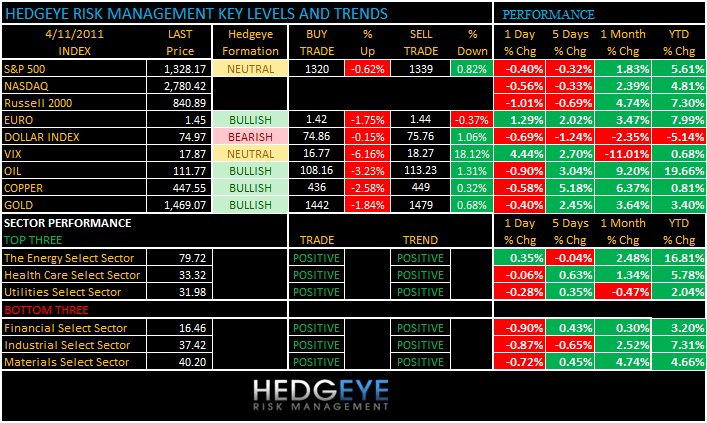

TODAY’S S&P 500 SET-UP - April 11, 2011

Over night the best performing markets are in the Middle East; Qatar and Kuwait up 1.03% and 0.88%, respectively. The IMF is coming around to the Hedgeye view and has lowered its forecasts for economic growth in the U.S. As we look at today’s set up for the S&P 500, the range is 19 points or -0.62% downside to 1320 and 0.82% upside to 1339.

SECTOR AND GLOBAL PERFORMANCE

We are on day 6 of perfect with 9 of 9 sectors positive on TRADE and 9 of 9 sectors positive on TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -966 (-208)

- VOLUME: NYSE 815.79 (-10.06%)

- VIX: 17.87 +4.44% YTD PERFORMANCE: +0.68%

- SPX PUT/CALL RATIO: 1.73 from 1.93 (-10.43%)

CREDIT/ECONOMIC MARKET LOOK:

Treasuries fall as economists estimate that U.S. data will show inflation quickened and Pimco’s Bill Gross set a bet against govt. debt.

- TED SPREAD: 24.73 -0.250 (-1.001%)

- 3-MONTH T-BILL YIELD: 0.04%

- 10-Year: 3.59 from 3.58

- YIELD CURVE: 2.76 from 2.77

MACRO DATA POINTS:

- 11 a.m.: Export inspections (corn, soybeans, wheat)

- 11:30 a.m.: U.S. to sell $32b 3-mo. bills, $30b 6-mo. bills

- 12:15 p.m.: Fed’s Yellen to speak to Economic Club of New York (text, Q&A)

- 4 p.m.: Crop progress (winter wheat, corn, cotton)

WHAT TO WATCH:

- President Obama to deliver major speech regarding deficit reduction this week - Politico

- NYSE Euronext board unanimously rejects NDAQ/ICE offer; reaffirms commitment to Deutsche Boerse combination

- YouTube announces the the initial roll out of YouTube Live, which provides live streaming capablity

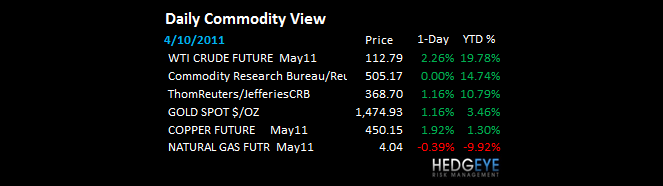

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- China Meat Binge Fuels Iowa-Sized Soybean Imports to Feed 689 Million Pigs

- Copper Erases Gain as Chinese Imports Stoke Speculation Demand May Weaken

- Gold May Slide on Sales After Rally to Record; Silver Reaches 31-Year High

- China Copper Imports Decline 33% on Year as Demand Ebbs, Stockpiles Climb

- Corn Advances to Highest Since June 2008 on Forecast for Shrinking Supply

- Cocoa Climbs on Ivory Coast Fighting; Coffee Declines, Sugar Prices Gain

- Hedge Funds Boost Bullish Bets on Grain, Soy Prices on Increased Demand

- Nickel Demand in China Set to Grow Fastest Among Metals, Antaike's Xu Says

- Alcoa Net May Triple as Aluminum Demand Outweighs ‘Monstrous’ Stockpiles

- Copper Set to Climb 13% to Record, Aluminum to Advance: Technical Analysis

- India May End Wheat, Rice Export Bans on Record Harvests, Citigroup Says

- Milk Shipments Resume From Japan’s Ibaraki as Radiation Levels Decline

- BHP Billiton Douses Speculation of $48.6 Billion Woodside Takeover Offer

CURRENCIES

EUROPEAN MARKETS

- Europe markets are mixed on inflation concerns and the beginning of earnings season.

- German Finance Minister Wolfgang Schaeuble said after a’meeting with EU counterparts at the weekend that it’s unclear whether Greece will need another cut in its bailout rate or a further extension of repayment terms.

- French Industrial Production 0.4% M/m, est. +0.5% (prior +1.0%)

- French Industrial Production 5.6% Y/y, est. +5.2% (prior +5.4%)

- French Manufacturing Production 0.7% M/m, est. +0.7% (prior +1.8%)

- French Manufacturing Production 7.2% Y/y, est. +6.4% (prior +6.8%)

- Italian Industrial Production (sa) 1.4% M/m, est. +1.7% M/m (prior +1.5%)

- Italian Industrial Production (wsa) 2.3% Y/y, est. +3.4% Y/y (prior +0.6%)

- Italian Industrial Production (nsa) 2.3% Y/y, est. +3.9% Y/y (prior +3.8%)

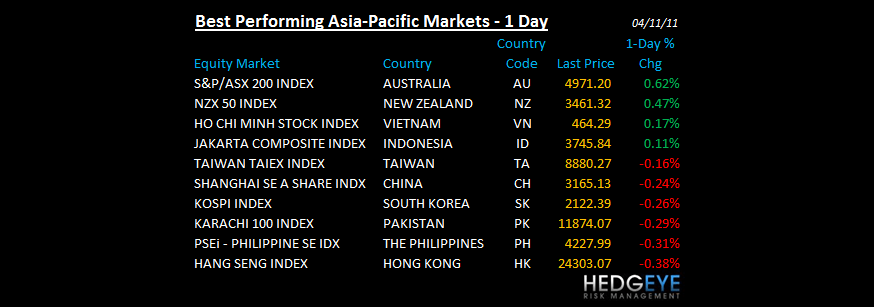

ASIA PACIFIC MARKTES:

- China falls for the first time in 5 days

- Most Asian stocks decline as oil reaches 30-month high and a 6.6-magnitude quake hits in Japan.

- Major markets were closed before the 7.1 earthquake in Japan.

- Japan February core machinery orders (2.3%) m/m vs cons (1.1%).

- China Q1 trade balance ($1.02B) vs year-ago $13.91B.

MIDDLE EAST