Positions in Europe: Long British Pound (FXB); Short EWI (Italy), Short Spain (EWP)

Thursday and Friday saw the EU Summit in Brussels largely disappoint as a consensus decision was not reached on funding for the temporary bailout facility (EFSF) – that is to provide additional funding to increase capacity from €250 Billion to €440 Billion– nor on the permanent fund (ESM) that is set to replace the EFSF in mid-2013. Instead, a decision on both facilities is set be finalized before the end of June 2011.

In other news, last week saw Portugal downgraded by credit agencies as it failed to pass an austerity bill; now the country is without a PM who vowed to quit if the program was not voted in. Early elections could be called as soon as June as investors shake concerning the question if/when the country will receive a bailout (pegged between €50-80 Billion) from the EU and IMF.

Meanwhile Ireland is set to publish the results of its additional round of stress tests this Thursday (3/31). Estimates suggest the government will need to inject an additional €27.5 Billion worth of capital. The Irish government continues its standoff versus Germany and France to maintain its 12.5% corporate tax rate and today reiterated that it wants to impose losses on banks’ senior bondholders.

Today Reuters reported that a Eurozone central banking source told the agency on Saturday that a new facility to give troubled Eurozone banks liquidity over a longer time frame, and replace the ELA (Emergency Liquidity Assistance), is currently being worked out for a more specific release this week. The source suggests that while the facility will be tailored to Ireland’s banking crisis, it would be available to the entire Eurozone. More to come….

The spotlight has missed Spain in recent weeks; despite the uncertainty surrounding the country’s banking system, a bailout does not look imminent. That said, Spain remains on the front of our screens as an economy (far greater than Greece, Ireland, and Portugal) that would require a far larger bailout and would have significantly more impact on the common currency.

The EUR-USD continues gain amid weakness in US debt/currency policy, and due to the ECB's signal it will raise its benchmark interest rate in the coming months. Our immediate term TRADE range for the EUR-USD is $1.39-1.42.

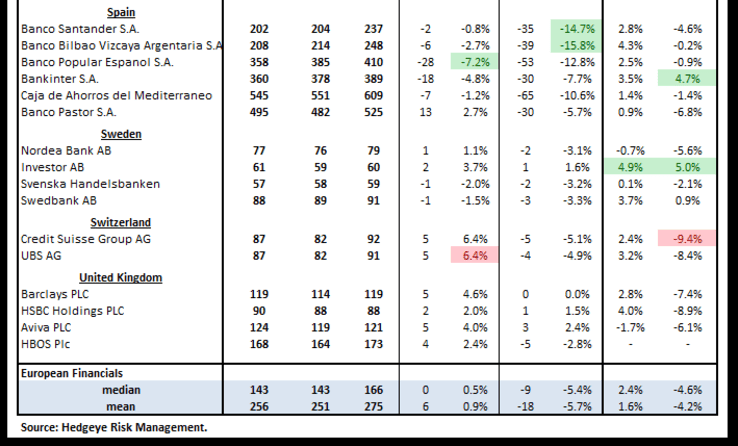

Below we include our weekly Risk Monitor for European bank CDS. Banks swaps in Europe were mixed week-over-week, tightening for 17 of the 39 reference entities and widening for 22. Greek banks showed a notable widening.

Matthew Hedrick

Analyst