TODAY’S S&P 500 SET-UP - April 4, 2011

Interestingly, but not surprisingly, Inflation Accelerating in Europe has both expectations for an ECB rate on Thursday and the Euro pushing higher. This is not good for debtors (another way to be long The Inflation), and most obviously expressed in Greek stocks. They are down a full -2.1% this morning but, more impressively, down -12.9% since a lot of the “reflation” mean reversion trades peaked on FEB 18th. As we look at today’s set up for the S&P 500, the range is 25 points or -1.38% downside to 1314 and 0.49% upside to 1339.

GLOBAL PERFORMANCE:

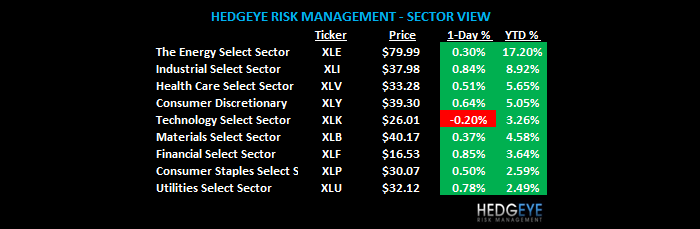

Day 1 of PERFECT; we have 9 of 9 sectors positive on TRADE and 9 of 9 sectors positive on TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1163 (+648)

- VOLUME: NYSE 902.12 (+16.15%)

- VIX: 17.40 -1.92% YTD PERFORMANCE: -2.15%

- SPX PUT/CALL RATIO: 2.22 from 2.10 (+5.58%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 25.03

- 3-MONTH T-BILL YIELD: 0.07% -0.03%

- 10-Year: 3.46 from 3.47

- YIELD CURVE: 2.66 from 2.67

MACRO DATA POINTS:

- 9:05 a.m.: Fed’s Lockhart speaks in West Palm Beach, Fla.

- 9:30 a.m.: Fed’s Evans speaks at Money Smart Week

- 11 a.m.: Export inspections (corn, soybeans, wheat)

- 11:30 a.m.: U.S. to sell $32b 3-mo. bills, $30b 6-mo. bills

- 3:15 p.m.: Fed’s Evans speaks on CNBC

- 4 p.m.: Crop progress plantings

- 7:15 p.m.: Bernanke speaks on clearinghouses and stability in Georgia

WHAT TO WATCH:

- Larry Page takes over as Google CEO today

- Vivendi agrees to buy Vodafone’s 44% stake in French mobile- phone operator SFR for EU7.95b ($11.3b)

- Belgium’s Solvay agrees to buy Rhodia for EU3.4b ($4.8b) in cash, boosting shares of other European chemicals stocks on speculation of more M&A

- President Barack Obama will file Federal Election Commission paperwork for his re-election bid as early as today, according to a person familiar with the planning

- Muammar Qaddafi’s acting foreign minister met with Greece’s prime minister in what Greek govt. described as an attempt to find a political solution to hostilities in Libya. Fighting continued in the besieged rebel- held city of Misrata on Sunday, AP reported

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Copper Seen Rising 18% to Record as Shortages Overcome Weaker China Demand

- Cocoa Seen Dropping 12% Once Fight for Ivory Coast Presidential Power Ends

- Corn Rallies to Highest Since 2008 as Stockpiles Drop, Goldman Sees Record

- Oil Rises to 30-Month High in New York on Fuel Demand Outlook, U.S. Jobs

- Lead Reaches Three-Year High on Speculation Demand Will Gain; Copper Rises

- Gold Advances on Conflict in Libya, Concern About European Sovereign Debts

- Tainted Pork Becomes Latest Inflation Driver for China: Chart of the Day

- Anglo American Will Struggle to Meet Collahuasi Copper Goal After Floods

- China's Minmetals May Need to Raise Its $6.5 Billion Equinox Offer by 29%

- Mitsubishi Materials to Increase Lead Output by 16% on Post-Quake Demand

- Palm Oil Advances, Tracking Gain in Soybeans, Corn on Lower Inventories

- Fight for Ivory Coast's Abidjan Enters Fifth Day, Food Supplies Run Short

- Japan Quake Recovery, Atomic Concerns Drive Demand for Copper, Iron, Beef

CURRENCIES

EUROPEAN MARKETS

European stocks are little changed near three-week highs as losses by financial companies offset takeover bids from Vivendi and Solvay.

MACRO DATA POINTS:

- Eurozone Apr Sentix Index 14.1 vs consensus 16 and prior 17.1

- UK Mar Construction PMI 56.4 vs consensus 54.9 and prior 56.5

- Eurozone Feb PPI +6.6% y/y vs consensus +6.7%

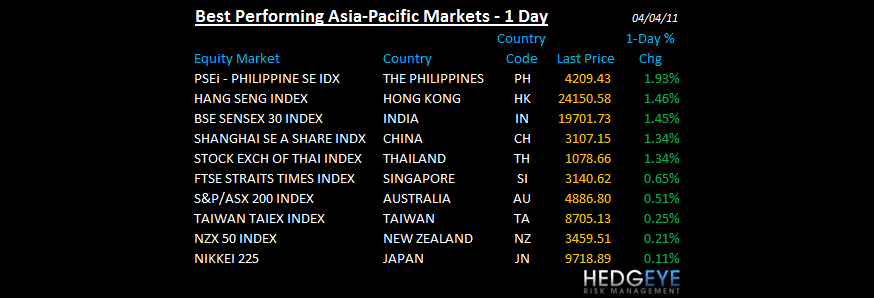

ASIA PACIFIC MARKTES:

The Asian markets turned in a stronger relative performance lead by China up 1.34%

MIDDLE EAST

Howard Penney

Managing Director