We have two months of sales noise until we see the extent to which the masters of our economy have pulled the goalie. Calendar shift provides some ground cover (i.e. excuse). Then the choice between growth, gross margin sustenance, both, or none of the above will become apparent for each retailer.

Not too many people will dispute that sales will take a hit when the 16 companies left that actually report same store sales print their numbers. The biggest factor is the Easter shift, which was very meaningful this year versus last (it was April 4 last year, and is April 24th this year).

By our math, last years’ spike accounted for roughly +11% growth in comps. If we get aggregate numbers in the (-1%) range for March 2011, we’d be looking at a steady rate of about +5% in the 2-year trend, and +1% in the 3-year (which we find most relevant). Anything below that, we’re going to be looking at a deceleration a month or two before we’d otherwise expect to see it.

Putting on our Historical Macro Hat

Let’s put our Macro hats on for a minute and not worry about a couple months worth of timing, or whether jeggings are still ok to wear this Spring. Take a longer look at two key components of consumption: 1) Taxes, and 2) the Personal Savings Rate.

Let’s go back a few decades to 1947. As you see, for the better part of 40 years, they moved in tandem – for the most part. Consumers felt good, they got a good return on their cash (even if sitting idle in a bank account), so not only did they save a greater proportion of income, but did so while taxes went higher. Then that relationship started to break down in 1985, and was completely polar by the 1990s.

We’re not trying to give a history lesson. Everyone knows these numbers, as well as the political and economic forces that drove them. But today, we’re looking at the personal savings rate of 5.6%. There has been only three times since 1991 where it was higher – and those were all over the past six months).

As it relates to the Personal Tax Rate, it stands at 9.5%. There has been only five periods since 1949 where it’s been this low.

So from a Consumer analysts’ perspective, we’re stuck with a near 20-year (close to a generation) high savings rate even though Bernanke and Geithner give virtually zero percent interest on our cash. Other countries are unceremoniously unloading US Dollars. And our collective tax rate is sitting near all time low. The government probably can’t cut taxes any further, and mathematically they can’t take interest rates down enough to matter. What’s going to stimulate the Consumer???

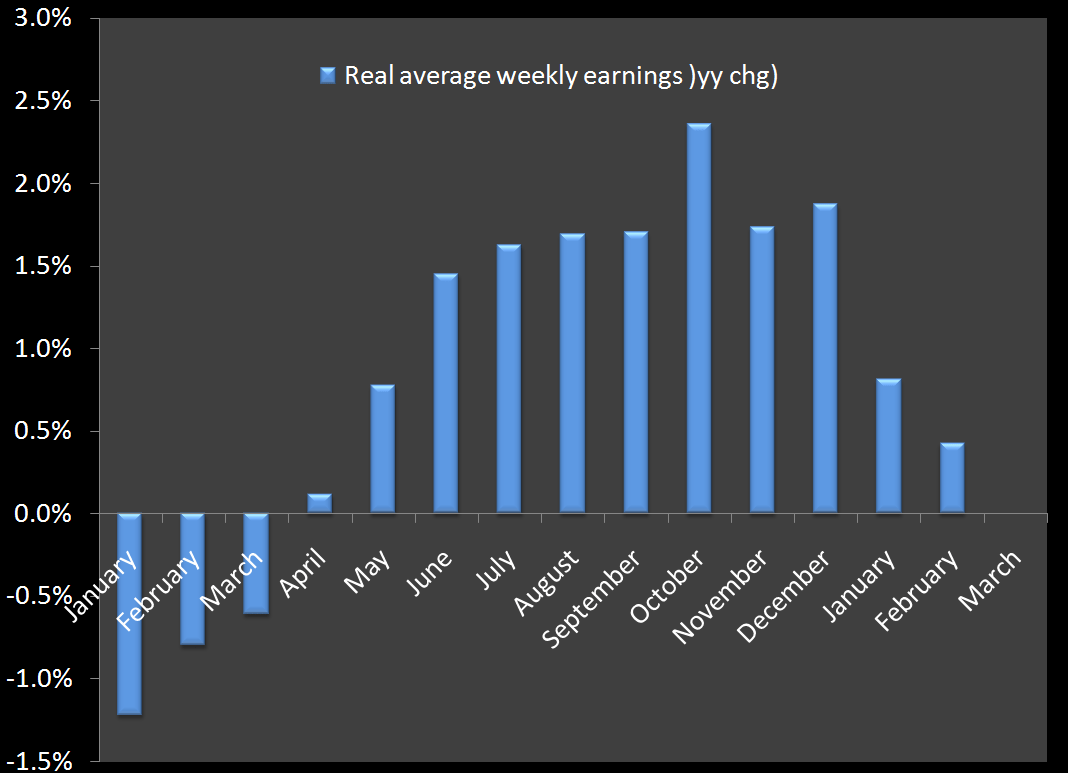

Employment and wage growth is one of the answers, no doubt. The chart below is particularly noteworthy, which shows the year/year change in real average weekly earnings. At risk of stating the obvious, come May/June we’ll really geta solid glimpse into the Consumers’ earnings power, and whether that is translating itself into enough Gross Margin dollars to offset cost inflation (keeping in mind that it is about the April/May timeframe that the higher costs begin to flow through financial statements).