Positions in Europe: Long British Pound (FXB); Short Spain (EWP)

If nothing else, the European discourse in recent weeks has proven out Keith’s Keynesian Endgame thesis – European leaders will continue to throw money and more favorable loan terms at member countries to prevent the failure of any one country, and therein preserve the structure that unifies unequal countries that share a common currency. This, along with the recent hawkish stance of the ECB and 25bps interest rate hike on April 7th, has been bullish for the EUR, currently pushing against $1.45 versus the USD.

With Portugal’s bailout imminent (in the neighborhood of €50-80 Billion), Greece’s fiscal issues are bubbling back to the surface. This weekend at a meeting of European finance ministers in Hungary, German finance minister Wolfgang Schaeuble re-stoked the fear trade by saying that Greece may need more capital and/or more favorable loan terms to return to fiscal health. The statement in and of itself comes as no great surprise – remember that Greece’s debt as a % of GDP is expected to ramp to 159% in 2012, and we’re of the camp that PM Papandreou and Co. will come well short of their target to reduce the country’s deficit from a high of 15.4% of GDP in 2009 to 3% by 2014 – yet the Greek equity index ATHEX was pounded down a full -2.6% on the news today.

This weekend’s meeting also opened up the prospect of a further restructuring of Greek government debt, with EU Economic and Monetary Commissioner Olli Rehn saying, “We have a solid plan. It is based on a very careful analysis of debt sustainability”. Translation: let’s fill up the trough. And this follows the already generous terms of the country’s €110 Billion bailout, which were amended last month to include repayment in 7.5 years instead of 3 and a cut to the interest rate of 100bps to around 3.5%.

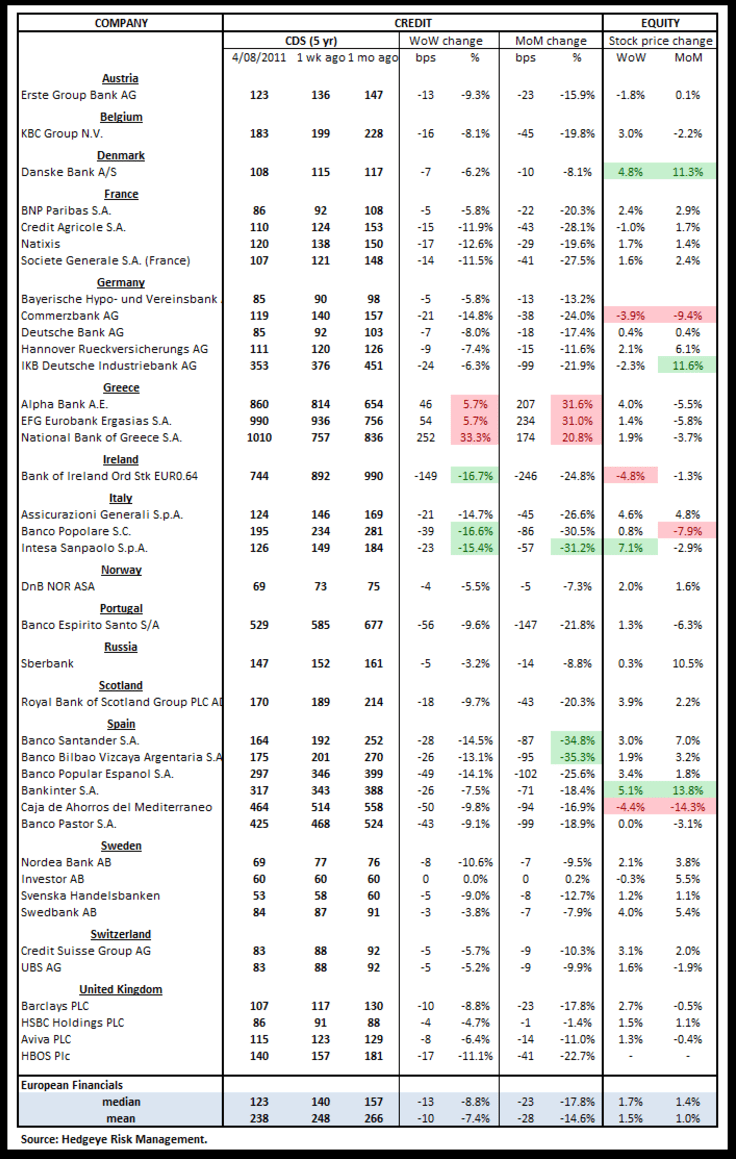

Hedgeye’s weekly European Risk Monitor shows that Greek bank swaps (in particular) pushed higher after improving on the margin last week (see chart below). Sovereign CDS spreads show a near-term downward inflection in risk for Ireland and Portugal, while on the TREND Greece pushes higher as Spain and Italy wane (chart below).

Matthew Hedrick

Analyst