TODAY’S S&P 500 SET-UP - March 17, 2011

We made a "short term bottom" call into the close yesterday, and this morning’s action in global equity, commodity, and currency markets confirms the same. Every market gets immediate-term TRADE overbought and oversold. As we look at today’s set up for the S&P 500, the range is 18 points or -0.07% downside to 1256 and 1.36% upside to 1274 (with upside to 1307 on a close > 1274).

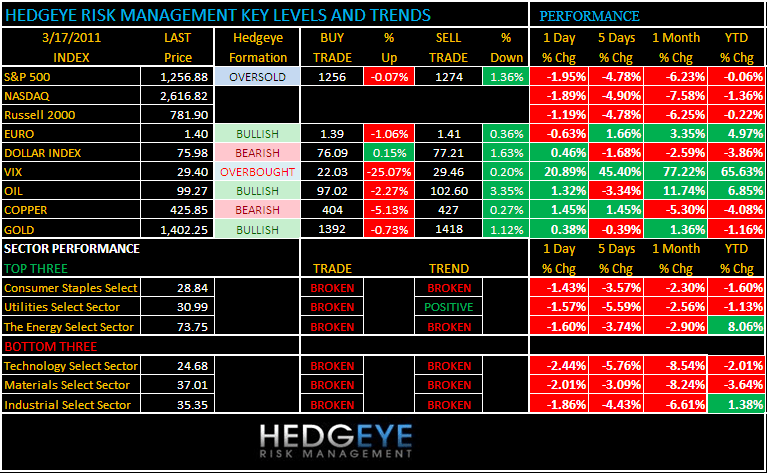

PERFORMANCE:

As of the close yesterday we have 0 of 9 sectors positive on TRADE and 2 of 9 sectors positive on TREND - Energy and Health-care.

- One day: Dow (2.04%), S&P (1.95%), Nasdaq (1.89%), Russell 2000 (1.19%)

- Month-to-date: Dow (5.01%), S&P (5.30%), Nasdaq (5.95%), Russell (5.05%)

- Quarter/Year-to-date: Dow +0.31%, S&P (0.06%), Nasdaq (1.36%), Russell (0.22%)

- Sector Performance: - Tech (2.44%), Industrials (1.86%), Materials (2.01%), Financials (1.85%), Energy (1.60%), Healthcare (1.74%), Consumer Disc (1.70%), Utilities (1.57%), Consumer Spls (1.43%)

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1636 (+106)

- VOLUME: NYSE 1460.96 (+13.43%)

- VIX: 29.40 +20.89% YTD PERFORMANCE: +65.63%

- SPX PUT/CALL RATIO: 2.52 from 1.69 (+48.45%)

CREDIT/ECONOMIC MARKET LOOK:

Treasuries were underpinned by a pickup in flight-to-quality buying.

- TED SPREAD: 22.58 0.101 (0.451%)

- 3-MONTH T-BILL YIELD: 0.10% +0.01%

- 10-Year: 3.22 from 3.33

- YIELD CURVE: 2.64 from 2.70

MACRO DATA POINTS:

- 8:30 a.m.: Consumer Price Index, est. 0.4%, prior 0.4%

- 8:30 a.m.: Net export sales, commodities

- 8:30 a.m.: Jobless claims, est. 388k, prior 397k

- 9:15 a.m.: Industrial production, est. 0.6%, prior (-0.1%)

- 9:15 a.m.: Capacity production

- 9:45 a.m.: Bloomberg Consumer Comfort, prior 44.5

- 10 a.m.: Leading indicators, est. 0.9%, prior 0.1%

- 10 a.m.: Philly Fed, est. 28.8, prior 35.9

- 10:30 a.m.: EIA Natural Gas

- 3 p.m.: Geithner attends FSOC meeting

WHAT TO WATCH:

- U.S. nationals urged to leave Japan amid growing fears of nuclear meltdown

- Obama administration indicates it will vote at the United Nations tomorrow to authorize military actions and no-fly zone in Libya

- U.S. House Republicans vote to cancel $1b in housing aid

- Moody’s keeps negative outlook on U.S. states and local government bonds

- Senate is expected to vote on three-week budget resolution

COMMODITY/GROWTH EXPECTATION:

- CRB: 338.17 flat YTD: +1.61%

- Oil: 97.98 +0.82%; YTD: +6.85% (trading +1.43% in the AM)

- COPPER: 419.75 +1.46%; YTD: -4.08% (trading +1.57% in the AM)

- GOLD: 1,396.95 +0.16%; YTD: -1.16% (trading +0.37% in the AM)

COMMODITY HEADLINES FROM BLOOMBERG:

- Soaked Midwest Soil Boosts Flood Risk for U.S. Wheat Crops, Sandbag Cities

- Beef, Pork Production in Japan’s Eastern Region Disrupted, Ministry Says

- Thailand, Indonesia, Malaysia May Delay Rubber Shipments, Consortium Says

- Oil Leads Commodity Advance for Second Day, Reversing Earlier Decline

- Gold May Advance as Japanese Crisis, Turbulence in Middle East Spur Demand

- Dry Weather May Hurt Coffee Production in Vietnam, Bolstering World Prices

- Copper May Rise in London on Prospects for Japan Rebuilding: LME Preview

- Glencore Loses $3.6 Billion as Mining Stocks Decline, Threatening IPO Plan

- Japan Quake May Mean U.S. Heating Oil Price Tops Gasoline: Energy Markets

- U.S. Feedlots Buy Fewer Cattle as Feed Costs Increase, According to Survey

- Corn, Wheat Advance as 9.5% Price Decline Attracts Importers, Investors

- Palm Oil Futures Decline for Second Day on Expectation Supplies to Expand

CURRENCIES:

- EURO: 1.3889 -0.63% (trading +1.04%% in the AM)

- DOLLAR: 76.681 +0.46% (trading -1.02%% in the AM)

EUROPEAN MARKETS:

No major MACRO data points were released today. Generally, European markets are trading higher. Austria and Ireland are the two best performing markets up over 1%. Iceland is the worst performing market down -1.30%.

- United Kingdom: +0.54%

- Germany: +0.61%

- France: +0.74%

- Spain: +0.66%

- Italy: +0.55%

- Greece: +0.01%

ASIAN MARKTES:

Most Asian market traded lower, with the exception of South Korea up +0.05%. The worst performing market was the Philippines trading -1.57%.

- Japan: -1.44%

- Hang Seng: -1.83%

- China: -1.14%

- India: -1.14%

- Taiwan: -0.50%

Howard Penney

Managing Director