Conclusion: Portugal is shaking with a heavy load of its debt (principal + interest) for 2011 coming due over the next 3-4 months; this is combined with a credit rating downgrade this morning, and push backs on its austerity programs to narrow its high debt and deficit imbalances. Bailout cometh?

Positions in Europe: Long Germany (EWG); Short Spain (EWP)

As the spotlight returns to Europe’s sovereign debt and deficit issues, Portugal continues to melt. All the macro signals we follow suggest that Portugal will likely follow its peers Greece and Ireland and require a bailout to meet its fiscal imbalances. The supporting evidence includes:

- A hefty schedule of debt (principal + interest) that comes due in the months of March, April, and June (or ~ €16.1 Billion), accounting for nearly two thirds of its debt obligations for 2011 (or ~ €25.4 Billion). So far the country has sold ~ €7 Billion in bonds of its €20 Billion target this year. (See chart below)

- Portugal’s credit rating was cut 2 steps by Moody’s today to A3 (or 4 steps from junk), citing the country’s “subdued growth prospects” and “the implementation of risks for the government’s ambitious fiscal consolidation targets.”

- Portugal’s Finance Minister Fernando Teixeira dos Santos acknowledged today that the country's current borrowing costs aren't sustainable in the medium and long term, according to the WSJ.

The combination of a substantial near-term load of debt payments due with a downgrade of its credit rating suggests that the yield premium to issue Portuguese debt will continue to push higher, making it harder to finance its near-term issuance, all of which increases the probability that the country asks for outside support. In an auction of 12-month treasury bills today worth €1 Billion, the average yield paid was 4.331%, up from 4.057% two weeks ago.

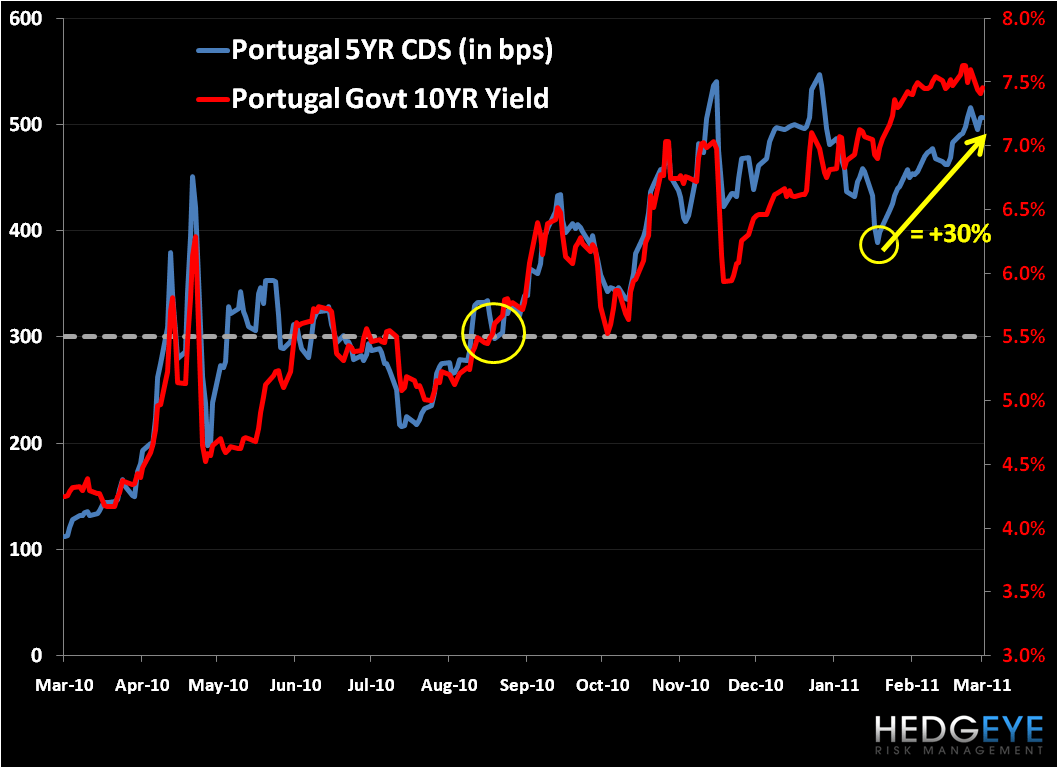

And the risk management signals that Portugal is near asking for a bailout include:

- Sovereign CDS suggests the risk trade is definitely “on”, and has been for over a year. Since a year-to-date low in Portuguese CDS on February 3rd at 389bps, CDS is up 30% to 507bps. Like we saw in the case of Greece and Ireland, when the 300bps level was violated to the upside, a bailout of the country came within weeks. Portugal broke out convincingly from the 300bps level in early September of last year. (See chart below)

- Like CDS, the risk premium to own Portuguese debt is also reflected by the government’s 10YR bond, which shows yields increasing 100bps year-to-date.

Finally, PM Socrates announced late yesterday that opposition lawmakers’ resistance to additional budget cuts announced last week to meet deficit targets threatens a “political crisis”. Socrates and his Socialist party, which does not have a majority in parliament, has put forward an overly ambitious target (in our opinion) to cut the country’s budget deficit from 9.3% of GDP in 2009 to an estimated 7% in 2010, 4.6% in 2011, and to the EU limit of 3% in 2012. The government issued austerity measures in late September 2010 that included a 5% wage reduction for public sector workers earning more than 1,500/month, a hiring freeze, and an increase in VAT from 21% to 23%. Now the government is calling for new austerity plans to control operational and administrative expenses.

Today Socrates said that the plan for the new cost cutting measures would be announced before the EU Summit on March 24-5 and acknowledged that if the new austerity measures are voted down in parliament, his government would likely face early elections.

Given the political consternation about the size and shape of its austerity program combined with the near-term forces of rising debt costs into a schedule of sizable payments coming due and estimated -1.3% GDP in 2011 (expect tax revenues to be down!), we think the probability of a near-term bailout in Portugal has greatly increased. We can’t be certain of the position Eurozone leaders will take on Portugal in the days ahead, especially ahead of the EU Summit on March 24-5, but we’d expect the market to continue to punish Portugal as uncertain surrounds the collision of its fiscal and political imbalances and near-term debt obligations.

Matthew Hedrick

Analyst