Cracker Barrel is, in my view, the most susceptible of all restaurant concepts to the demand destruction that is caused by elevated gasoline prices. We charted CBRL traffic trends versus miles driven in our post on 4/12. Today, the Hedgeye Energy team produced a telling chart today showing that gasoline prices are looking a lot like 2008.

If gasoline consumption trends are rolling over, the miles driven statistics will follow. CBRL has struggled to generate significant traffic growth for some time now. From the second quarter of this year, it should slow even further. At the very least, it’s difficult to argue that CBRL will see the pick up in traffic that the concept needs. A combination of inflation and slowing same-store sales is not what we are looking for in today’s environment.

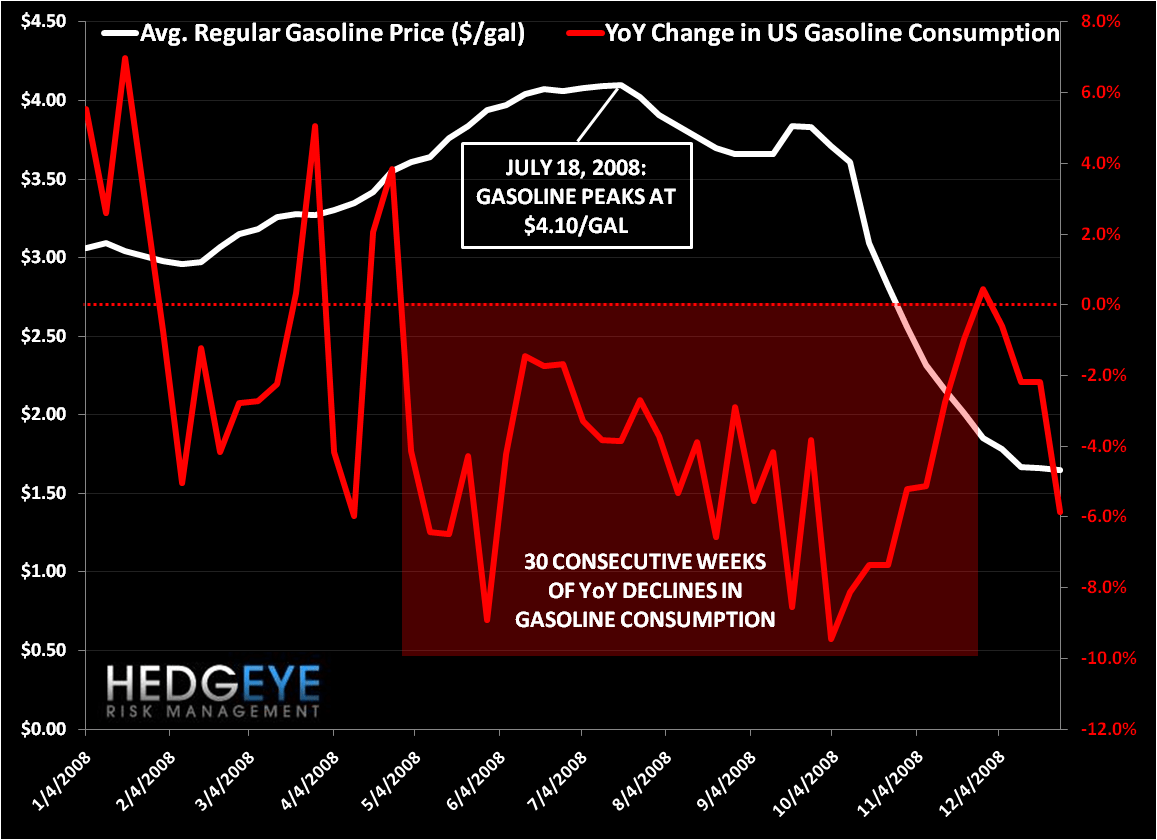

The following come from the Hedgeye Energy team in today’s note titled, “GASOLINE CONSUMPTION SHOWING EARLY SIGNS OF A 2008 REPEAT”:

MasterCard Advisors reported this week that US retail gasoline stations sold 9.02MM b/d of gas in the week ending April 8th – a 3% drop year-over-year. It was the six straight weekly year-on-year decline, indicating that demand destruction as a result of higher prices has set in, and it is eerily similar to 2008.

In early May of 2008, with the price of Brent crude oil near $110/bbl and the regular gasoline at $3.60, gasoline consumption went decidedly negative for 30 straight weeks. During that time (May 2008 – Nov 2008) the price of Brent crude oil went from $108/bbl in May to its mid-July peak of $145/bbl before crashing to $60/bbl in December. Prices did not find a bottom until February 2009, near $55/bbl.

In fact, in 2008 it was not until gasoline consumption was negative year-on-year for 12 consecutive weeks that oil and gasoline prices peaked and subsequently began their rapid declines in mid-July.

The fact that higher gasoline prices impair demand and economic activity is obvious. What’s not so apparent is the threshold and timing at which it does so. Recent history reminds us of the damage that high energy prices can have on asset prices. With gasoline consumption negative for six straight weeks and the average price of a regular gallon of gas at $3.79, the spring of 2011 is beginning to look a lot like the summer of 2008…

Howard Penney

Managing Director