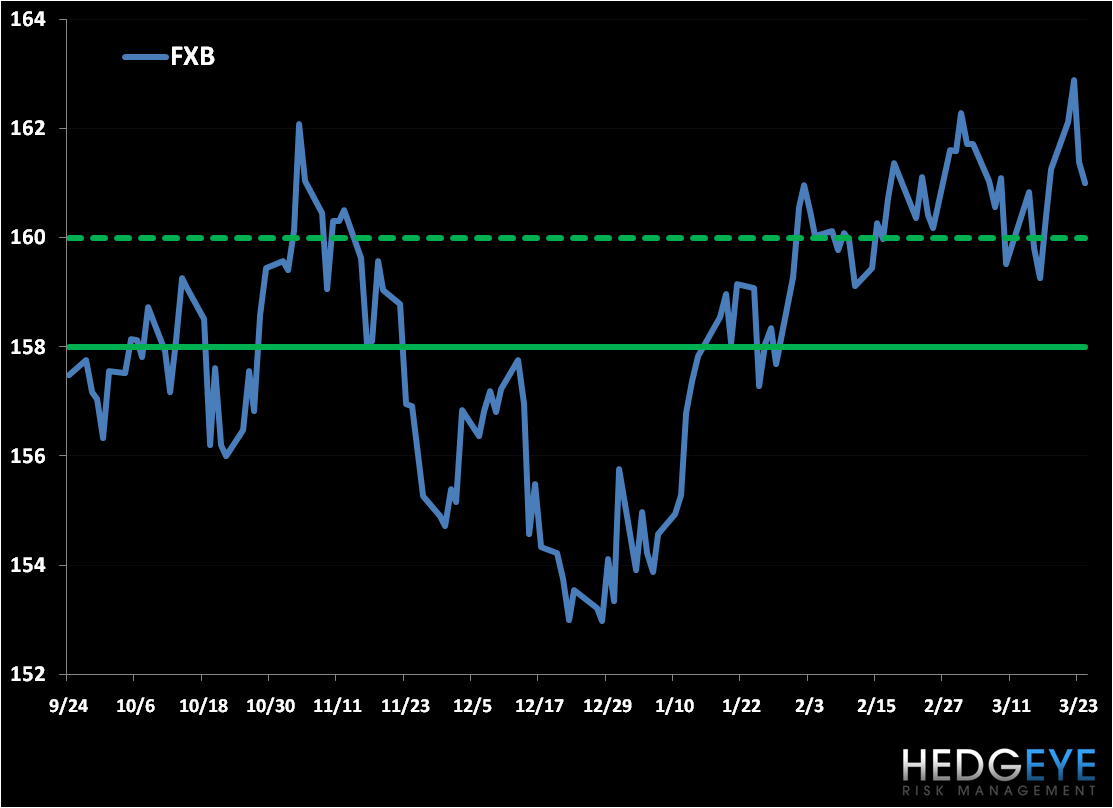

Positions in Europe: Long the British Pound (FXB); Short Italy (EWI), Short Spain (EWP)

High Frequency PMI Data Inflects

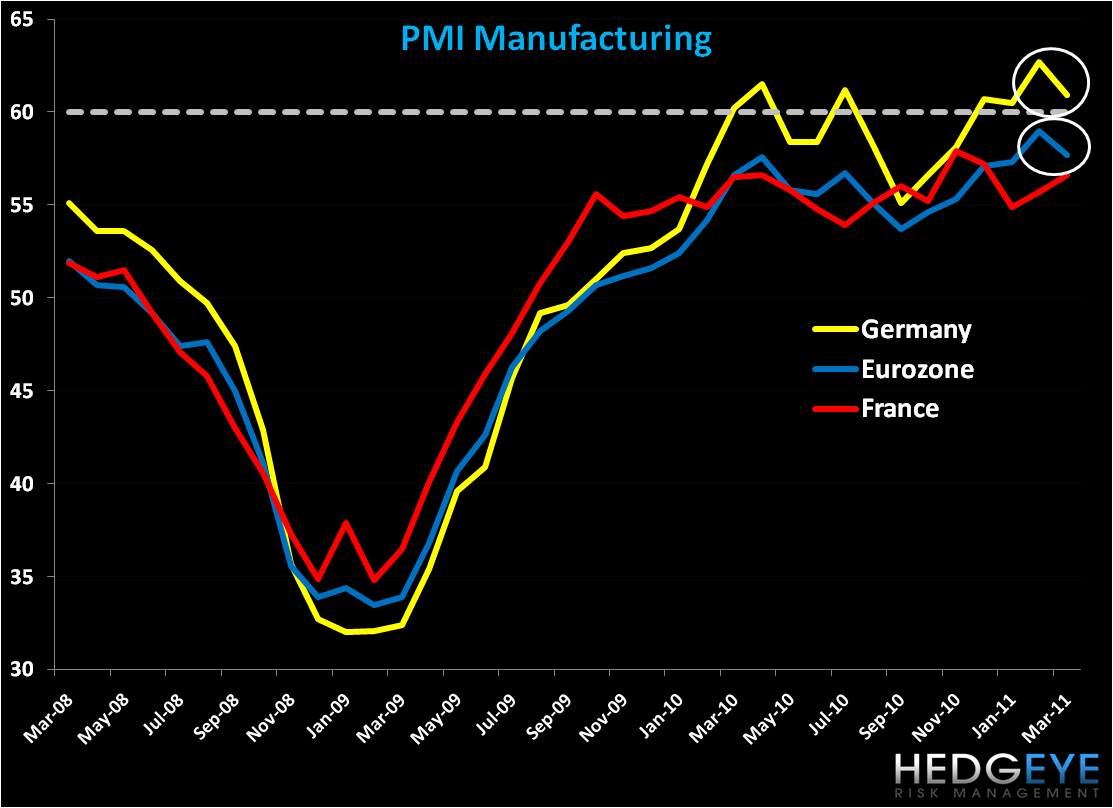

An initial March reading today of Manufacturing and Services PMI data for Germany, France, and the Eurozone average showed a market inflection to the downside in manufacturing in Germany and the Eurozone versus the previous month. The move is indicative of the uncertainty in global demand following the earthquake and tsunami in Japan earlier in the month, but also the mean reversion trade. As we’ve mentioned over the last three months, European PMI figures were white hot, in particular for German manufacturing, which was bumping up against and through the 60 line, a heavy resistance level on a historical basis (see charts below).

While we continue to like Germany longer term from a fundamental basis, our models show that the fiscally sober nations of Europe (think Germany, Sweden, and the Netherlands) are all broken on immediate term TRADE and intermediate term TREND durations. Therefore, we’re not invested in them in the Hedgeye Virtual Portfolio. Perversely, some of Europe’s most indebted nations are leading global equity performance YTD (think Greece +13.9%, Italy +8.5%, Spain +8.4%), while Germany underperformed strongly in the days following Japan’s earthquake on March 11th and is flat year-to-date.

However, German fundamentals and business trends continue to look positive. Exports are expanding, employment has improved, and factory orders and business confidence have come in strong over recent months. GDP is expected to grow 2.5% this year. We continue to believe that Germany will be the region’s growth engine and given the country’s fiscal conservatism Germany can also be a defensive play as the region remains mired in a sovereign debt contagion.

Here are a few recent news stories to keep in mind regarding Germany:

- Last week Chancellor Merkel ruled to shut down 7 of the country’s oldest nuclear plants for a 3 month moratorium.

- On Wednesday, Germany refused to participate in the enforcement of an arms embargo on Libya that the UN authorized and has abstained in the Security Council on the resolution authorizing military action to protect Libyan civilians. Germany is therefore diverging from its European allies Britain and France, who have supported the UN action.

- Support for Merkel’s CDU party has waned in state elections this year (already in Hamburg and Sachsen-Anhalt). This Sunday, the CDU could well lose its stronghold in elections in Baden-Wuerttemberg and Rheinland-Pfalz. As support for the CDU at the state level wanes, expect Merkel to face increased opposition in the upper and lower houses of parliament which will weaken her broader authority.

Socrates Takes a Bow

Late yesterday Portugal’s parliament voted down the newest austerity bill backed by PM Jose Socrates and his minority Socialist party. While the outcome wasn’t a great surprise, Socrates had made it clear going into the vote that if the package didn’t pass he’d step down. Now with his resignation tendered, there’s increased noise that Portugal will asks for a bailout from the EU and IMF worth €50-100 Billion in the coming days. [The risk premium to own Portuguese debt has jumped, reflected by Portuguese CDS trading up 37bps since Monday (3/21) to 533 bps.]

Under these circumstances, and the decision by Fitch today to cutting Portugal’s debt rating, today begins the first of a two-day EU Summit to decide on the structure of the region's temporary and permanent bailout funds. The most recent kink in the armor comes with Finland’s firm stance that it won’t approve increasing its loan guarantees to the temporary bailout fund (the European Financial Stability Facility, or EFSF) in order to raise its full capacity to €440 Billion versus the current ~ €250 Billion. It also appears Ireland will not get a concession on the interest rate of its bailout loan (~5.8%) as the country is unwilling to hike its corporate tax rate (at 12.5% vs EU average of 23%). All in, it appears friction may well divide the Summit and prevent a unified decision. We believe this would weaken the common currency.

This EUR-USD has held up well this month despite sovereign debt contagion fears coming back into the market spotlight over recent weeks. We primarily attribute this to the USD’s weakness. However, we believe the market has largely priced in that the Summit would go off without a hitch, meaning that both the increase in funding for the temporary bailout fund (EFSF) would pass as would a permanent fund, or the European Stability Mechanism worth €500 Billion beginning in mid-2013. Should this not be the case, we’d expect the EUR-USD to pull back from its recent steady level of $1.41.

---

We bought the British Pound via the etf FXB in the Hedgeye Virtual Portfolio yesterday (see levels below). We’ll have a post out on our outlook on the UK economy, including the implications of Chancellor of the Exchequer Osborne’s 2011 Budget, in the coming days. We remain short Italy (EWI) and Spain (EWP) over the intermediate term TREND.

Matthew Hedrick

Analyst