Darden is scheduled to report fiscal 3Q11 earnings next week on Thursday, March 24 after the market close. The company held a two-day analyst meeting on January 31 and February 1 and provided a mid-quarter update on earnings and comp guidance. Although the company cited an estimated negative 80 bp impact from weather and a 20 bp hit from the Lenten season shift into fiscal 4Q11 this year on fiscal 3Q11 blended comps (60 bp Lent shift impact at Red Lobster), the company’s second half blended comp guidance of +1.5% to +2.5% assumes a significant acceleration in two-year average trends across each of its three major concepts. Specifically, management guided to +3.0% to 3.5% same-store sales growth at the Olive Garden in fiscal 2H11, flat to -0.5% comp growth at Red Lobster and +4.0 to +4.5% growth at LongHorn Steakhouse.

For fiscal 3Q11, management stated that it expects comps to come in at +1.0%, or just below the mid-point of the targeted 2H11 comp range after adjusting for the negative weather impact. This +1.0% comp growth would translate into a 280 bp acceleration in two-year average trends from the prior quarter, which seems aggressive, particularly given the recent trends at Red Lobster. It is important to remember, however, that management gave this guidance two months into the quarter and recently reported Knapp track trends point to sequentially better casual dining trends in February. That being said, I am modeling a slightly lower 0.7% blended comp estimate for the third quarter as I am not yet convinced of the timing of the turnaround at Red Lobster. This 0.7% estimate still assumes a 260 bp acceleration in two-year average trends, and that includes the negative impact from weather.

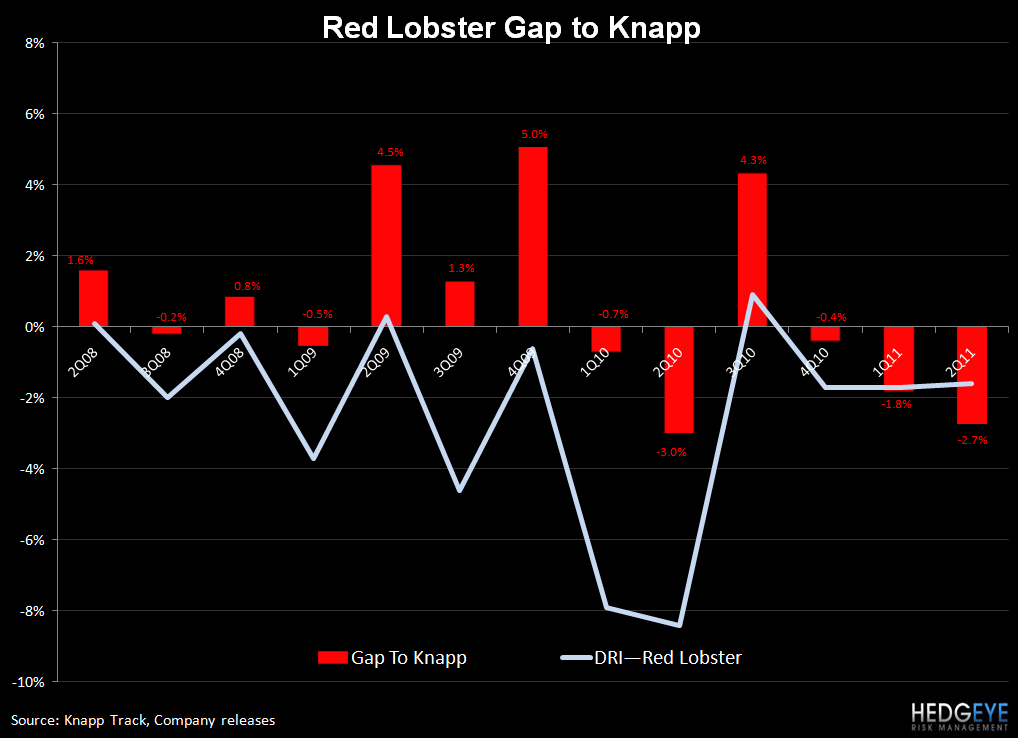

Red Lobster’s same-store sales growth has fallen short of street estimates for the last three quarters and its underperformance relative to Knapp Track trends widened to nearly 3% during fiscal 2Q11 on both a 1-year and 2-year average basis. Management attributed the weakness to the fact that affordability has become a more important consideration for its core customers and that Red Lobster’s promotions were not properly addressing that need for value. In October of fiscal 2Q11, the company altered the way it was advertising its featured menu items to include specific price points rather than just starting price points in order to provide what it called “price assurance” for its customers. Management also introduced more affordable items across the menu.

The company highlighted the sharp jump in Red Lobster’s comp growth in October and November to +1.8% from -6.6% in September as proof that these pricing changes are causing the tide to turn at Red Lobster. On a two-year average basis, comps improved an impressive 470 bps in October but then decelerated 125 bps in November, which is still much better than the extremely weak results seen in September. Management stated during its analyst meeting that trends in December and January, after adjusting for weather, were in line with October and November levels, which implies about 1.0% same-store sales growth on a reported basis when you adjust for the estimated negative 80 bps from severe weather.

Given the concept’s recent underperformance, I think investors will be most focused on whether Red Lobster was able to sustain these improved trends in February. For reference, it will be important to focus on two-year average trends in February because Red Lobster is facing a much more difficult comparison from February 2010 of +7.5% relative to the -8.5% comp in January 2010. In addition, the company’s estimated 60 bp negative impact from the shift of the beginning of Lent into 4Q11 this year will hurt reported February results. Taking this all into consideration, I am modeling a -2% comp for Red Lobster in fiscal 3Q11 (slightly below management’s -1% guidance), which assumes a nearly 450 bp acceleration in two-year average trends. This estimate is aggressive, but we know the December/January trends were positive and industry trends improved in February. The company will need to sustain the assumed significantly higher fiscal 3Q11 level of two-year average trends, relative to 1H11 levels, during the fourth quarter in order to hit its targeted fiscal 2H11 Red Lobster comp growth of flat to -0.5%, which could prove difficult.

As I stated earlier, DRI’s fiscal 2H11 comp guidance for both the Olive Garden and LongHorn implies a sequential uptick in two-year average trends, but given these concepts’ recent performance and the industry’s recently reported improved trends in January and February, the guidance does not seem to be as much of a stretch. On a one-year basis, however, the comps will likely be much better during the fourth quarter than the third quarter as a result of easier comparisons and the expected reported weather impact in fiscal 3Q11. Management’s fiscal 3Q11 blended comp guidance of +1.0% implies a 2% to 4% comp during the fourth quarter to achieve the targeted fiscal 2H11 +1.5% to +2.5% growth range.

Relative to earnings, rising commodity costs are definitely a concern for Darden. During the company’s fiscal second quarter earnings call, management guided to a +1.0% to 1.5% increase in fiscal 2H11 commodity costs and to flat FY11 food and beverage costs as a percentage of sales. A little over a month later, the company raised this inflation guidance to up 1.5% to 2.0% but did not comment on food and beverage costs as a percentage of sales. Given that commodity costs moved higher and the company updated its blended comp guidance to +1.5% to +2.0% from 2.0%, food and beverage costs as a percentage of sales will likely move slightly higher on a full-year basis, which will have a negative impact on margins in 2H11 relative to the first half when food and beverage costs as a percentage of sales declined.

I am expecting restaurant-level margins to continue to improve during the second half of the year, however, as the YOY bp change comparisons get easier and same-store sales trends should come in better, particularly during the fourth quarter. Additionally, Darden achieved significant leverage on the labor line during the first half of the year, which I expect will continue and help to offset some of the commodity cost pressures. Further helping the labor expense line is the company’s new direct labor optimization initiative, which it is rolling out later in the year. Management anticipates this effort will generate modest savings during fiscal 4Q11 and then ramp up significantly next year, ultimately delivering $30 million to $40 million in annual savings when fully implemented.

I am currently modeling full-year earnings of $3.37 per share, which is in line with both the street’s estimate and the high end of management’s full-year guidance. Relative to consensus EPS estimates, however, I am $0.02 shy of the third-quarter estimate and $0.02 higher for the fourth quarter.

Howard Penney

Managing Director