Positions in Europe: Sold Long Germany (EWG) today; Covered Short Spain (EWP) on 3/16

In the last two days both the Swiss National Bank (SNB) and Norway’s Central Bank (Norges Bank) kept their main interest rates on hold, at 0.25% and 2.00% respectively. The decisions are worth considering within their own context, and as it relates to ECB policy.

Today’s decision from the SNB to HOLD comes as no great surprise as a hike would likely encourage the appreciation of the Swiss Franc (CHF) vs most major currencies, in opposition to the SNB’s mandate to limit appreciation to protect the country’s exports; further, inflationary pressures remain benign with Swiss CPI at +0.1% in February Y/Y.

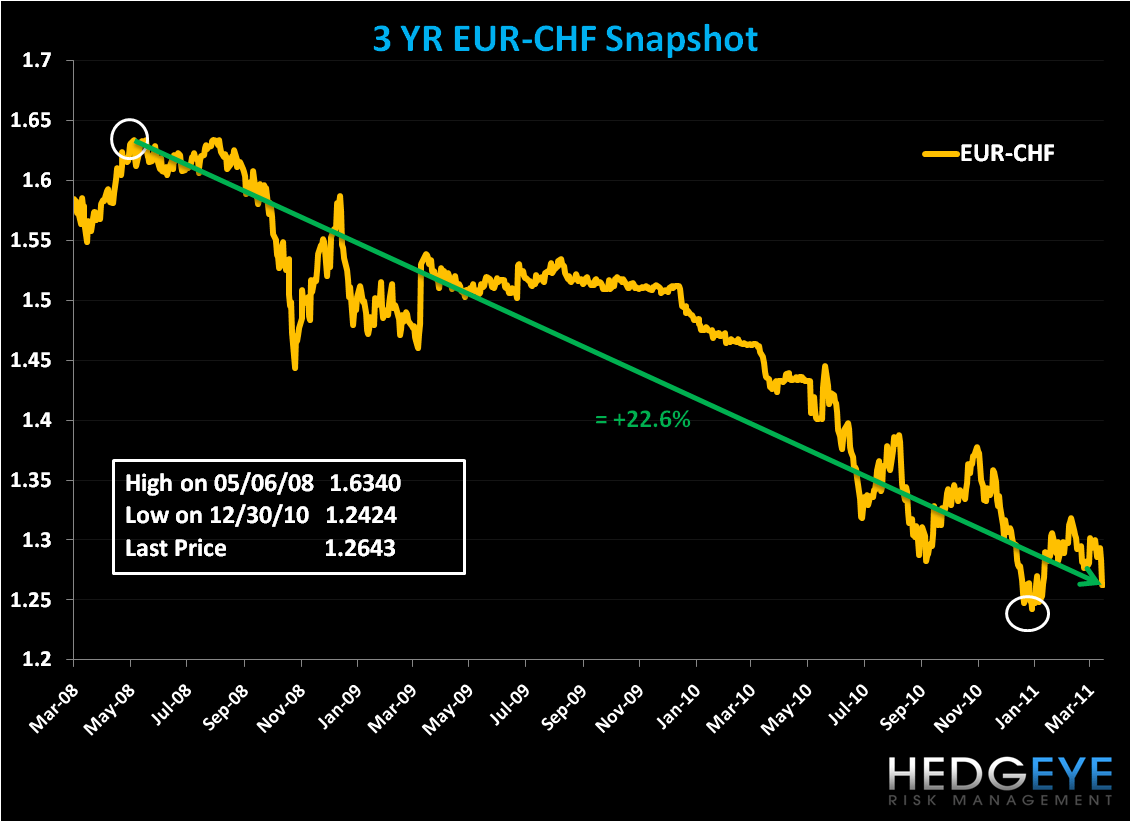

As a safe haven play, the CHF vs most major currencies has gained steadily over the long term; intermediate term (vis-à-vis the Eurozone’s sovereign debt contagion); and immediate term in the wake of the earthquake in Japan (+2.2% since March 14th). The chart below shows just how prevalent the currency’s appreciation has been since a low in early May 2008:

Norges Bank also left rates unchanged yesterday, despite threats of rising home price inflation (+9.2% in February Y/Y) and household credit growth on the rise. CB Governor Jan F. Qvigstad said there is a “50/50 chance in May or June” of a rate increase.

Both bank decisions to keep rates on HOLD give credence to the recent pause in global economic sentiment following the earthquake in Japan. In our mind, the events in Japan may well tame the hawkish commentary of ECB President Trichet at the last ECB meeting on 3/3 in which he signaled that a hike (likely 25bps) could come as soon as next month. While the Eurozone is feeling pressure from rising inflation -- CPI in February came in 10bps higher than January at 2.4% Y/Y -- given the threat of stagnation from the world’s third largest economy (Japan’s GDP equals ~ 9% of the global economy), persistent European sovereign debt contagion concerns, and further unrest in the Middle East and North Africa, Trichet and the rest of the ECB governing board may reconsider the impact a rate hike will have on the region, especially for the periphery which shows a strong negative divergence across fundamentals, including high debt and deficit levels, poor GDP growth prospects for this year and next, and high inflation and unemployment levels.

Under these global conditions, Trichet may well elect to push out a rate hike decision.

Matthew Hedrick

Analyst