It’s not surprising that RUTH was one of best performing restaurant stocks next to MSSR yesterday. As luck would have it, I have been spending some time on the RUTH story and the risk-reward from here is favorable.

Trading at ~ 5.0x EV/EBITDA, there is nothing but skepticism in the stock. Given the company’s exposure to higher prices for red meat this is understandable, but negative expectations appear to be priced in.

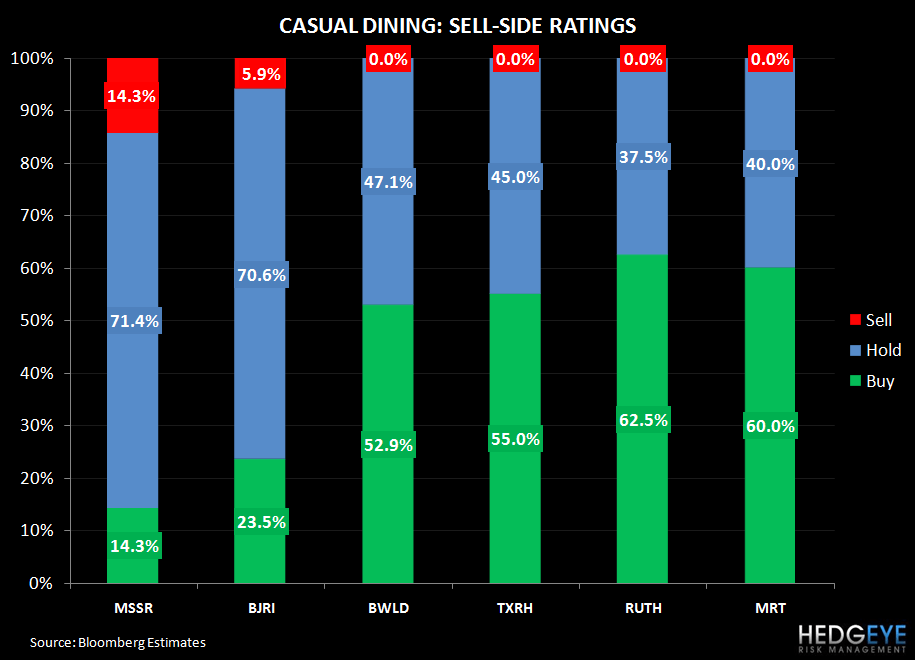

Yesterday, Tilman’s bid for MSSR was a telling sign. For the right operator everything has its price, no matter what the fundamentals look like. As a public company, MSSR has been a disastrous stock. As a private company, the new owners can potentially implement the changes necessary to drive incremental profitability and not worry about quarterly earnings. While no all companies are susceptible to these same issues to a greater or lesser degree, I believe RUTH is more resilient in the current climate given the franchise store base the company maintains.

Beyond the obvious industry related issues, one negative (but could also be a positive) is that the stock is closely held. Management has skin in the game owning 22.7% (including the 19.7% owned by Bruckmann, Rosser, Sherrill & Co). Another 17% is owned by the three largest shareholders. While this can create some liquidity issues it is also creating inefficiencies in valuation.

CURRENT SALES TRENDS

As of RUTH’s 2/18/11 conference call, January's same store sales were up mid-single digits at Ruth Chris according to management. I estimate that Ruth Chris comps increased by between 4 and 5% in January and trended roughly level throughout the quarter. In 4Q10, Ruth Chris’ two largest markets, California and Florida, were up 9.3% and 7.8% respectively. Nearly every company-operated restaurant is producing positive comps (nearly all traffic) as the company has not raised prices recently. Management said that Mitchell’s remained negative, in the mid-single digit range – which I estimate to be -2% to -3% - in January. The weakness at Mitchell’s was driven by the soft Florida market, where sales were down 10.6%, while all other markets improved for the brand.

Within the Rut's Chris’ franchise system, domestic comparable franchise-owned same-store sales increased 8%, while international same-store sales increased 15.5%.

FROM PLAYING DEFENSE TO PLAYING OFFENSE

Up until 2011, RUTH’s senior management has had to play defense, burdened by a leveraged balance sheet into the teeth of a major recession that brought a violent snap-back in consumption levels. For the past 18 months there has not been any unit growth, management has cut G&A and taken much-needed steps to deleverage the balance sheet. In February 2010, Bruckmann, Rosser, and Sherrill made a $25 million investment in preferred stock and concurrently followed that with a $25 million rights offering, issuing 10.2 million shares. In aggregate, those two transactions allowed the Company to pay down $44 million on its credit facility.

With the balance sheet issues now in the past, the focus can turn to more efficient operations and unit growth. One of the potential catalysts for the stock over the next six months is the reacceleration of unit growth. Once growth stops, it generally takes a chain like Ruth Chris approximately 18 months to recommence the expansion of their restaurant base. Currently management is working on filling the Ruth's Chris unit pipeline for 2012 and beyond. The company is less focused on standalone units, but instead cited growth with an emphasis on the gaming and hotel industries as key for the 2012 and 2013 growth pipeline. Currently, the company does not have not have any formal development agreements in place. In 2011, RUTH can expect up to three potential franchise openings in 2H11.

MARGIN TRENDS

The biggest risk to the RUTH story is the uncertainty surrounding margins on a go forward basis. As of the end of January, RUTH has not locked in pricing for their 2011 beef needs. During fiscal 2010, RUTH purchased more than 60% of the beef it used from one vendor, New City Packing Company, Inc. I suspect that New City Packing does not want to take the other side of the RUTH trade and lock in a price. This could be an instance of the Bernanke-sponsored price volatility that our Macro team highlights with such frequency.

In 4Q10, beef prices were up 12%, which caused a 140pbs decline in food cost margins. While the company is very cautious about raising prices, they are planning to take a price increase of approximately 0.50 bps in March. Management intends to “evaluate further pricing opportunities as we go through the year.”

The company does not give annual guidance but does outline the following guidelines; Food and beverage costs of 30.5% to 31.5% of restaurant sales, marketing spend 3% to 3.5% of total revenues, G&A expenses of $23 million to $25 million and an effective tax rate of 25% to 30%.

Howard Penney

Managing Director