“Sometimes we stare so long at a door that is closing that we see too late the one that is open.“

-Alexander Graham Bell

Finally, we’re here. This week we’re finally going to see US Professional Politicians face the door that’s closing on their conflicted and compromised careers of debt-financed-deficit-spending. This isn’t the time to give into their fear-mongering. This is going to open he door for a generational opportunity in America. This is great news.

On Friday, the stop-gap bill to keep the US Government open for business expires. With $14,272,778,776,442 in US Debt + another $55,800,000,000,000 in unfunded Medicare and Medicaid liabilities, I say shut these politicians down. The biggest risk to America today isn’t what’s happening in the Middle East or Japan – it’s the 112th Congress.

And no, Mr. Jaime Dmon, we don’t measure America’s risk solely in terms of the price of its stocks and bonds. America is bigger than that. America is a place that puts a higher multiple on liberty than it does the sustainability of your earnings. America is a place where The People who stand up for the truth will be heard.

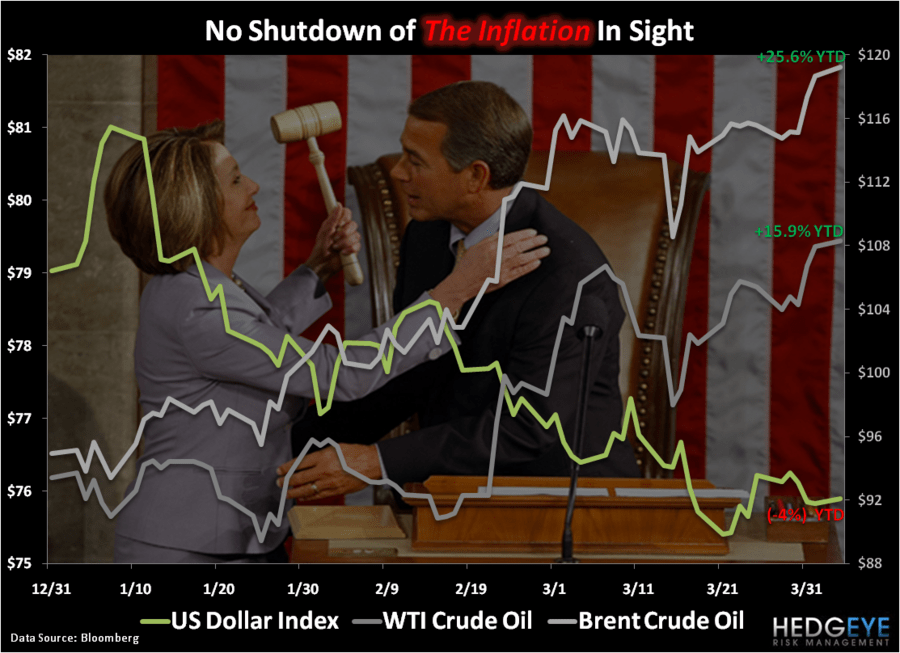

From a fiscal and monetary policy perspective, the sad truth about last week in Global Macro markets was more of the same. The US Dollar Debauchey continued – and, as a result, The Inflation that’s priced in US Dollars pushed higher.

With the US Dollar Index closing down for the 10th week out of the last 14, here’s what else happened to prices week-over-week:

- Euro = +1.4% to $1.42 versus the USD closed out the best quarter that it’s had since it started trading in 1999

- Canadian Dollar = +2% to $0.96 versus the USD and continues to ake higher-highs

- CRB Commodities Index (19 commodities) = +0.3% to 360, testing its highest weekly closing highs since The Inflation of 2008

- West Texas Crude Oil = +2.4% to $107.94, making a fresh 30-month high just in time for your weekend at the pump

- Gold = +0.10% to $1428, closing just a hair inside its highest weekly closing price ever – ever is a long time

- Copper = -3.6% to $4.25/lb as the world comes to realize that Global Growth Slows As Inflation Accelerates

- Volatility (VIX) = -2.7% to 17.41 as month and quarter-end trading volumes slowed to a pay-day halt

- 2-year US Treasury Yields = +9.5% to 0.80% as the politicization in the short end of the curve comes under global pressures

- Yield Spread (10-yr yields, minus 2-yrs) = -7 basis points on the week, upsetting the piggy banker’s net interest margin spread

US Equities ralliedto another long-term lower-high because, well… as Gordon Gekko might say, debt-financed-deficit spending “is good”…

Until it isn’t.

Interestingly, but not surprisingly. It was all good for Greek Equities too … until the Free-Moneys-Forever monetary policy of the European Central Bank (ECB) stopped playing the music.

With the ECB set to raise interest rates on Thursday, Euroe’s currency and interest rates continue to strengthen. This is great news for the conservative Euro dweller who has cash in that old tickle trunk that we old fashioned folks call a savings account. It’s really bad news for the Greek Gekkos out there who are laden with deficits and debts.

Greece’s stock market is down another -2.1% this morning, taking its cumulative swoon to -12.9% since what Wall Street called the “reflation” trade sarted to morph into The Inflation problem on February the 18th. Interestingly, but not ironically, that was the same day that the SP500 peaked for 2011. This should remind us all that what goes up with Big Government’s help, can come down – and quickly.

If you want to look at The Inflation being priced into Global Market prices for the YTD, it’s pretty straight forward: TOP Global Stock Market YTD = Russia +17.2% versusBOTTOM Global Stock Market YTD = Egypt -23.0%.

I know - which one of the affluent American Senators of the Fiat Republic really cares about starving young people in the Middle East or the 44,000,000 Americans (new all-time high) on food stamps anyway? Social revolutions be damned. Obama’s got the guns.

In the US stock market, The Inflation trade continues to be the only one that’s really getting people paid: S&am;P Sector Performance YTD: Energy (XLE) = +17.2% versus Consumer Staples (XLP) = +2.6%.

Of course, everyone on Wall Street and in Washington knows this – we just don’t like to talk about it so plainly. The Inflation is a policy to get the stock market “going” – The Bernank has all but told you that. Now it’s time for us to start dealing with its unintended societal consequences.

In the edgeye Asset Allocation Model, I drew down my Cash position week-over-week. Here are the allocations ahead of this week’s trading:

- Cash 46% (down from 52% last week)

- International Currencies = 27% (Chinese Yuan, Canadian Dollar, British Pounds – CYB, FXC, and FXB)

- Fixed Income = 12% (Long-term Treasuries and US Treasury Flattener – TLT and FLAT)

- Commodities = 9% (Oil and Gold – OIL and GLD)

- International Equitie = 6% (China – CAF)

- US Equities = 0%

That’s right. At this stage of the game, I have the same policy as The Bernank in trusting the 112th Congress with The Inflation – ZERO. That’s marked-to-market with a zero percent allocation to US Equities until the US Dollar stops being debased. If it takes a Shutdown of these professional politicians and the storytelling they employ – so be it. In the long-run, wersquo;ll all be better off with them just stopping what they’ve been doing anyway.

My immediate-term support and resistance levels for the SP500 are now 1314 and 1339, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer