THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - April 15, 2011

Today at 11am we are hosting our 2Q11 Global MACRO Theme conference call (email if you’d like to participate).

- American Sacrifice - a scenario analysis and calendar of catalysts for the US Dollar

- Trashing Treasuries – long of The Bernank’s Inflation, short US Treasuries

- Housing Headwinds II – part deux in the Josh Steiner chronicles of the best Housing work on Wall Street

As we look at today’s set up for the S&P 500, the range is 19 points or -0.50% downside to 1308 and 0.95% upside to 1327.

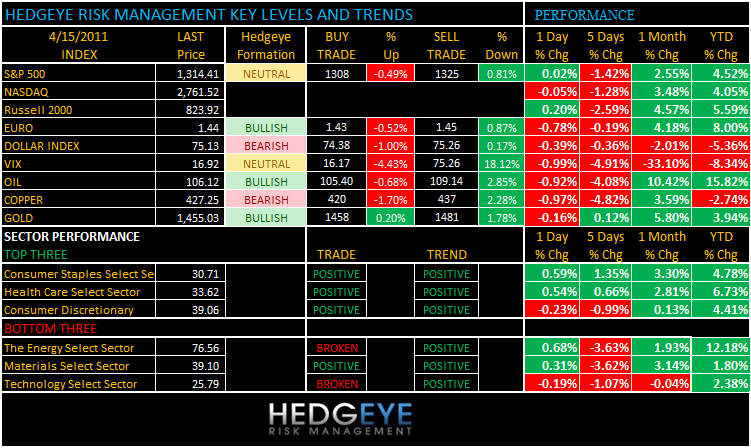

SECTOR AND GLOBAL PERFORMANCE

We now have 5 of 9 sectors positive on TRADE and 8 of 9 sectors positive on TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 227 (+126)

- VOLUME: NYSE 894.31 (-0.73%)

- VIX: 16.27 -3.84% YTD PERFORMANCE: -8.34%

- SPX PUT/CALL RATIO: 1.58 from 1.68 (-6.21%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 20.96

- 3-MONTH T-BILL YIELD: 0.07% +0.01%

- 10-Year: 3.51 from 3.49

- YIELD CURVE: 2.74 from 2.74

MACRO DATA POINTS:

- 8:30 a.m.: Consumer Price Index, est. 0.5% M/m, prior 0.5%

- 8:30 a.m.: Empire Manufacturing, est. 17.00, prior 17.50

- 9 a.m.: Net long-term TIC flows, est. 40.0b, prior $51.5b

- 9:15 a.m.: Industrial production, est. 0.6%

- 9:15 a.m.: Capacity utilization, est. 77.4%

- 9:55 a.m.: UMich Confidence, est. 69.0, prior 67.5

- 10 a.m.: Fed’s Evans speaks in NYC

- 11:15 a.m.: ECB’s Constancio speaks in New York

- 1 p.m.: Baker Hughes Rig Count

- 1:30 p.m.: Fed’s Hoenig to speak on economy at Purdue

WHAT TO WATCH:

- Pressure for CVS Caremark to split up increasing - NYT

- T. Rowe Price considers exiting UTI Asset Management - Economic Times

- Fed reports balance sheet assets of $2.67T on Wednesday, +$16.8B w/w and +$326.8B y/y

- Broadcasters ask CRTC to look at regulating Netflix - Globe & Mail

- Dunkin' Brands planning a summer IPO, says CNBC's Kate Kelly

- Treasuries rise as the Fed and President Barack Obama consider cutting stimulus measures for the U.S. - Bloomberg

- Groupon may pick Goldman Sachs, Morgan Stanley as lead underwriters for planned IPO later this year, said to value company at $15b-$20b: WSJ

- G-20 finance ministers, bankers meet this weekend in Washington.

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Quest for ‘Holy Grail’ of Super Corn Intensifies on Fertilizer Price Surge

- Oil Heads for First Weekly Loss in a Month Amid Inflation, Demand Concern

- Wheat Declines, Erasing Advance, as Russia and Ukraine May Add to Supply

- Copper May Fall for a Fifth Day as Record Chinese Output Increases Supply

- U.S. Probably Won’t Repeat Last Summer’s Record Heat, Forecasters Predict

- Sugar Falls on Brazil Production, Reduced Goldman Forecast; Coffee Rises

- Gold Is Little Changed After Reaching Record on Global Inflation Concern

- Copper Production in China Climbs to a Record on Higher Fees After Quake

- Orphanides Says Not Clear Price Pressures From Commodities Will Fade Soon

- K+S Bets on Higher Potash Prices on Demand as Investments Constrain Growth

- Toyota’s Molten Aluminum Turned Into Lump Shows Post-Quake Power Challenge

- Commodity Trading Rules Are a Target for Worldwide Securities Regulators

- Oil May Rise Next Week on Mideast Unrest, Saudi Output Cuts, Survey Shows

CURRENCIES

EUROPEAN MARKETS

- Moody's downgraded Ireland to Baa3 from Baa1; outlook negative.

- Greek government will decide today on additional measures to cut its deficit.

- Eurozone March final CPI +2.7% y/y vs consensus +2.6% prior revised to +2.4% from +2.6%

- Eurozone March final CPI +1.4% m/m vs consensus +1.3% and prior +0.4%

ASIA PACIFIC MARKTES:

- Asian stocks were mixed as inflation and growth accelerate more than estimated in China.

- The Chinese central bank may boost reserve requirements for lenders as early as today - Bloomberg

- Inflation in India also exceeds estimates at 8.98%.

- China Q1 GDP +9.7% y/y vs cons +9.5%; March CPI +5.4% y/y vs cons +5.2%; March PPI +7.3% y/y vs cons +7.2%.

- Japan revised February industrial output +1.8% m/m vs initial +0.9%.

MIDDLE EAST

Howard Penney

Managing Director