TODAY’S S&P 500 SET-UP - March 29, 2011

We are looking at the short end of the yield curve to tell us where the political wind is blowing – that’s where the politicization is – and we’re seeing a huge move higher in 2yr yields here, implying no Quantitative Guessing III (QG3).

As we look at today’s set up for the S&P 500, the range is 31 points or -1.39% downside to 1292 and 0.98% upside to 1323.

PERFORMANCE

As of the close yesterday we have 5 of 9 sectors positive on TRADE and 8 of 9 sectors positive on TREND. The XLU is the only sector to be broken on both TRADE and TREND.

- One day: Dow (0.19%), S&P (0.27%), Nasdaq (0.45%), Russell (0.25%)

- Month-to-date: Dow (0.23%), S&P (1.28%), Nasdaq (1.85%), Russell (0.2%)

- Quarter/Year-to-date: Dow +5.36%, S&P +4.18%, Nasdaq +2.93%, Russell +4.86%

- Sector Performance: Healthcare (0.03%), Consumer Staples (0.03%), Industrials (0.09%), Energy (0.24%), Financials (0.33%), Utilities (0.35%), Materials (0.46%), Tech (0.23%), and Consumer Discretionary (1.04%)

EQUITY SENTIMENT

- ADVANCE/DECLINE LINE: -587 (-1526)

- VOLUME: NYSE 784.29 (-4.91%)

- VIX: 19.44 +8.54% YTD PERFORMANCE: +9.52%

- SPX PUT/CALL RATIO: 1.82 from 1.99 (-8.92%)

CREDIT/ECONOMIC MARKET LOOK

Treasuries were weaker for an 8th consecutive session.

- TED SPREAD: 21.07 -1.724 (-7.567%)

- 3-MONTH T-BILL YIELD: 0.11% +0.02%

- 10-Year: 3.47 from 3.46

- YIELD CURVE: 2.66 from 2.67

MACRO DATA POINTS

- 9 a.m.: S&P/CaseShiller Home Price, est. M/m (-0.44%), prior (-0.41%)

- 10 a.m.: Consumer Confidence, est. 65.0, prior 70.4

- 11:30 a.m.: U.S. to sell $40b in 4-week bills, $35b in 5-yr notes

- 4:30 p.m.: API inventories

WHAT TO WATCH

- Wal-Mart gender bias case arguments heard by the Supreme Court

- News Corp. said to be in talks to hand over control of Myspace to Vevo.com

- U.K. government hosts meeting of foreign ministers in London to resolve differences among coalition partners on Libya

- U.S. district court hearing for GM vs Allied Systems. If Allied systems doesn’t attend may be ordered to release the 1,704 vehicles being held at its facilities

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Rising Corn Acreage Seen Failing to Meet Increased U.S. Feed, Ethanol Use

- Crude Oil Trades Near One-Week Low in New York as Libyan Rebels Make Gains

- Copper Declines for Fourth Day on Concern About Weakening Chinese Demand

- Gold Drops for Fourth Day on Signs U.S. Economic Recovery Is Strengthening

- Corn, Wheat Climb on Speculation Japan May Sustain Imports Following Quake

- Commodity Gains May Exceed Forecast on Japan, Middle East, Goldman Says

- Japanese Rice Imports Are Unlikely to Rise After Quake, U.S. Group Says

- Sugar Gains on Speculation About Curbed Supplies From Brazil; Cocoa Falls

- Corn, Wheat Demand in Japan ‘Resilient’ After Quake, FCStone’s Clancy Says

- Cosco Singapore Says Japan Not Major Destination for Its Dry-Bulk Carriers

- N.Z. Vegetable Exports May Increase on Japan Radiation Concern, Groups Say

- Delta Spars With Morgan Stanley on Proposal to Curb Commodity Speculation

- Copper Will Lead Base-Metals Rally on Shortage, Brook Hunt's Kettle Says

- Rio Tinto Is Said to Discuss Acquiring Riversdale Shares From Brazil's CSNws

CURRENCIES

EUROPEAN MARKETS

MACRO DATA POINTA:

- Germany Apr GfK index 5.9 vs consensus 5.8

- France Feb Consumer Spending +0.9% m/m vs consensus +0.4%

- UK Q4 Final GDP +1.5% y/y vs preliminary +1.5%

- UK Feb mortgage approvals 46.97k vs consensus 46.0k

- European Automobile Manufacturers' Association (ACEA) Feb Commercial Vehicles Registrations in the EU +16.8% y/y

ASIAN PACIFIC MARKTES

Most Asian market traded lower; China was the worst performing market in the region.

MACRO: Japan February retail sales +0.1% y/y vs consensus (0.5%). Jobless rate 4.6% vs consensus 4.9%. Household spending (0.2%) m/m, matching expectations.

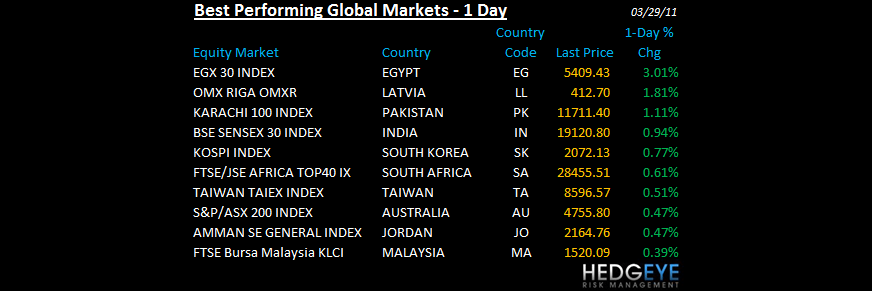

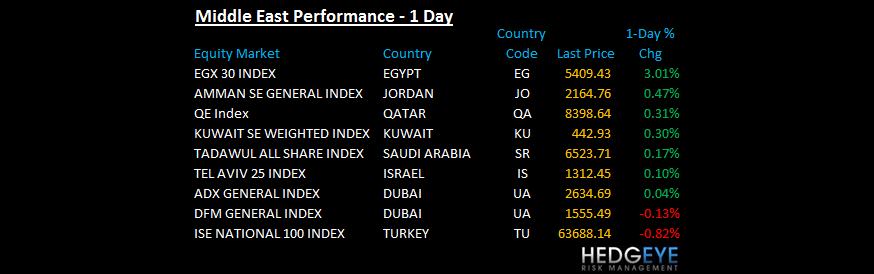

MIDDLE EAST

HEDGEYE RISK MANAGEMENT KEY LEVELS

Howard Penney

Managing Director