Overall, there’s probably not many analysts/PMs out there who are short/underweight Retail that are not scratching their heads wondering what they’re missing, and why today’s sales are so strong. If they’re not asking that, then they’re being intellectually dishonest.

We’ve spent the past few hours debating, crunching, and thinking about what all this means. And at the end of the day, we’re sticking to our guns that retail will roll meaningfully in 2H (actually, with margin pressure becoming apparent in June).

Yes, there was definitely an overwhelmingly high number of beats relative to expectations. But there’s a lot of factors at play…

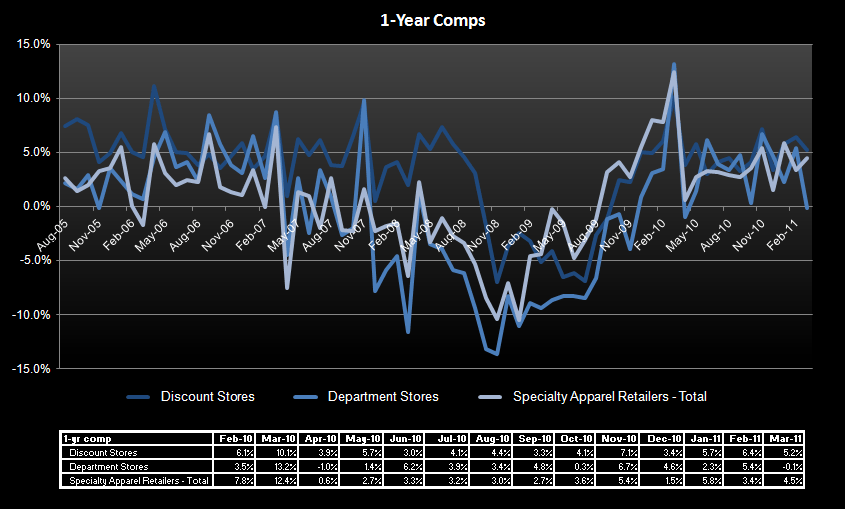

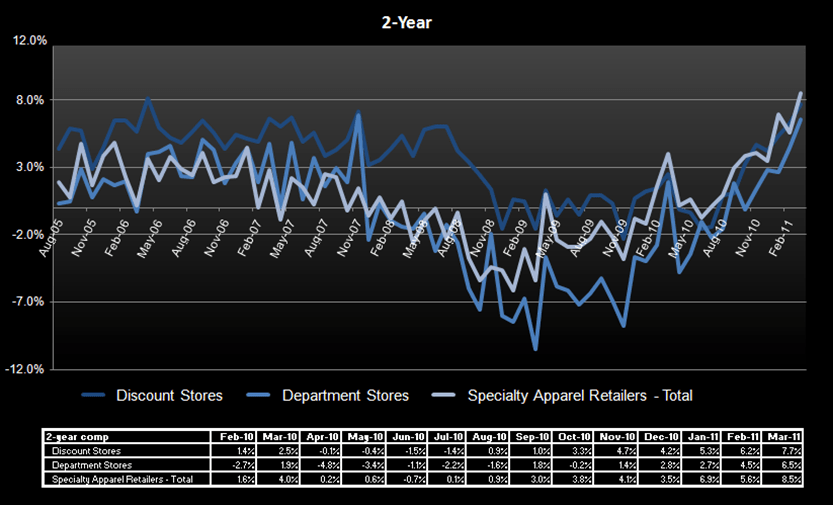

1) Sample size: Let’s not forget that over the past year, the number of companies represented in the sample went from 33 to 23 – and because one of those companies is Wal-Mart, we’ve seen $260bn in revenue go silent. Look at it this way, we have a $14 trillion economy with a 73% consumption rate – so about $10.2 trillion in PCE. Wal-Mart’s US sales account for about 2.6% of that. Better yet, WMT accounts for 7.1% of all dollars deployed at retail in the US.

2) Target didn’t exactly knock the cover off the ball. It beat expectations by 90bps, but still printed a (-5.5%) comp, as strength in consumables and Home was offset by weakness in/mix shift away from apparel and footwear.

3) COST continues to confirm our view on inflation with both fresh foods and food and sundries still up in the LSD range while meat and produce increased reflecting MSD inflation. In addition, gas contributed +3% and +7.5% to SSS for both COST and BJ respectively. Our view is that while this won’t be the first or second crack in the retail industry’s margin equation, it will add to the pain as the retailers choose to capture consumables inflation costs at the expense of discretionary product margins. (i.e can’t take up price on milk, eggs, and chicken – so look to extract margin in categories like underwear, shirts, toys, etc…).

4) There’s no doubt that higher-end products and brands are outperforming. Not a shocker. JCP -0.3, Macy’s +0.9%, Nordstrom +5.1%, and Saks +11.1%. This is definitely a positive for Ralph, and to a lesser extent Guess and PVH.

5) Mesh that with another major undisputable fact…after drawing working capital down to the lowest level in the history of modern day retail, we need to start to see inventory flow into – and then out of – the system in order to allow any of these companies to grow sales. I don’t think anyone would dispute that Gross Margin variability is headed higher – but companies won’t talk about that when their most important month of the quarter is left to go. While this will be more of an issue in 2H, it is likely to be a factor this quarter as well.

So now what?

We’ve got another month of meaningful acceleration in sales. Who’s going to short retail after we saw a seemingly inexplainably strong March, and should see a better than 1,000bp ramp in April? Well… I might. But then in May we get the deceleration and it is on product that has a higher cost embedded in the margin. Then a month later the consumer runs out of QE2 support. Our financials analyst, Josh Steiner, noted this morning to clients how history shows that the end of any period of quantitative easing has put the brakes on improvement to the employment picture for an average of 5-6 months. We have no reason to think it will be different this time around.

That means that we either need wage improvement to drive income, which we’re not going to bank on.

That leaves us with two remaining levers to boost personal consumption – taxes and savings rate. Taxes are sitting at about 9.5% now, one of the lowest levels on record. Yes, that sounds so low, and most people reading this wish they could have this rate. But math is math. Even if you argue that the government understates the tax numbers (why not? They have no problem misrepresent other numbers – like the CPI ) at least give them the benefit of the doubt that they consistently misrepresent it. The latest trajectory is near trough, and it’s probably not going any lower.

If there’s one area where we think we could be wrong, it’s with the personal savings rate. It’s crept up to 5.6% from close to zero over the past few years, and this is a direct trade-off with consumption. Could the consumer draw down savings in 2H and be sitting there with no savings, but still be spending? Yes. We’re Americans. That’s what we do. But the savings rate came down over time as interest rates came down, which has obvious implications for purchasing power. With rates today sitting near zero, it scares me to think of what the consumer environment will be later this year if we’re right with our thesis, and the consumer draws down savings back towards zero while interest rates have nowhere to go but up.

I work in an office of hockey heads. But I think the scenario I just described is like ‘pulling the goalie.’

For all these reasons, I’m a seller into strength over the next two months. Favorites include LIZ, PSS, FL, ROST, RL. Least Favorites: WMT, TGT, CRI, JNY, JCP.

Additional SSS Callouts:

- The strongest performing categories were food/grocery (TGT, COST), women’s and men’s apparel (KSS, COST), and home (ROST, KSS, TGT). On the contrary, softness in footwear was highlighted by several retailers (KSS and TGT) given its sensitivity to the Easter shift.

- Weekly trends were consistently stronger throughout the month with the weakest results in week 5 due to the Easter shift. The one notable exception is COST, which realized a +1-2% benefit from the shift and extra day in March compared to the rest of companies that expect the tailwind in April.

- Given the importance of April to Q1 results, there were few changes to corporate Q1 outlooks with three exceptions: 1) Macy’s, which increased its April comp outlook following stronger than expected March sales and a tailwind of both shift and a planned cosmetics promotion; 2) ROST, which expects to come in ‘somewhat above’ initial Q1 EPS guidance; and 3) Gap, which took Q1 EPS down by $0.04 to reflect events in Japan.

- COST continues to confirm our view on inflation with both fresh foods and food and sundries still up in the LSD range while meat and produce increased reflecting MSD inflation. In addition, gas contributed +3% and +7.5% to SSS for both COST and BJ respectively.

- JCP noted that inventories remain in-line with expected sales trends, though they did sneak in that they saw higher volume of clearance merchandise – suggesting possible margin pressure. They did comment, however, that the Liz Claiborne product is performing ‘exceptionally well.’

- Consistent with recent results, ROST highlighted that pack-a-way still accounts for roughly 47% of total inventories while consolidated inventories increased 35% up from 27% in February. We continue to expect that higher pack-a-way to provide a margin benefit in the 2H.

- From a regional perspective, performance was strongest in the Southeast and SoCal (COST, BJ, KSS, TJX, TGT) and weakest in the Northeast (GPS, TGT, TJX).