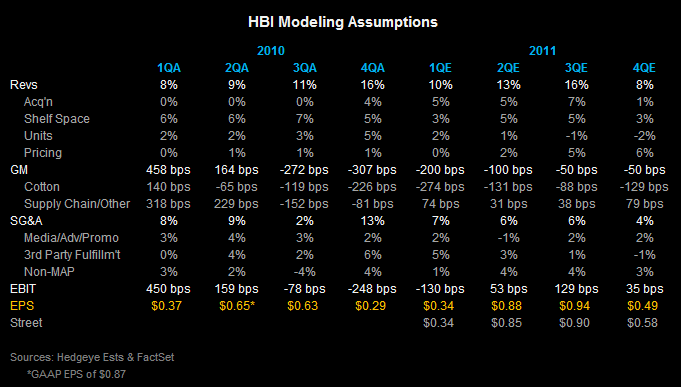

In looking at the upcoming quarter for HBI before the market open tomorrow, we expect few surprises. We’re shaking out at $0.34 for the quarter. Relative to consensus, we expect slightly stronger top-line results to be offset by lighter margins. We don’t expect disappointment as it relates to guidance, as the company still has three quarters of the ‘Gear for Sports’ acquisition to go, which will relieve strain in the P&L that might otherwise be there in the core business. Here’s a look at our assumptions for the quarter:

Sales:

- Top-line growth of 10% in the quarter will be driven equally by organic and inorganic growth in Q1.

- The Outerwear segment will account for the majority of growth. Gear For Sports alone will account for 5% with another ~2% driven primarily by continued strength at Champion. The balance of incremental revenue is going to be derived from shelf space gains (~2% alone from DG) in addition to modest price increases towards the end of the quarter.

Gross Margin:

- Cotton remains the primary driver here. With average cost of $0.82 versus $0.52 last year, we expect margins down -200bps by our math with pricing and supply chain savings of nearly +100bps partially offsetting a -300bps cotton headwind.

SG&A:

- Aside from the top-line, this is where we are most differentiated from consensus. We expect SG&A growth of 8% driven by two key factors, the incremental Gear costs (~$10mm) and continued 3rd party fulfillment expenses of another ~$10mm.

Taking into account $4mm in incremental interest expense related to the acquisition and a tax rate of 21% (one of the greater variables, which could tweak earnings higher) we’re looking at $0.34 versus the Street at $0.34E for the quarter and $2.66 vs. $2.73 for the year. Given the challenging setup from a SIGMA perspective, we see limited opportunity for upside in the quarter with compares getting progressively more favorable providing an offset over the balance of the year. We have numbers going up to $3.11 in EPS next year with FCF increasing from $173mm to $297mm (~$3/sh) in ’11 and ’12 respectively.

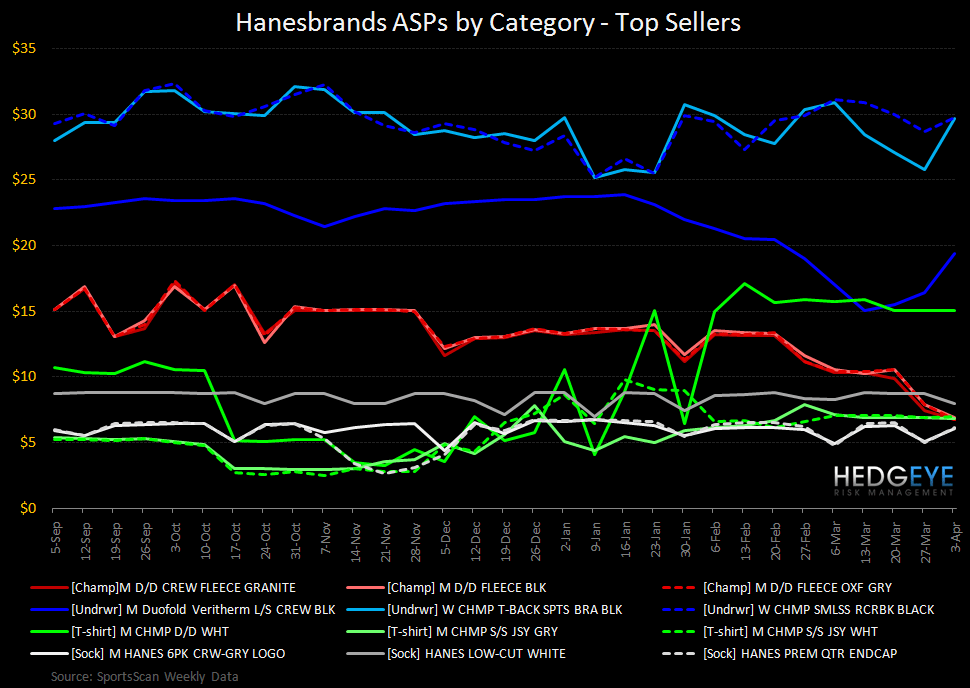

With the shares up over 20% since reporting Q4, pricing, additional shelf gains, and the latest update on where cotton is secured will be key elements in driving continued outperformance from current levels that we will be looking for on tomorrow’s call.

Additionally, one of the keys to the management’s strategic plan and our thesis is that Hanes will be able to command a certain element of pricing in order to navigate current inflationary pressures. In order to track the progress and timing of these price adjustments as well as consumer receptivity, we’ve created a tracking mechanism utilizing our SportScan data that captures ASPs, YY change, and resulting sales growth across four different categories – Champion, Undergarments, T-shirts, and Socks. The charts below illustrate the results. Call us with any questions, or if you’re interested in receiving this with regularity going forward please let us know.

Casey Flavin

Director