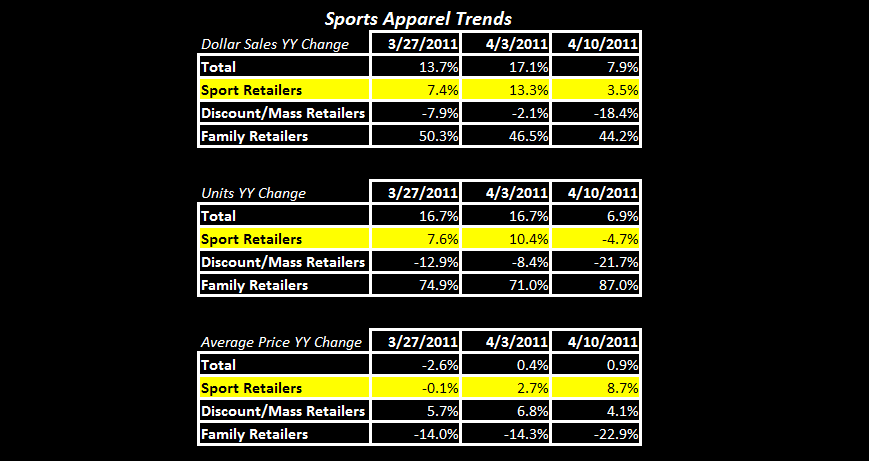

Underlying trends for the athletic space were mixed last week due to heightened variability around the Easter shift. Athletic apparel decelerated while footwear rebounded – on the other hand, underlying (trailing 3-week) trends for apparel remain very positive while footwear is down low single-digits, but stable.

So, is it time to hit the panic button on footwear? No. Let’s consider the impact of the “Egg Effect.”

A lot has been made of this Easter shift, but at the end of the day what does it really mean for the space? In an attempt to quantify it, here’s the math:

The domestic footwear market is approximately $48Bn at retail, with a 45/55 split between athletic ($22Bn) and non-athletic ($26Bn) respectively. Footwear retailers contend that demand begins to ramp 3-weeks before the Easter holiday. However, based on our weekly athletic footwear data, there is a notable pickup only two weeks in advance over which weekly sales as a percent of total annual sales increase by up to 30-40bps (see the chart below). While non-athletic footwear is the greater beneficiary of the shift, our assumptions account for only a two week boost to error on the side of conservatism. Based on the seasonal surge during which weekly sales volume ramps from 1.8% of annual sales to 2.1%-2.2% heading into Easter, the shift equates to $200-$300mm in incremental Easter sales, or 12%-16% growth across the industry. With that pending demand in-store over the next two weeks and footwear down only 2-3% on a trailing 3-week basis in the face of this benefit last year, the underlying trend in footwear is in fact very much intact.

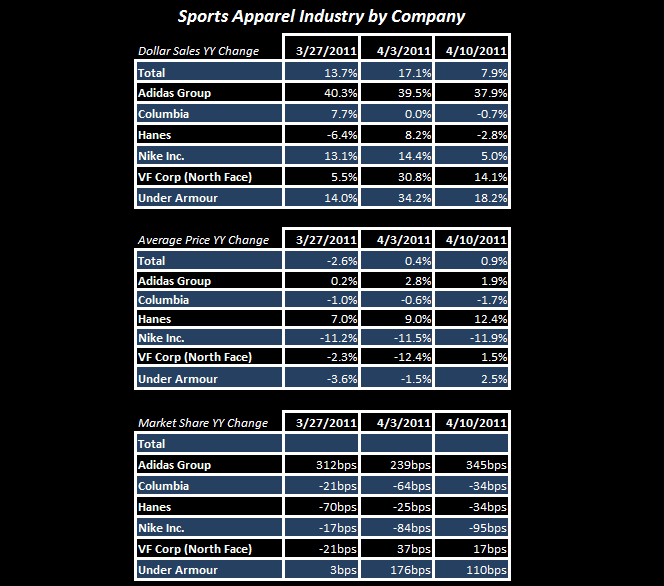

As for apparel brand performance, Adidas remains impressively strong along with solid mid-teen growth out of both Under Armour and VF (The North Face). Adi continues to be a steady share gainer with Under Armour improving nicely over the last couple of weeks driven by the incremental contribution from its new charged cotton product. Nike’s trend slowed on the week with ASPs declines still outpacing peers.

In footwear, brands rebounded across the board sequentially with Nike, Adidas, and Reebok the notable outperformers. An honorable mention for Under Armour with sales up 10% on the week confirming the positive sales trend seen in recent weeks. The sole negative callout is Skechers with sales down -25% and 280bps of share loss.

Before we bake in expectations for +20% growth in footwear next week, it’s important to realize that sales were up 21% last year before decelerating to the high single-digits. With that in mind, when looked at in aggregate we see a strong end to Q2 for footwear retailers.

Casey Flavin

Director