This note was originally published at 8am on April 05, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“They would be our shepherds, and we are to be their flock.”

-Frederic Bastiat

After watching Maria Bartiromo interview Chicago Federal Reserve Bank President Charles Evans yesterday into the market close and then watching The Bernank shepherd the financial media into taking his word for it on The Inflation last night, I thought about becoming a sheep.

Or should I rethink my being in this interconnected Global Macro game of risk as a lemming? Perhaps a monkey? Or a donkey? Ah, so many attractive career options are available if I were to accept the wishes of the overlords of the Keynesian Kingdom and become a member of The Fiat Flock…

Born in France in 1801, then orphaned at the age of 9, Bastiat penned the aforementioned quote when he wrote “The Law” in 1850. Not surprisingly, his work wasn’t well regarded by the French Socialists of his time. Neither was it promoted by Charles de Gaulle in the 1950s when his debt-financed-deficit-spending and devaluation programs destroyed both the franc and French credibility in global markets…

During days when the General-in-Chief of the US Federal Reserve (Bernanke) is more left leaning and socialist than the ex-Finance Minister of France turned head of the European Central Bank (Trichet), I think it’s worth taking a moment this morning to consider America’s constitutional definition of liberty as an alternative to this wanna be Centrally Planned world.

The Bastiat Questions (“The Law”, page 46):

“The pretensions of organizers suggest another question, which I have often asked them, and to which I am not aware that I have ever received an answer: Since the natural tendencies of mankind are so bad that it is not safe to allow liberty, how comes it to pass that the tendencies of the organizers are always good? Do they consider that they are composed of different materials from the rest of mankind?”

The Implied Answer (“The Law”, page 46):

“They have, therefore, received from heaven, intelligence and virtues that place them beyond and above mankind: let them show their title to this superiority. They would be our shepherds, and we are to be their flock.”

So how do you feel about that? How do you feel about American central planners debauching the longstanding entitlement we’ve had to the definition of a “free market” system? What’s so free about a market whose every breath of weaning volume depends on The Bernank’s heavy hand?

It’s sad to watch.

Back to this morning’s Global Macro Grind…

The Top 3 headlines this morning are:

- “UConn beats Butler for the National Championship”

- “Texas Instruments To Buy National Semiconductor”

- “Bernanke Says Fed Must Monitor Inflation Extremely Closely.”

Great news for UConn and National Semi – but what’s up with The Bernank? What exactly does monitoring inflation “extremely closely” mean? Were our shepherds monitoring The Inflation somewhat closely before food prices hit all-time highs?

I don’t know how else to say it, so I’ll say it like the Chinese just did this morning by addressing The Inflation head on and raising China’s benchmark interest rate. If we’re not going to address reality about oil at $108/barrel, a new leader in the global financial system will. Don’t think for a New York minute that China didn’t do this in Bernanke’s face this morning for a reason.

China waited on Ben Bernanke’s speech to The Fiat Flock in Georgia last night. This what he said:

“So long as inflation expectations remain stable and well anchored… the increase in inflation will be transitory”

No, dear hard working red-white-and-blue-collared Americans, I couldn’t make that quote up if I tried. Yes, Bernanke makes up his own “forecasts” about matters like growth and inflation all of the time – and, yes, his forecasting track record speaks for itself. It’s terrible.

On Growth:

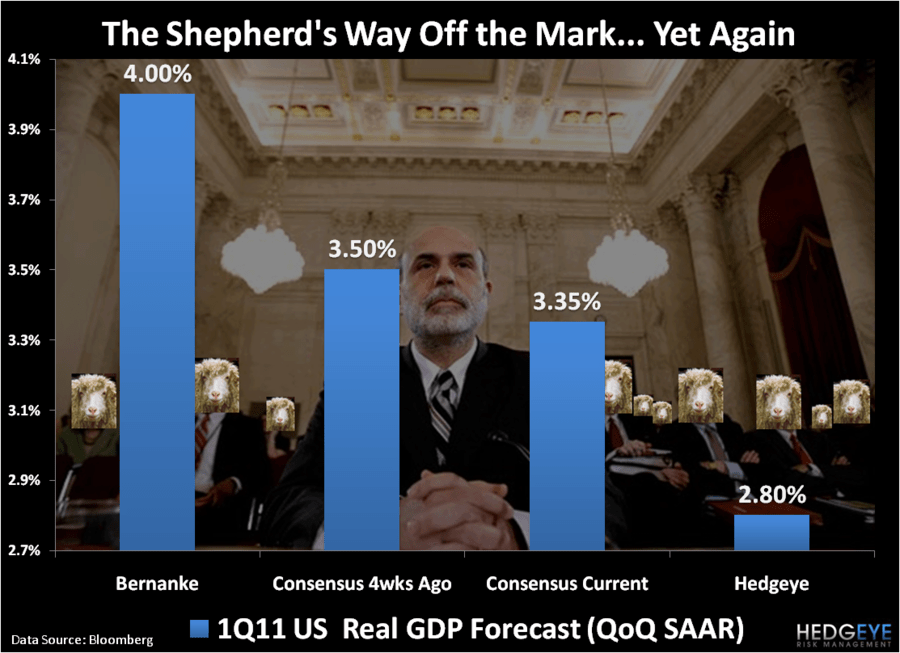

- Bernanke is still forecasting 2011 US GDP growth of 4% to Infinity and Beyond…

- The Street, including both Goldman and Bank of America, is cutting GDP growth estimates closer to the Hedgeye estimate

On Inflation:

- Bernanke calls inflation expectations well anchored and prices “stable”

- The Market, including Commodity and Volatility prices, is flashing the highest food prices and gyrations in price volatility, ever…

As we like to say at Hedgeye, Mr. Bernanke, ever is a long time…

There has never been a Federal Reserve Chairman who has overseen more Americans on food stamps (44 million people and counting). There has never been a Federal Reserve Chairman who has overseen 3-week explosions of price volatility (VIX) on the order of +40-60%, and then draw downs to higher-lows that are the most expedited in market history (7 days in March = VIX down -41.6%).

We are not your Fiat Flock. We do not trust your “forecasts.” And we want our markets back.

My immediate-term support and resistance lines for WTI Crude Oil are $105.91 and $108.92, respectively. My immediate-term support and resistance lines for the SP500 are now 1318 and 1341, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer