This note was originally published March 17, 2011 at 07:55am

“It isn’t as important to buy as cheap as possible as it is to buy at the right time.”

-Jesse Livermore

Having been a market practitioner for the last 12 years, I’ve come to respect that a Risk Manager needs to be as well versed in the tactical thinking of a Jesse Livermore (“Reminiscences of a Stock Market Operator”) as the libertarian theorizing of a Bastiat (read “The Law”, 1850).

Valuation isn’t a catalyst. Price momentum is. When the slope of price momentum changes to the bearish side, valuation becomes a trap. When price momentum is bullish, it justifies the best storytelling in the world.

I’m not so much interested in being a valuation-guy, a perma-bull, or a perma-bear. Been there, tried all three. I’m interested in being right. Livermore taught me the same – “There is only one side of the market and it is not the bull side or the bear side, but the right side.”

Whether you are on the buy-side or the sell-side, I’ll assume your goal is also to be on the Right Side. That’s how you get paid. Sure, we all have different durations and risk tolerances in being exposed to our respective investment decisions. But the market doesn’t care about how we think about these things individually. The market waits for no one.

This is why I am trying my best to evolve my Multi-Factor Global Risk Management Model so that it is Duration Agnostic. That’s where the concept of our TRADE/TREND/TAIL framework was born. And the mathematical principles of interconnectedness embedded in Chaos Theory support it.

As a reminder, here’s how we think about TRADE/TREND/TAIL durations:

- TRADE = the immediate-term (as in 3-weeks or less, which I’ll get to in a minute in terms of seeing a Short Covering Opportunity)

- TREND = the intermediate-term (3-months or more, which is how we think about companies and countries sequentially)

- TAIL = the long-term (3-years or less, which is how we think about our key Global Macro Themes like “Housing Headwinds”)

Of course, some of you invest beyond what I am defining as the TAIL. I do too. When I invested 1/3 of my net wealth to create Hedgeye Risk Management, I considered that a fairly long-term and concentrated investment idea.

But when it comes to managing Global Macro market risk in an environment of Heightening Price Volatility (which is what these Fiat Fool central planners from the US Federal Reserve to the Bank of Japan are perpetuating via their unprecedented money printing experiments), I think you need to acutely manage the shorter-term duration risk - the TRADE and TREND.

So that’s how we think about it and this is what I did about it yesterday in the Hedgeye Portfolio:

- Covered short position in SPAIN (EWP)

- Covered short position in EMERGING MARKETS (EEM)

- Covered short position in WALMART (WMT)

- Covered short position in INDUSTRIALS (XLI)

- Bought long positions in HEALTHCARE (XLV)

- Added to long position in GERMANY (EWG)

Overweighting one of the key risk management relationships we’ve been working with in calling for this 6.5% correction (the inverse relationship between the SP500 and the VIX), yesterday I finally registered a signal that I considered an explicit Short Covering Opportunity.

- The SP500 is immediate-term TRADE oversold (3.0 standard deviation move)

- The VIX is immediate-term TRADE overbought (3.5 standard deviation move)

Now there is a difference between what The Street and a bullishly-bias media amusingly label a “buying opportunity” and what Risk Managers recognize as a Short Covering Opportunity.

A Short Covering Opportunity is reserved for those Risk Managers who had the sobriety to short things before they started going down. A “buying opportunity” is a decision to deploy cash and expand you gross exposure to the market.

I did both yesterday (you are allowed to do both):

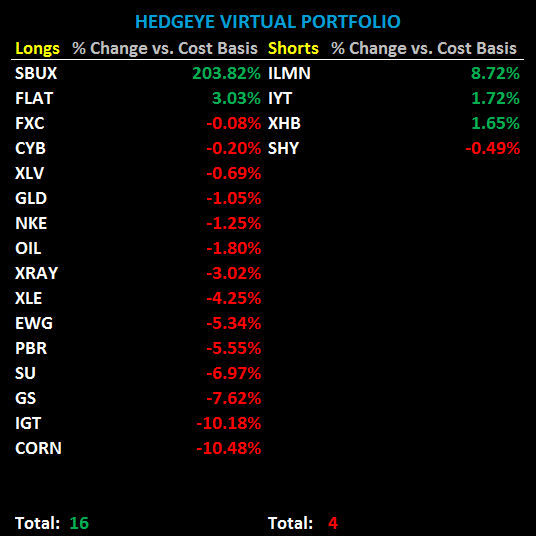

- Hedgeye Portfolio (a proxy for my net exposure to the market): I moved to 16 LONGS and 4 SHORTS, by covering shorts

- Hedgeye Asset Allocation (a proxy for my gross exposure): I moved to 43% CASH yesterday, down from 46% the day prior

Again, I fully respect and understand that how I am expressing my risk management views may not be found in a Yale economics textbook on portfolio theory. I am trying to evolve the risk management process and show the financial services community that there is a transparent and accountable way that a firm can both originate ideas and manage risk, without being on the other side of our clients’ trades.

I also fully understand (but do not fully respect) the marketing message behind being “fully invested.” Sure, there will be a time for that (Q2 of 2009), but not when our fundamental Global Macro research is proactively calling for Global Growth Slowing As Global Inflation Accelerates. When the winds of price momentum blow from bullish to bearish, that’s called being fully exposed.

I’m not trying to take a “victory lap” this morning. I am deeply interested in trying to explain what we are doing here and why. I don’t think it’s credible for the said savants of Wall Street “strategy” to keep missing huge draw-downs in global markets like they have for the last decade. Instead of whining about it, we are passionately pursuing a better way.

My immediate term support and resistance lines for WTI crude oil are now $97.02 and $102.60, respectively, and I took our asset allocation to oil up to 6% on Monday from 3%. My immediate term support and resistance lines for the SP500 are 1256 and 1274, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer