Position in Europe: Long British Pound (FXB)

As is typical for Mondays, we release our weekly European Risk Monitor. This morning peripheral risk premiums have popped dramatically in response to 1.) ongoing concerns that Greece must restructure its debt, 2.) Finnish elections over the weekend that saw the anti-bailout/euro-skeptic True Finns party gain significant share, 3.) widening yields from a Spanish bond issuance, and 4.) Moody’s decision to downgrade long-term deposit ratings of five Irish banks to junk.

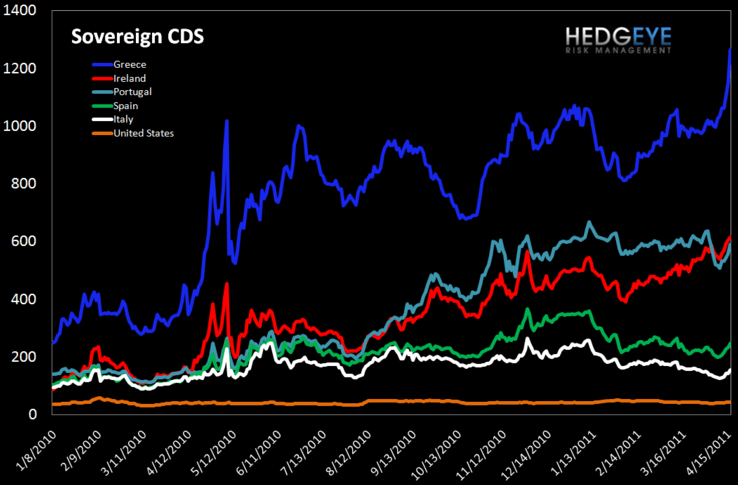

As we’ve seen over recent weeks, European sovereign debt contagion fears have accelerated. While Greek leadership continues to deny that its public debt needs restructuring (a position also held by French finance minister Christine Lagarde), the Germans under finance minister Wolfgang Schaeuble continue to press in opposition. As the debate heightens, the market is sending a clear signal, with Greek sovereign CDS jumping a full 112bps day-over-day to 1262bps as the Greek 10YR bond yield gained 65bps to an all-time high of 14.5% today! (see chart below)

Finnish parliamentary elections on Sunday further weighed on the region as the True Finns more than quadrupled its share of the vote to 19% (to place third) under a platform opposed to Eurozone bailouts. According to exit polls, the conservative National Coalition Party of current finance minister Jyrki Katainen leads with 20.2%, followed by the opposition Social Democratic Party (which also opposes further bailouts unless private investors and lenders are forced to take financial losses) with 19.4%. While the weeks ahead will bear out the structure of a coalition government, the True Finns’ gain under the leadership of Timo Soini puts into play an inflection in Finland’s traditional pro-Europe stance, and complicates a potential bailout for Portugal assuming a new Finnish government rejects further bailouts and unanimous approval must be reached by all Eurozone member states to grant new rescue loans.

Rounding out a thick flow of European news this AM, Spain sold €3.51 Billion of 12M bonds at an average yield of 2.770%, far outpacing the previous issue a month ago of 2.128%, and €1.15 Billion of 18M bills at 3.364% versus 2.436%. Additionally, Moody’s downgrade the long-term deposit ratings of Allied Irish Banks, EBS Building Society, and Irish Life & Permanent Group Holdings by two notches to Ba2, and ICS Building Society and Bank of Ireland (one and two steps respectively) to Ba1, the highest junk rating. This follows Moody's decision last Friday to downgrade Ireland's debt two notches to Baa3.

In response, Spanish CDS jumped 13bps to 246bps and Irish CDS rose 30bps day-over-day to 589bps. Our weekly European Financial CDS monitor indicates that bank swaps in Europe were wider week-over-week, widening for 34 of the 39 reference entities and tightening for 5 (see chart below).

As yields push up and credit ratings deteriorate, it will be more and more difficult for Europe’s periphery to (re)finance its debt. This should spell underperformance, in particular from the peripheral capital markets, yet associated weakness could also spill over to the region’s most stable countries, and in particular the common currency that up until this week was pushing against $1.45 versus the USD on higher benchmark interest rates form the ECB and a continued drag on the USD from weak US fiscal and monetary policy.

We covered our position in Spain today in the Hedgeye Virtual Portfolio with the country getting hammered down to our immediate-term TRADE support level. Our long-term TAIL view of Spain remains bearish.

Matthew Hedrick

Analyst