“The case has, in some respects, been not entirely devoid of interest."

-Sherlock Holmes

Sherlock Holmes is the fictional detective created by Scottish author and physician Sir Arthur Conan Doyle. Doyle based the character of Sherlock Holmes on a number of prominent physicians of the late 1880s. Indeed, criminal detective work certainly has parallels to a medical examination. The role of the physician is to provide a diagnosis after thoroughly collecting information both from and about the patient. Great investment research incorporates a similar process.

In our daily morning research process, each Sector Head provides relevant facts in our internal research meeting, which underscores our moves in the Virtual Portfolio that day (in combination with our quantitative models). Quite often, which makes sense when you get enough”Type A” Hedgeyes in a room, we have much broader discussions. A few weeks back our Financials Sector Head Josh Steiner asked, effectively, whether the federal budget deficit could be narrowed by just reversing the stimulus. That is, shouldn’t compares on stimulus spending get much easier, which would effectively narrow the deficit? As usual, a great question.

To back up, the American Recovery and Reinvestment Act of 2009 (“ARRA”) was passed by the 111th U.S. Congress in February 2009. According to many reports, the act was nominally worth some $785 billion to the economy. Roughly 1/3 of this came in the way of tax cuts, while almost 2/3s came in the way of increased government spending.

The philosophical rationale for ARRA, according to our friends at Wikipedia, was as follows:

“The stimulus was intended to create jobs and promote investment and consumer spending during the recession. The rationale for the stimulus comes out of the Keynesian economic tradition that argues that government budget deficits should be used to cover the output gap created by the drop in consumer spending during a recession.”

Seems simple enough, even for a hockey head like myself.

Interestingly, if we look at government spending in the 2008 – 2010 period we can actually see the impact of the stimulus act on government ledgers. In fact, according to usgovernmentspending.com the U.S. federal government spent $2.98 trillion in 2008 and $3.59 trillion in 2010. So, the net increase over this period was just over $600 billion, which roughly equates to the spending portion of The Stimulus.

In theory, Dear Watson, there then should then be a step down in spending as ARRA, or The Stimulus, winds down and begins to compare against itself. Interestingly, in 2011 federal government spending is actually expected to step up to $3.61 trillion!

The long run compounded annual growth rate of federal government spending from 1990 to 2007 is 4.47%. If we apply this growth rate to the 2008 – 2011 period, 2011 normalized government spending on that basis would be $3.42 trillion, almost $200 billion less than what the government will actually spend and roughly one-third the size of ARRA, or The Stimulus. So, where did the stimulus go? Confused? I certainly am, but it seems that cutting government spending is not as simple as favorable compares against a “one-time” spending program.

But on to a more interesting case, that of today’s global macro investment outlook. While Keith is enjoying Disney World with his two little risk managers, Jack and Callie, the Hedgeye Research Juggernaut continues to grind. Three key data points to call out this morning are as follows:

1. Europe – Overseas on the continent, equity indices are rallying hard this morning up almost 2% across the board with the FTSE and DAX leading the way. Interestingly sovereign bond market are flashing a different signal as bond yields continue to rise in the PIIG nations and both Spain and Portugal are selling debt at much higher rates than even three weeks ago.

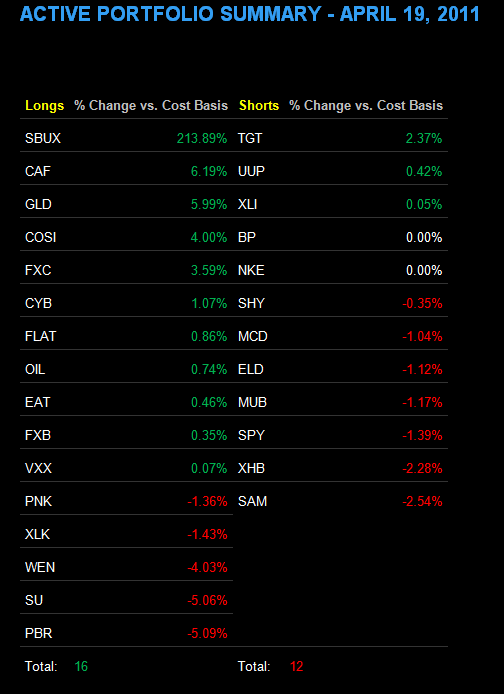

2. Asia – Asian equity markets are also positive across the board, with China the clear negative divergence up only 27 basis points. The noteworthy callout from Asia is the following report: “A senior Hong Kong monetary official told The Wall Street Journal on Tuesday that China's central bank is "actively considering" new rules that would make it easier to bring yuan funds raised offshore back onto the Chinese mainland.” This is positive for the long position we are holding in the Chinese Yuan in the Virtual Portfolio.

3. Technology earnings – We are long the technology sector in the Virtual Portfolio via the etf XLK and are seeing serious fundamental support this morning from a number of key technology bell weathers. In fact, Intel, IBM, Juniper Networks, and VMware all exceeded analyst expectations. The results suggest that businesses are spending again. That said, IBM is trading lower as contract signings, an indicator of future demand, were less than expected.

Before I let you get back to your detective work this morning, I’ll leave you with one last quote from Sherlock Holmes:

“How often have I said to you that when you have eliminated the impossible, whatever remains, however improbable, must be the truth?”

Indeed.

Keep your head up and stick on the ice,

Daryl G. Jones

Managing Director