TODAY’S S&P 500 SET-UP - April 13, 2011

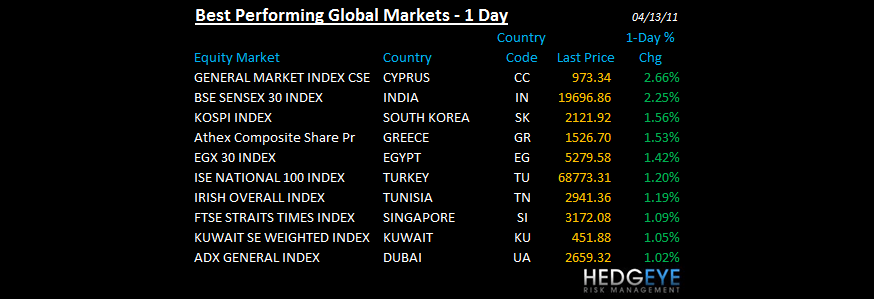

China continues to trade higher, up another +0.96% last night to +8.6% YTD (almost 2x the YTD SP500 return, unadjusted for Burning Bucks) leading what continues to be an improving Asian equity picture (ex-Japan). As global growth slows, unlevered Chinese growth becomes more valuable.

After being bearish/short China in 2010, we’re long now and will focus 1/3 of our Q2 Macro Theme presentation (Friday) on the why. As we look at today’s set up for the S&P 500, the range is 18 points or -0.32% downside to 1310 and 1.05% upside to 1328.

SECTOR AND GLOBAL PERFORMANCE

Two more sectors broke trade yesterday; Energy and Technology. We now have 6 of 9 sectors positive on TRADE and 9 of 9 sectors positive on TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1498 (-318)

- VOLUME: NYSE 949.53 (+15.98%)

- VIX: 17.09 +3.10% YTD PERFORMANCE: -3.72%

- SPX PUT/CALL RATIO: 1.50 from 1.37 (+9.26%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 23.51

- 3-MONTH T-BILL YIELD: 0.05%

- 10-Year: 3.52 from 3.59

- YIELD CURVE: 2.75 from 2.74

MACRO DATA POINTS:

- MBA mortgage applications index fell for third week, declining 6.7% week ended April 8 to lowest in 2 months; Refis down 7.7%; Purchases drop 4.7%

- 8:30 a.m.: Retail Sales, est. 0.5%, prior 1.0%

- 9 a.m.: IMF releases report on global financial stability

- 10 a.m.: Business inventories, est. 0.8%, prior 0.9%

- 10:30 a.m.: DoE inventories

- 1 p.m.: U.S. to sell $21b 10-year notes reopening

- 2 p.m.: Fed’s Beige Book

- 5 p.m.: Fed’s Bullard to speak in St. Louis

WHAT TO WATCH:

- Leonard Green may make bid for BJ’s Wholesale Club today; BJ’s said to ask for opening round proposals this week: N.Y. Post

- China’s debt rating may be cut for first time in 12 years after record jump in lending: Fitch.

- Newsletter writers classified as bears by Investors Intelligence was below 20% for second week in a row. Bullish sentiment declines to 55.4% from 57.3% in the latest US Investor's Intelligence poll

- EU Commission fines Procter & Gamble and Unilever a total of €315.2M in washing powder cartel case

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Sugar Seen Declining as Production in India Set to Climb 5% on Plantings

- Oil Drops a Third Day in New York as Libyan Rebels Consider Truce Proposal

- Soybeans Advance as Biggest Drop in a Month Lures Importers; Corn Climbs

- Copper May Drop for Third Day on Concern About Credit Tightening in China

- Gold May Rebound From One-Week Low as Japan Concern, Libya Add to Demand

- Cocoa May Advance on Ivory Coast Disruption; Coffee Climbs, Sugar Drops

- Equities Trump Gold as Investors' Best Inflation Hedge: Chart of the Day

- China Cotton Buying Slows for U.S. Sellers, Eastern Trading Co.'s Lea Says

- Rio Tinto Iron-Ore, Coal, Uranium Production Declines on Australian Floods

- BHP Isn't Justifying Laggard Woodside's Most Expensive Valuation: Real M&A

- Rubber Futures Tumble as Toyota Set to Suspend Output at European Plants

- Cocoa Arrivals Gain 36% From Brazil’s Bahia Region, Thomas Hartmann Says

- Malaysia Plans Sugar IPO, Postal Sale as State Companies Pledge to Divest

CURRENCIES

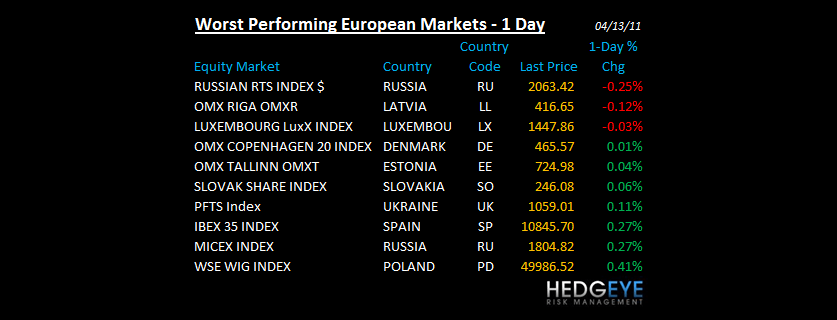

EUROPEAN MARKETS

- Industrial production data for the euro area suggests that the economic outlook continues to deteriorate for the region’s weakest countries; EuroZone Feb Industrial Production +7.3% y/y vs consensus +7.8% and prior revised +6.3% from +6.6%; EuroZone Feb Industrial Production +0.4% m/m vs consensus +0.7% and prior revised +0.2% from +0.3%

- European equity markets trade higher following a positive lead from Asia

- France Mar CPI ex tobacco +0.8% m/m, prior +0.5%

- Germany Mar Wholesale Prices +10.9% y/y vs consensus +10.7%, prior +10.8%

- UK Feb ILO unemployment rate +7.8% vs con +8.0%

- UK Mar claimant count +0.7k vs con (4.2K)

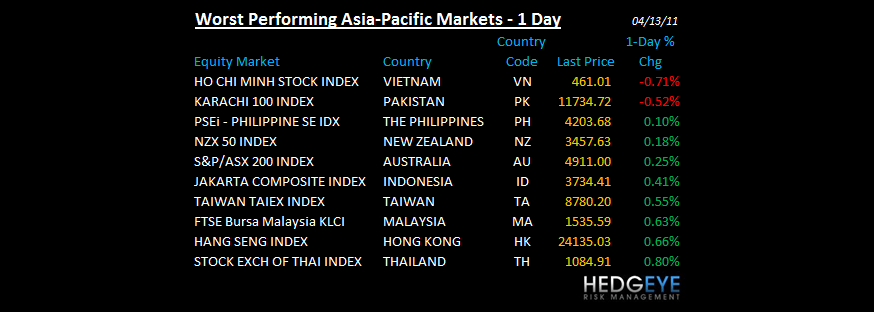

ASIA PACIFIC MARKTES:

- Asian markets rose in the afternoon after seeing limited gains in the morning.

- South Korea and India led the region.

- Vietnam and Pakistan were outliers on the downside.

- Japan March CPGI +0.6% m/m, +2.0% y/y.

MIDDLE EAST

Howard Penney

Managing Director