Texas Roadhouse is not a vehicle we would recommend to play the long side of the steak category.

TXRH is currently trading at a premium multiple on a cash flow basis. 8.2x EV/EBITDA NTM is the third highest multiple in casual dining, trailing only BJRI and DIN. I hold a negative view of the stock from here.

The primary negative factors for the stock are as follows:

- 65% of the company’s commodity costs are locked for the year (80% of beef needs) but significant exposure remains in diary costs in particular. While dairy costs came down significantly over the past week, the commodity markets remain volatile and there is significant risk that the company’s guidance of 3% food inflation for the year 2011 will prove conservative.

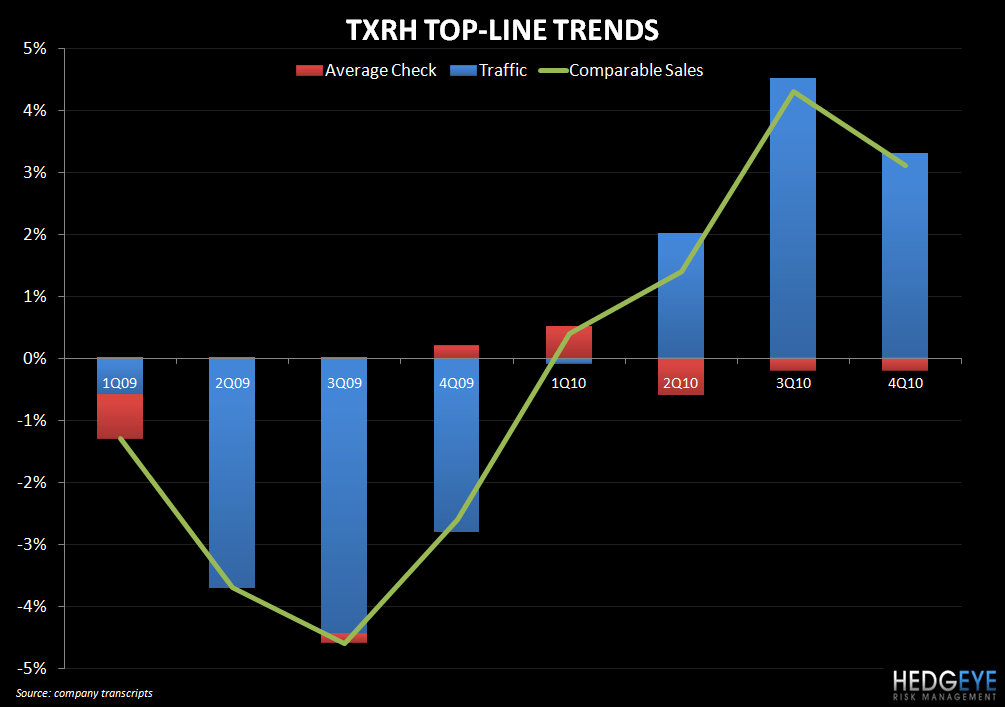

- TXRH has been performing well from a top-line perspective. However, traffic compares get increasingly difficult over the next three quarters and, while optimists may point to top-line outperformance as evidence of some room to add price to the menu, a combination of a step up in price and tough traffic compares could spell trouble for the TXRH top-line.

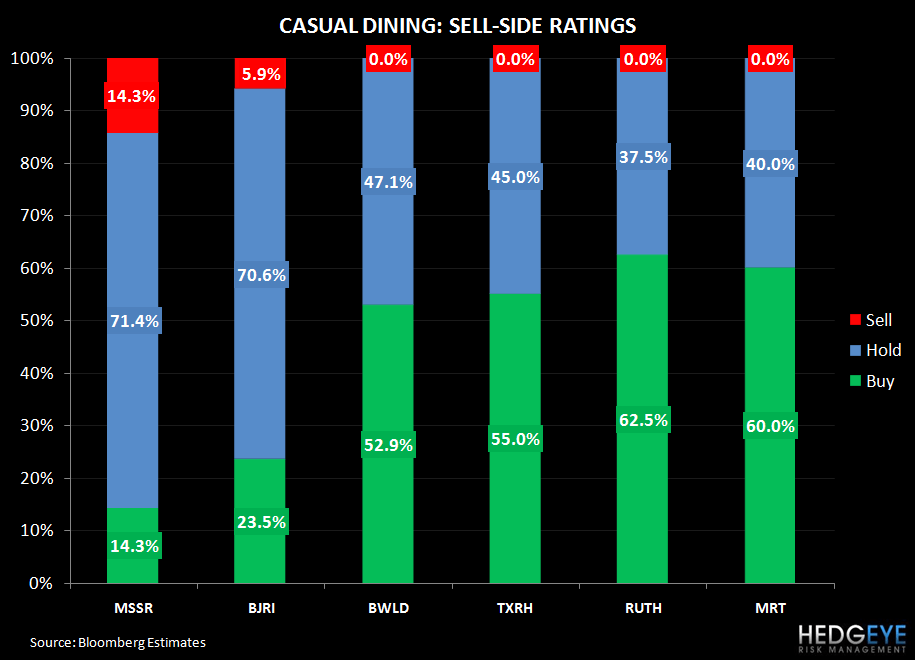

- As mentioned earlier, the stock is trading at a lofty multiple which, I believe, is too high given the alternative plays on the space (RUTH at 5x cash flow) and the stock’s less-than-certain outlook. While there is a strong divergence between the valuation of RUTH and TXRH, the respective sell-side ratings around the stocks (as the second chart below indicates) are much the same.

- I am also unsure of the effectiveness of the Leader of the Door strategy being implemented at TXRH restaurants to improve wait times. While management maintained their enthusiasm around this initiative at the most recent Analyst Day in New York, how exactly this will play out remains to be seen.

- The TXRH core customer is sensitive to gas prices and it seems that Texas Roadhouse could feel some top-line pain from the current level of prices at the pump. Commentary from DRI CEO Clarence Otis on the most recent Darden earnings call regarding the impact of gasoline prices on casual dining revenues highlighted how acute of a concern gas prices are.

Howard Penney

Managing Director