Editor's Note: This is a Hedgeye Guest Contributor piece written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.

In my previous essay, I pointed out some disturbing facts about the debt. This essay describes the anatomy of a debt default and suggests the risk of default is real.

A debt default happens when debt holders become concerned about whether the government can meet its obligation to service the debt. This can happen when the cost of servicing the debt gets so large that debt holders begin to fear that the government may not be able to make its scheduled payments. As long as the perception is that the government will be able to service its debt, there is no risk of default.

The cost of servicing the debt is determined by both the size of the debt and the interest rate the government has to pay to service it. If the debt is sufficiently large, some investors might become concerned about whether the government can meet its interest payment obligations even when the interest rate is relatively low. However, a debt default is more likely to happen when the debt is viewed as “large” and the interest rate the government has to pay to finance the debt is high.

In any event, when investors become concerned about whether the government will be able to service the debt, they will start demanding a lower price, i.e., a higher interest rate, to purchase the debt. When this happens the cost of servicing the debt will go even higher, which will cause more investors to be concerned that the government may not be able to service the debt, and the interest rate the government will have to pay to service its debt will go even higher. This will cause more investors to become concerned that the government may not be able meet its payment obligations. This dynamic process can spin out of control unless the government takes action to reduce the size of the debt. Debt default effectively occurs the first time the government fails to meet its debt service obligations on time.

“When is the debt too big?” Many people believe that the debt is too large when the debt is 100% or more of GDP. The federal debt held by the public, FDHP (the debt that investors hold and the government pays interest on) is currently 95% of GDP. By this metric the debt is large. However, there are a number of countries whose debt has been much higher than this for some time without defaulting. Consequently, the size of the debt relative to GDP doesn’t appear to be a sufficient condition for a default.

The size of the debt is a contributing factor, but it’s not the critical factor. Lenders won’t worry about the size of the debt so long as they are confident that the government will be able to meet its interest payment obligations. Hence, the critical factor is the size of the country’s debt service. However, it is hard to know what would trigger investors’ concern about the size of the debt service. Some investors are likely to become concerned when the absolute size of the annual debt service gets large, but large relative to what: Large relative to total government spending or GDP, or as a percent of the FDHP? Investors are more likely to be concerned if the critical measure is “large” and trending larger.

The figure below shows the size of debt service by these three measures from 1981 to 2021. These data suggest that the debt service is currently not a problem by any of these measures. Debt service as a percent of GDP or government spending peaked about the same time; at 3.2% in 1991 for GDP, and at 15.5% in 1996 for government spending. Furthermore, both have been low since 2001 when debt service was 14.6% of government spending and 1.95% of GDP. Debt service as a percent of FDHP has trended down over the entire period.

Nevertheless, there are reasons to believe that debt service will increase significantly over the remainder of this decade. In May 2022 the Congressional Budget Office (CBO) estimated that the FDHP would be $35.8 trillion by the end of 2030. However, the CBO’s estimates have been almost always on the low side even before the Covid-19 spending spree. In January 2007 the CBO estimated that the debt would be $5.4 trillion at the beginning of 2012. It turned out to be $10.4 trillion. One could argue that the CBO’s estimate was off because it didn’t anticipate the 2007-2009 recession and the associated spending. Fair enough. However, in January 2012 the CBO projected the debt would be $14.5 trillion at the beginning of 2020. In fact it was $17.2 trillion as of 2019Q4. This was a period of economic expansion so there is no specific event for this error except that the government spent more than the CBO expected.

The CBO’s estimate for 2030 does not include the spending approved by the $1.7 trillion Omnibus bill President Biden signed into law on December 29, 2022. The $1.7 trillion alone will increase the CBO’s estimate to $37.5 trillion.

Interest rates have increased significantly since May 2022. Treasury rates across the term structure have been hovering in the neighborhood of 4%. The CBO’s debt estimates are based on the assumption that the average rate the Treasury will pay to finance the debt will increase slowly from 1.9% in 2022 to 3.0% in 2030. If interest rates remain about 4%, the annual interest cost of servicing the debt will be much higher.

The average maturity of the FDHP is about 6 years. Hence, one-sixth of debt will be refinanced every year. Debt that was incurred when interest rates were historically low will be replaced with higher interest bearing securities. The CBO’s estimate reflects this fact, but probably not enough.

In May 2022 the CBO projected that the annual interest on the debt will reach $1.2 trillion by the end of 2030. This could happen much sooner. If the interest rate was 3.5%, the interest expense for refinancing the 2022 debt alone by the end of 2025 would be $714 billion; $122 billion in 2023, $237 billion in 2024 and $355 billion in 2025. This, combined with the CBO’s estimate of total deficit spending of $3.7 trillion and the $1.7 trillion in spending passed in December 2022, would add $6.1 trillion to the 2022 debt of $24.3 trillion. This would make the debt $30.4 trillion by the end of 2025. If the interest rate is 3.5%, the interest cost of servicing the debt at the end of 2025 would be $1.1 trillion. Given the CBO’s penchant for underestimating spending, the debt and the costs of debt service could be much higher. It is not difficult to believe that even if spending is no higher than the CBO expects it to be, the FDHP would be $50 trillion or higher by the end of 2030 if interest rates remain high. If this were to happen, the interest cost of the debt service could be about $2.0 trillion annually by the end of the decade.

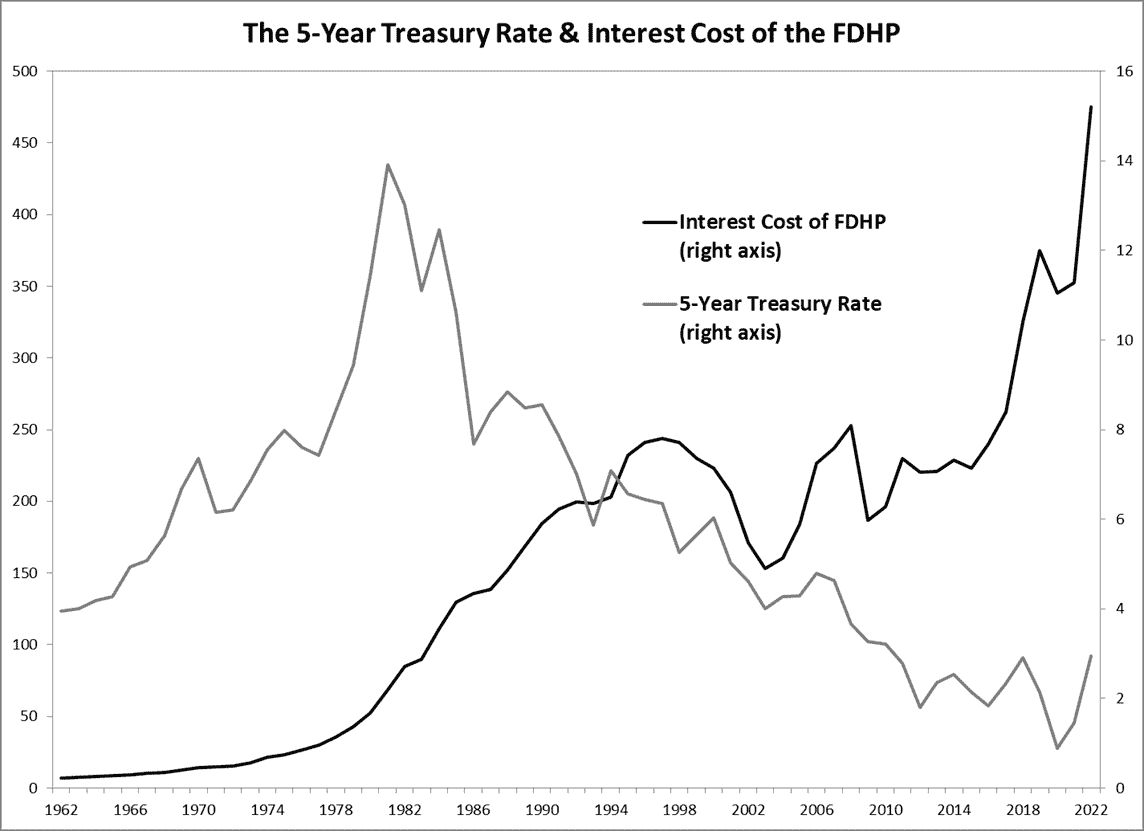

The figure below demonstrates the effects higher interest rates have had on the cost of servicing the debt. The figure shows the 5-year Treasury rate (the right axis) and the interest cost of servicing the debt (the left axis) annually from 1962 to 2022. The figure shows that even though the interest rate was increasing significantly by

1970, the cost of debt service remained low because the debt and deficits were small. The cost of debt service began increasing after 1970 because interest rates and deficit spending were rising. The cost of debt service continued to increase after interest rates peaked in 1981 because the deficit became increasingly larger.

The interest cost of servicing the debt peaked in 1994 and declined until 2003 because, as I noted in my previous essay (here), deficit spending only increased by $188 billion during the eight years of the Clinton administration and because interest rates continued to decline. The interest cost of the debt began increasing with the massive deficit spending under the Obama, Trump and Biden administrations. This occurred in spite of the fact that interest rates continued to decline and were extremely low from 2011 to mid-2022. Of the $9.4 trillion in interest the government has paid on the debt since 1940, nearly half, $4.4 trillion has occurred since 2008. All but $98 billion has been paid since 1962. If interest rates remain high, the debt and debt service will become painful.

Then there is the fact that the Federal Reserve currently holds about 23% of the FDHP. The Fed rebates the interest the Treasury pays on this debt back to the Treasury weekly. Between December 29, 2010, and August 31, 2022, the Fed rebated just shy of $1 trillion to the Treasury. Hence, the FDHP would be nearly $1 trillion higher now if the Fed had not engaged in its large-scale-asset-purchase program, commonly known as quantitative easing (QE). If the Fed were to abandon this program (which it definitely should because it has been completely ineffective, see 2014 and 2017), both the debt and debt service will increase further. For reasons that I will discuss in my next essay, the Federal Reserve currently owes the Treasury $22.4 million because it hasn’t been able to make these payments since September 7, 2022.

Finally, it is extremely likely that the government will commit to more spending than it has up to now. The need to replace aging infrastructure is much larger than the spending proposed in the misnamed Inflation Reduction Act of 2022. Congress suggests this Act will reduce the debt—don’t hold your breath.

Then there is the fact that climate change is going to demand a lot more spending. Also, there are always things, such as Covid-19, wars, financial crisis etc. that no one fully anticipates that will cause the government to spend more than expected. Indeed, some of the largest errors the CBO has made over the last 15 years are the consequence of such events.

I have no idea whether we will get to the point of defaulting on the debt. But it is clear that if Congress and the administration continue on the path they have been on for more than 15 years, default becomes increasingly likely. If the dynamic process described in the fourth paragraph of this essay were to get started, the government would have to make draconian cuts in spending and/or increase taxes dramatically to keep it from spinning out of control.

It is important to note that this dynamic process will be exacerbated if the government attempts to meet its payment obligations by printing money or making deposits to their accounts and/or by financing its spending this way rather than issuing new debt. This method of financing will exacerbate the problem because it will increase the inflation rate. This is what happened as a result of the Cares Act and American Rescue Plan Act which were largely financed this way.

The proponents of what is called Modern Monetary Theory argue financing the debt this way will prevent a default because everyone who holds the debt is getting paid. That’s true. The government is still paying off its nominal debt obligations; if the interest cost is $100, the holder of the debt is getting paid $100 interest. However, the purchasing power of the $100 that is paid is much lower than the purchasing power debt purchasers expected when they purchased the government securities. This is a default in terms of real purchasing power.

It is important to understand that default by inflation could be worse than cutting spending and increasing taxes. The reason, of course, is that inflation hurts everyone, not only those who hold the government debt. Moreover, as I pointed out in a previous CSE Perspective (here) the effects of inflation are permanent for nearly everyone.

In any event, whether the government defaults like this or simply doesn’t make the interest payments, the result is the same—higher interest rates to finance the debt. If this dynamic process is allowed to continue, the government won’t be able to borrow at almost any interest rate. Unlike Greece, no one will be able to bail us out.