side. As we highlighted in our Q2 Theme presentation, CPI compares are set to get very easy in the United States. In fact, June CPI last year was +1.1%, which is really the beginning of the easy comps. Starting this summer it is likely that we see government reported data that looks inflationary and will make it difficult for The Bernank to remain perpetually dovish.

As monetary policy begins to tighten in the U.S. and theoretically strengthen the U.S. dollar, the music will likely stop for the commodity rally in the intermediate term. This will create an investment opportunity of another kind if you are at the Investment Puck. And as famed U.S. Olympic Coach Herb Brooks once said:

“Great moments are born from great opportunities.”

Keep your head up and stick on the ice,

Daryl G. Jones

Managing Director