“It was a matter in which we have heard some other persons blamed for what I did myself.”

-Abraham Lincoln, 1862

That’s one of the many outstanding leadership quotes in the book I highlighted yesterday, “Team of Rivals – The Political Genius of Abraham Lincoln.” If he wants to get re-elected, President Obama should think long and hard about Lincoln’s example of transparency, accountability, and trust. Rather than giving lip-service to being like the great American leaders who came before him, Lincoln was his own man - and he lived these principles out loud.

Whether you like following politics or not, you need to get the direction of their leanings right if you want to get your Global Macro positioning right. Currency markets move on policy – policy is set by politicians. And while that’s a pathetic and sad statement about our said “free market” system altogether, you can’t get bogged down by it – you need to play the game that’s in front of you.

Currently, the most important game in Global Macro Risk Management is the cross-asset-class correlation-risk associated with what the US Dollar does. If you get policy right, you’re likely to get the US Dollar right. If you get the US Dollar right, you’ll get fewer things wrong.

This is where my only political advice to the President of the United States (or whoever realizes that they could win his office) comes into play – get the US Dollar right (strengthen it) and you’ll Deflate The Inflation. If you Deflate The Inflation, The People will believe in you.

Strong US Dollar Policy isn’t a partisan thing. It’s an American thing. Reagan had it. Clinton had it. Nixon and Carter devalued it. Nixon and Carter also had a Dollar Debauchery man at the Fed named Arthur Burns.

Reagan had Volcker. President Obama has The Bernank.

Obama will be the first to tell you he took on a lot of Bush’s baggage. He’ll be the last to tell you he made a mistake in taking on Bush’s Bernanke. So, Mr. President, let’s strap on the accountability pants, Blame Yourself, and take a walk down that path – because your General-in-Chief on all things US economic policy definitely won’t be doing it for you anytime soon. Some of his Generals in the Fed’s ranks will.

In one of the great 2011 accountability headlines coming out of the US Federal Reserve last night, Kansas City Fed President, Thomas Hoenig, explained the following by effectively blaming himself:

- “Once again, there are signs that the world is building new economic imbalances and inflationary impulses…”

- “The longer policy remains as it is, the greater likelihood these pressures will build and ultimately undermine world growth…”

- “…remember, I’m not advocating tight monetary policy… I’m advocating a non-crisis policy. Zero is a crisis policy that by itself should be temporary.”

Now this isn’t Hoenig’s first rodeo. He joined the Federal Reserve Bank of Kansas City in 1973. He is the longest serving member at the Fed and his 8 consecutive “dissents” (English for publically disagreeing with The Bernank) recently tied Henry Wallich’s 1980 record for most disagreements with Fed policy (Wallich has been validated as being very right). Hoenig is a known inflation hawk – most likely because he faced it in the 1970s and joined Wallich and Volcker in fighting it.

Does the President of the United States really want to test the waters on $120/oil and 1970s style Jobless Stagflation? Does he want to roll the bones on The Quantitative Guessing experiments in Japan gone bad? Does he want to run against someone in 2012 who will crush him like a bug with the simple conclusion that Growth Slows As Inflation Accelerates?

I don’t think so. Remember, he’s a professional politician – after all…

As opposed to someone holed up in a room of academia’s Keynesian Kingdom, I’m in the soup. I’m managing risk in this cross-asset-class correlation-risk game each and every day. I have been writing these morning strategy notes since I started this firm without bailout moneys 3 years ago – and I’ve made 19 calls on the US Dollar since (long and short side) – and I’ve been right 19 times. If you want a USD opinion – at least ours has some credibility.

Call me politically irrelevant. Call me Canadian. Call me names from the heavens, Mr. Big Government Intervention man. But don’t call me a McClellan (1862) in this currency war, because it’s The US Monetary Policy that’s managed by you, the unaccountable generals, at the front of The Inflation lines who are perpetuating the problem.

Back to the Global Macro Grind…

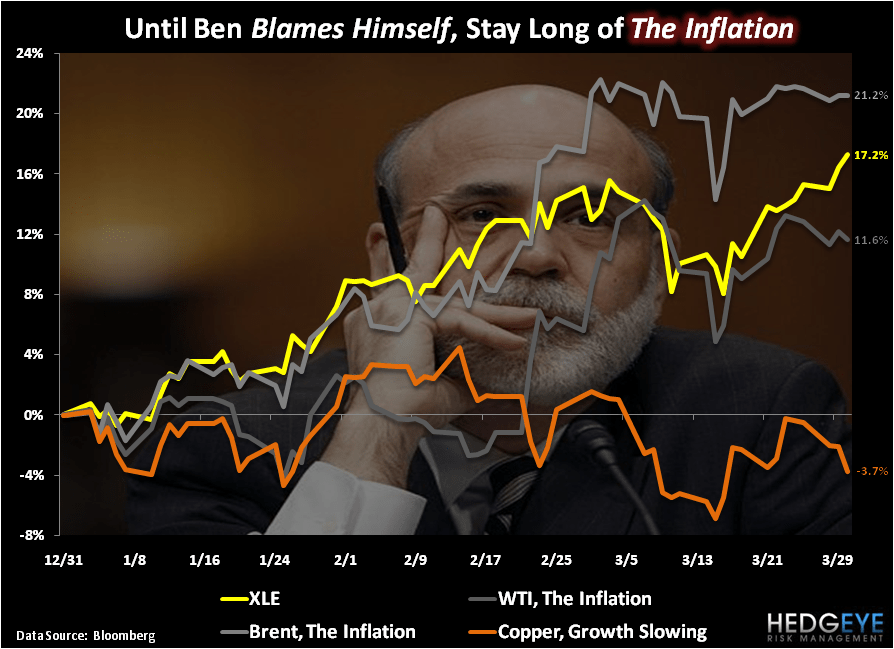

Now that the IMF is cutting their US GDP Growth estimate for 2011 this morning (to 2.8%), I’ll assume that our call for Growth Slowing As Inflation Accelerates is being absorbed into the craws of consensus. The leading indicator that is the price of Dr. Copper remains bearish and broken with intermediate term TREND resistance (which was longstanding support) at $4.38/lb.

Consensus doesn’t mean that Growth Slowing signals don’t continue to flash amber lights – it simply means the 6.5% intra-quarter SP500 correction had more to do with a longer-term global reality (piling sovereign debt-upon-debt-upon debt structurally amplifies inflation and impairs growth) than a tsunami of complacency.

Japanese and Chilean Industrial Production Growth reports for February (pre quake) came out yesterday and both slowed again sequentially. Eurozone inflation (CPI) for March accelerated again, sequentially. And while the US Dollar trading up for 2 of the last 3 weeks has helped Deflate The Inflation this week (bullish for Equities), it looks like that reverts back to the mean of Burning Buck and up oil again this morning. I’m staying long oil and long gold.

My immediate-term TRADE lines of support and resistance for oil are now $102.13 and $107.95, respectively. My immediate-term TRADE lines of support and resistance for the SP500 are now 1305 and 1333, respectively.

Looking forward to seeing everyone at Hedgeye Soho’s launch party in NYC this evening – no government bailout moneys required for us to buy you drinks.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer