This note was originally published at 8am on April 12, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The name of the author is the first to go

followed obediently by the title, the plot,

the heartbreaking conclusion, the entire novel

which suddenly becomes one you have never read,

never even heard of,”

-Billy Collins, Forgetfulness

Human beings are forgetful creatures. Coaches the length and breadth of this country berate their players to never make the same mistake twice on the court, field, ice, or track. In retrospect, having tried my utmost to follow this adage in my sporting – and later in my professional endeavors – I think “never make the same mistake ten times” would perhaps be a more realistic goal to set!

Even with regard to that diluted standard, I am sure I have fallen short. Nonetheless, I am going to make a bold statement to begin this Early Look in earnest: investors, being human, are forgetful. Believing what they want to – or are paid to – believe, many commentators are pointing out the differences between “this time” and “that time”. While there are differences; it is 2011 now and it was 2008 then, the similarities are also striking. This earnings season could very well shape up to be the period where similarities become glaringly obvious.

Last night AA officially started the 1Q11 earnings season with a miss on revenues and beat on earnings; investors’ attention is turning towards the balance of the earnings season. StreetAccount reported last week, for the fourth straight time, that negative preannouncements had outnumbered positive updates over the prior seven days.

The market has been notably resilient in the face of major geopolitical unrest, natural disasters, and a veritable tsunami of freshly-printed Greenbacks originating from the epicenter of Modern-Day Keynesian Dogma: Washington, D.C. Despite this, and besides the greasing of the market coming from the Free Money Fed policies, the outlook for the S&P 500 merits caution, if not outright divestment.

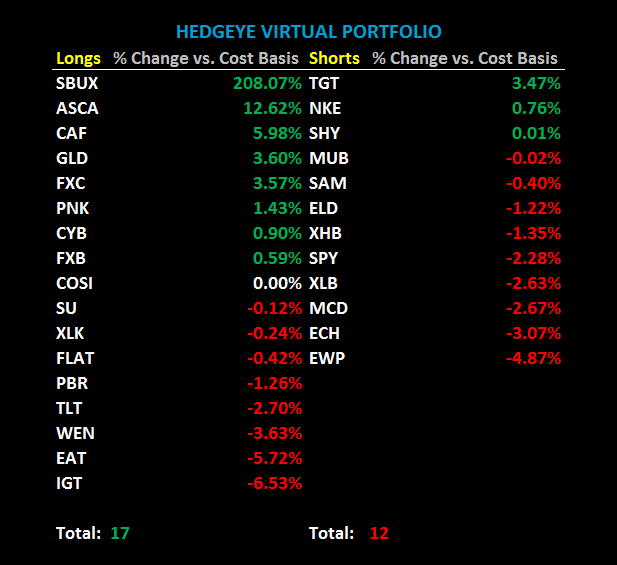

Currently, in the Hedgeye Asset Allocation model, Keith has maintained near a 0% allocation to US Equities in recent weeks (though is currently at 6%) and is short the S&P 500 in the Hedgeye Virtual Portfolio. Downward revisions to GDP numbers on a global basis are being coupled by endemic inflation in commodity markets as the US Dollar is debauched. Hedgeye has been vocal that this current period represents a pivotal process in the market where growth slowing and inflation accelerating is being felt by corporations, citizens, and even bureaucrats alike. The cycle of corporate earnings is peaking. Tops are processes, not points.

The tone AA set is important, with a market cap of $19 billion and a business model that is tethered to the global macroeconomic climate. AA represents a prism through which we can attempt to view part of the global economy. The issues AA faces go beyond this quarter as the stock remains 64% below the peak set on 7/16/07. Importantly, from a top-line perspective, we think AA will not stand as an outlier this earnings season.

Despite the recent optimism, much of it grounded in reality (for a change), surrounding the improving job market and the solid top-line environment evident in corporate earnings, AA’s quarter could be just the beginning of a string of corporate earnings that call the sustainability of the current trend into question. Consistent with the past few quarters, FX tailwinds and various types of productivity gains will likely allow many companies to meet earnings expectations.

Having said this, it is worth noting that the deep cost-cutting measures that were made in the midst of the Great Recession have left the majority of companies, on balance, leaner and needing less revenue growth to leverage fixed costs. Nonetheless, with expectations high and inflation accelerating, revenue growth remains a key focus of corporate management teams. If such a scenario plays out this quarter, it would corroborate quite neatly with Hedgeye’s view that margins – at the level of the past few quarters – are set to roll over.

In my view, expectations have already begun to moderate under the threat to profit margins from surging commodity and raw material costs, along with the shocks to the global supply chain from the earthquake/tsunami in Japan. Alcoa’s management team’s statements confirmed this, as it stated, “earnings were curbed by a weaker U.S. dollar and higher energy and raw-material costs”.

As we proceed through this earnings season, I would argue that it is important to recognize the signs of demand destruction that is going to result from inflation. Gas prices, thus far, do not seem to have impacted consumer spending as meaningfully as one may have thought, given that prices at the pump over the past couple of months have steadily risen. Perhaps the consumer is somewhat accustomed to high food and energy costs, having been there before, or at least has faith that prices will come down, be it by Centrally-Planned or Divine means?

In the US, consumer behavior has not been as affected, as immediately as it was during the last spike in gas prices. However, signs are starting to manifest themselves that Americans are not impervious to the effects of inflation, even if the Chairman of the Fed is. Darden Restaurants’ Inc. CEO Clarence Otis opined on his company’s most recent earnings call that gas prices were “having a dampening effect” on Darden’s business. Other casual dining companies have since echoed Otis’ comments, predicting that the almost-certain-to-be higher gas prices during the upcoming summer months will result in demand destruction that will hurt their profitability via the top-line.

The case for inflation-induced demand destruction is playing out in the UK today. UK retail sales dropped by 1.9% (on a same-store basis sales declined 3.5%) in March as accelerating inflation squeezed households’ spending power at the fastest rate in 60 years; the decline is the biggest drop since the series began in 1995.

It is not late 2007/early 2008, it is 2011, but lest we be forgetful, this is the same country that it was three years ago. Gas prices at this level will matter on the corporate bottom line and, if one listens to the early indications from executives such as Otis, they already matter a great deal.

The Faithfully Forgetful may point out other differences between 2008 and 2011. Housing was more of an issue then, someone might say. At Hedgeye, we would argue that the housing markets of 2008 and 2011 are eerily similar in that not enough attention is being paid to the fundamental strength, or lack thereof, in the housing sector. As our Financials Team has reiterated for months on end, housing is set to decline sharply throughout 2011. This call is no longer a prediction; it has been playing out for months now as Corelogic, Case-Shiller, and New Home Sales data continue to highlight softness in residential real estate. As always, feel free to reach out to sales@hedgeye.com if you would like to see the detail of Hedgeye’s Housing Headwinds thesis.

Rather than pointing out the obvious differences, I believe it is the similarities between this market and that of three-and-a-half years ago that are far more interesting. A market showing resilience in an upward trend is encouraging for investors and so it should be. However, a market barely breaking stride in the face of tectonic shifts in global geopolitics and parabolic price action in commodity markets exhibits a detachment from reality and should not be comforting to investors. Having blind faith in the appearance of resilience, and forgetting how the story may end and has ended before, could prove a costly mistake.

Function in disaster; finish in style,

Howard Penney