“Let him that would move the world, first move himself.”

-Socrates

Working closely with a European over the past year has been a learning experience for me. Europe’s history has always been fascinating, of course, but the future of Europe is now highly topical as uncertainty mounts and political turmoil seems more and more likely to cross the Mediterranean and bring tectonic shifts in the power structure of the continent. Having a European on the team helps me to get a different perspective on events over there. It’s been educational!

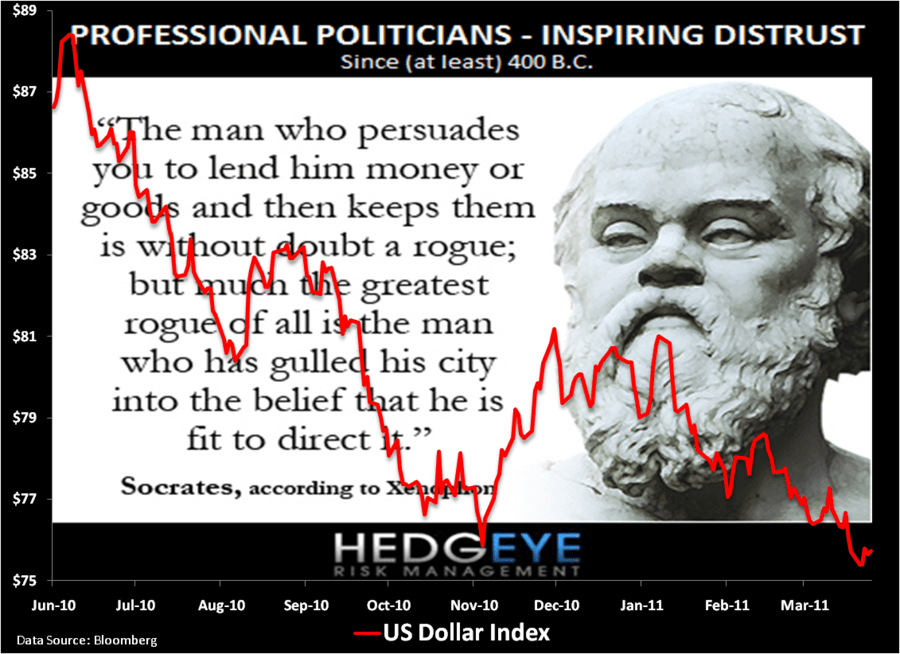

One small thing I’ve realized is that European names often sound far more grandiose than the names I grew up around. For instance, economist and former president of the Deutsche Bundesbank, Axel Weber, does not sound like a man you’d want to mess with. The time has come for Portugal’s travails to garner some media attention and, with it, another interesting name has been brought to my attention. Jose Socrates.

While I have a firm interest in politics in this Republic, and therefore have a passing interest in the origins of Western philosophy, I must confess that my weekend reading list is not heavily weighted towards political philosophy. In yesterday’s Early Look, Keith referenced the Portuguese Prime Minister Jose Socrates, and his recent decision to step down. Relative to some of his fellow eurocrats, Socrates showed a degree of humility in tendering his resignation this week in light of the escalating sovereign debt issues in Portugal.

His namesake that lived in Athens over 2,400 years ago was tried and killed for disrespecting the gods and corrupting the youth of Athens. Rather than plea for his life and compromise principles he held dear, Socrates accepted the death that preceded his death as part of the social contract between himself and society. He refused, as a matter of principle, to pursue conventional politics. In fact, in The Apology, he is depicted as an individual that took pride in distancing himself from public office, reflecting that he was “really too honest a man to be a politician and live”. As the quote at the head of this Early Look indicates, Socrates’ view was that people should adjust themselves, and their views, to fit the world and its realities. Clearly this is not a tenet that has been held by many politicians, in 400 B.C. or 2011 A.D.! It seems that Keith, in his disapproval of Professional Politicians, is in good company.

We do not see 2011 as the year opacity died in Washington D.C. It will likely survive as long as this Union does. However, we are aware of the increasing premium Americans are placing on transparency, accountability, and trust. Twitter, YouTube, and the general proliferation of easy-access information – and the thirst for it – underline this trend. As a sanity check, simply observe the steady decline of self-professed leaders stepping into the political arena. Transparency separates the boys from the men, the principled from the corrupt, and the industrious from the idle. We believe demand-driven transparency is coming to America in a big way. It is no longer a choice of politicians and public figures to be forthright or not; individuals are demanding it. That was our call when we opened the doors at Hedgeye in 2008, and it remains our call today.

Being cognizant of the fact that our role is to help our clients make money and, more importantly, not lose any, I have applied the Socratic Method in consulting some colleagues about some of their best fundamental ideas. The Socratic Method searches for general, commonly held truths that shape opinion, and scrutinizes them to determine their consistency with other beliefs.

This Method rhymes with our modus operandi at Hedgeye: upon gaining conviction in a fundamental thesis, each vertical filters the idea through our Macro process in order for the idea to ultimately become a call we communicate to clients of the firm. Below, I outline some broad parameters impacting our current investment approach from a fundamental perspective:

- Job creation is a net positive, but too slow for a real robust recovery

- Inflation is real, despite what Bernanke and everyone who is long oil/energy tells us (bullish on oil)

- Government support for consumer income will diminish beginning 2Q11 (short large, cumbersome consumer businesses)

- Focus on some basic consumer services that are less discretionary (eating out and/or dental needs)

- Think local – what can consumers do to entertain themselves while not driving too far (casual dining/regional gaming)

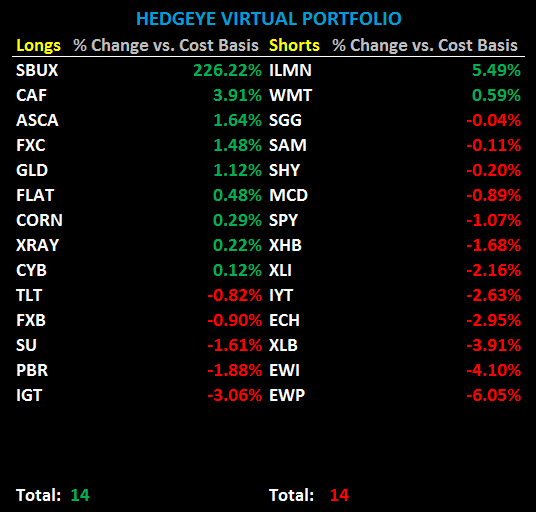

Here are some ideas from the research team using me as a filter, with one caveat -- Keith has not signed off on them with his quantitative models as a long or short. The ideas would all fit in the intermediate term TREND duration:

Financials: Today at 11am we are rolling out a Hedgeye Black Book highlighting TCF Financial (TCB) as a SHORT. Our horizon for TCB is over the next 2-3 quarters. Our Financials team’s core thesis is that the street is underestimating credit losses in the consumer loan book at TCB. We think there’s downside of 20% over 6-9 months.

Energy: Long SUNCOR Energy (SU). As global geo-political tensions mount, particularly in the Middle East where nearly 60% of the world’s proven reserves lie buried, oil deposits in low political risk countries as Canada are increasingly more valuable. Our favorite among these attractive Canadian Oil Sands companies is Suncor (SU) which has no exploratory risk; price and operating leverage are strong tailwinds. We consider it cheap with more upside potential than downside risk; SU is underpriced in the market by ~20%. With Brent crude oil at ~$115/bbl and SU 87% oil weighted, price momentum is a strong tailwind, as SU has a 0.69 positive correlation with Brent.

Gaming: This was a difficult choice given the group’s recent performance. The Gaming team has been very positive on IGT but could not go with name today given the +5.04% move yesterday. I like the Ameristar Casino (ASCA) story. ASCA is a best in class operator that should be able to beat the quarter. The MACRO environment is stable relative to other gaming operators, the company has easy comparisons, and the FCF yield offers some downside protection.

Restaurants: I continue to be positive on SBUX, but I’m going with Brinker International (EAT). I recently met with management in a market where the company has recently reimaged 16 stores and they appear to be hitting the company’s hurdle rates for return on investment. The best way to describe how the company is thinking about the remodels is that they don’t want to simply “preserve the status quo.” Like our Gaming, Lodging and Leisure team’s view of ASCA, I think the earnings estimates are low for the current quarter. I still like the SHORT side of MCD, and we are currently short that stock in the Hedgeye Virtual Portfolio.

Retail: One name that has been in and out of the Hedgeye Virtual Portfolio and a high-conviction SHORT is Carters (CRI). What we see, that the street does not, is that margins will unravel by 400bps in 2011. The retail team posted a note on 9/16/10 with the title “CRI: One of the Worst Stories in Retail.” Now that is conviction. Other SHORT names to consider are J.C. Penney (JCP) and Wal-Mart (WMT).

Healthcare - I’m going with DENTSPLY International (XRAY). The Hedgeye Healthcare team has been conducting a series of calls with dentists focusing on our MACRO survey work. The bottom line is that our demand model is forecasting rising visit volume, driven by per capita visits by age and employment status. In FY 2011, our model suggested some improvement in US patient visits and we assumed some improvement in mix from patients signing on to “treatment plans” that dentists are selling (this is consistent with what dentists are suggesting in our calls). EPS growth should accelerate in FY2011 as the US market improves, particularly in the second half as employment gains among younger workers accelerates. Another long in the Healthcare space is Baxter (BAX). BAX is insulated from much of the global macro turmoil as their IVIG business returns to price and volume growth, but it is less interesting at these levels based on our fundamental factor screens. I would defer to Keith as to what he thinks might be a good entry point. The fundamentals suggest the stock is in need of a catalyst or a pullback. Lastly, their Japan exposure is not insignificant.

I apologize for the longevity of this Early Look. I’ll leave you with some parting words from the Athenian Socrates ahead of the weekend: “Enjoy yourself -- it’s later than you think”.

Function in disaster; finish in style,

Howard Penney

Rory Green