The Sisyphean fight that is Bernanke’s refusal to acknowledge reality is becoming more and more apparent to the consumer.

The strong earnings season, positive conflicted government data, and it’s looking more and more like a Bernanke recovery and not a consumer recovery. The fourth quarter of 2010, many have said, confirmed that a consumer recovery was in the bank. Consumer data emerging in 1Q11 is now calling that view into question.

The expectation that the consumer will lead this recovery from start to finish is unreasonable. the support mechanism are not there. Yesterday the government reported that excluding the effects of changes in tax payments and Social Security contributions, disposable income would have risen 0.3% in February and 0.2% in January rather than the 0.3% and 0.8% reported. Consumer prices, as measured by the consumer spending deflator, rose 0.4%, the fastest growth since June 2009. Inflation rising, house price depreciating, and the looming prospect of interest rates increasing are factors that do not point to the consumer staying rock-solid throughout this process.

The consumer has no purchasing power on an inflation-adjusted basis and, when excluding transfer payments, the outlook is very negative. At best, we can expect consumer spending to remain at its current level, but that would imply no meaningful increase in the savings rate or balance sheet repair.

Regulators are also proposing a draft definition of a “qualified residential mortgage” that could, when finalized, preclude all but the most conservative mortgages from being defined as “qualified residential mortgages”. Under the proposed rule, among other stringent conditions, buyers seeking a mortgage to buy a home will be required to put down at least 20%. As our Financials Team wrote this morning, the current version of the definition is expected to be a headwind to the housing market. The current downward slide in home prices and the prospect of a new era of sky-high down payments is disconcerting to say the least.

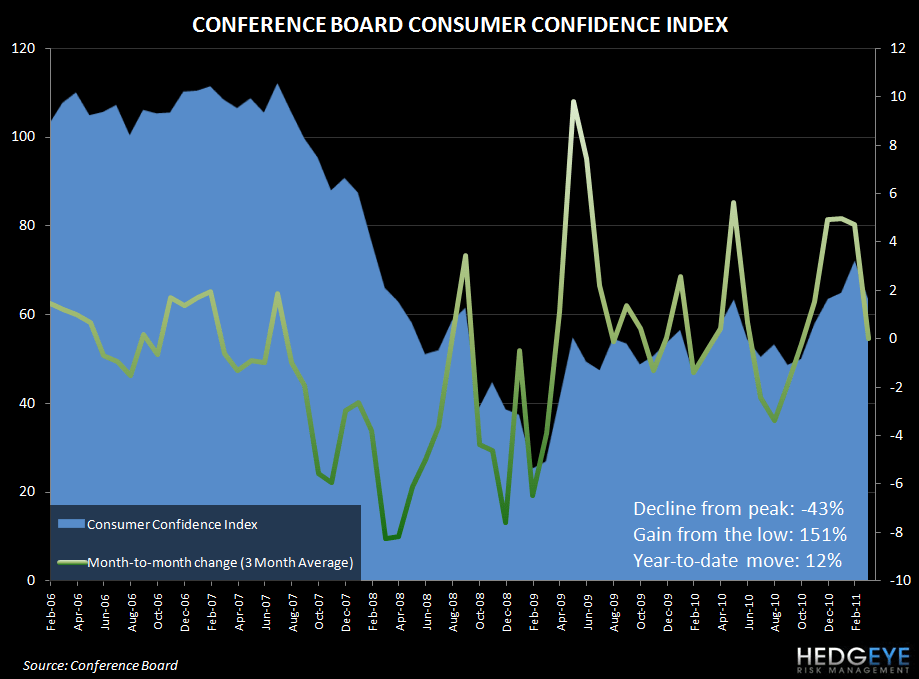

Not surprisingly, the Conference Board reported today that consumer confidence fell significantly in March; reaching a three year high in February. As we have been highlighting in the past few consumer posts, the expectations component is largely driving the overall index and was again instrumental in March as it fell to 81.1 from 97.5 (previously 95.1); the present situation component rose to 36.9 from 33.8 (previously 33.4). Overall, confidence fell to 63.4 from 72 (revised from 70.4).

As Keith alluded to in this morning’s Early Look, inflation is not a positive sign for a market experiencing 30-year highs in corporate margins. The consumer’s margins certainly aren’t at peak levels and the pain is coming through in the numbers.

Howard Penney

Managing Director