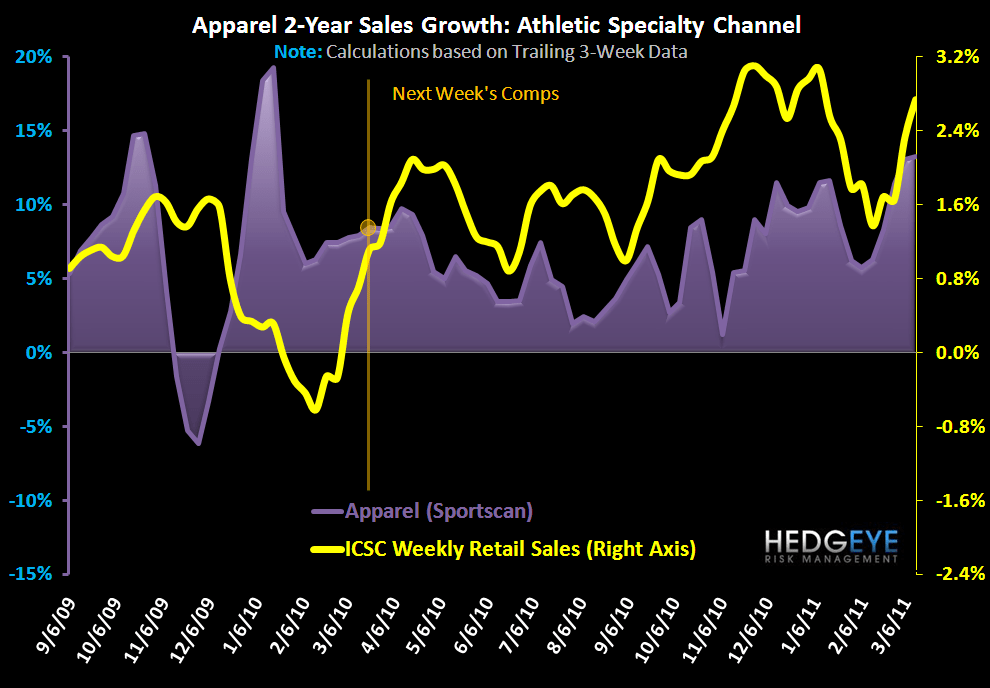

Weekly athletic apparel sales remain healthy through the first two weeks of March extending a strong finish to February. Both the athletic specialty and department/mass channels improved on the week while sales in the family channel slowed on the margin. Most notably, ASPs declined in both the athletic specialty and family channel for the fourth straight week. However, unit volume continues to outpace ASP declines. On the contrary, ASP increases have impacted sales momentum in the discount/mass channel as unit sales remained negative for the third consecutive week. Sales growth was strong across all regions with very few exceptions. The Pacific region stands out as being a laggard with momentum still positive but slowing over the prior two weeks.

Lastly, we note that athletic apparel faces its toughest compares in the coming week as it faces the Easter shift. Once past last year’s Easter comp (April 4th) compares get progressively more favorable over the next 3-months.

Casey Flavin

Director