There are a few datapoints out of the footwear space worth noting over the past 24 hrs. They generally point to continued health in the space, and give us added confidence in our call on Athletic Footwear overall, as well as on Collective Brands (PSS).

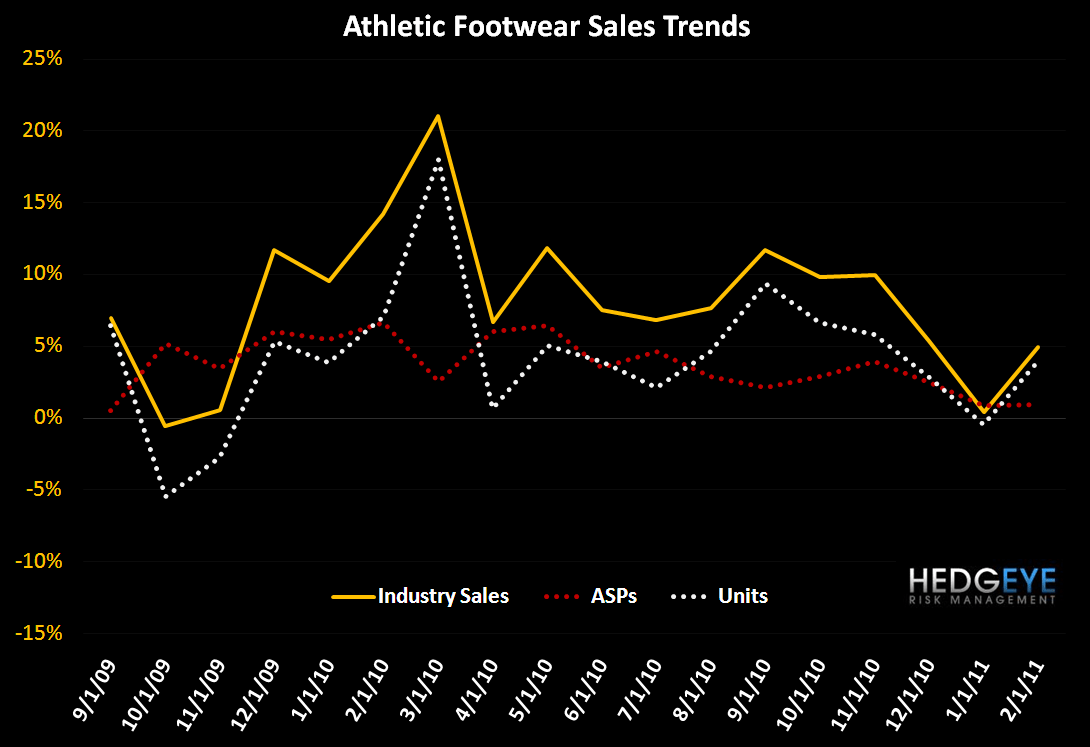

First off, NPD data shows that we’re ‘comping the comp’ with +5% growth this February versus +14% a year earlier. Average price point was up +1% for the second consecutive month. Not huge, but more often than not this metric tracks the Gross Margin trends in the space.

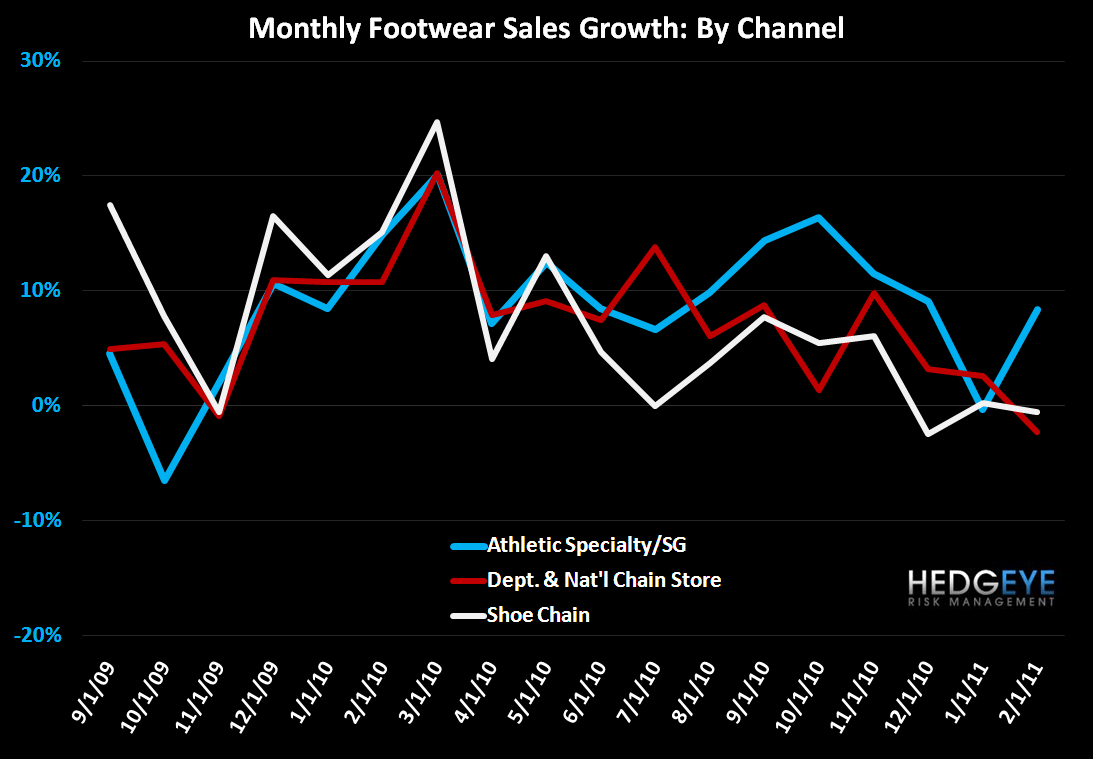

The Athletic Specialty space continues to outperform, which definitely synch with recent results out of Dick’s, Foot Locker, etc… The Family Channel looks good as well, holding steady from recent months. The channel that disappointed was the department stores, which is not a big shocker, and does not concern us. Actually, any weakness in footwear in department stores will only add to the margin pressure we should see as it relates to our call on Apparel for a 4.5pt industrywide margin decline.

Some nuggets out of Brown Shoe (BWS) and DSW:

BWS: This company is pretty much a disaster. Let’s not mistake it as a proxy for PSS – or anything else for that matter. Its wholesale business did not look good, which doesn’t shock us. Famous came in at +4.9% and sequentially unchanged on a 2-year basis, and 1Q comp guidance looks beatable at +low-msd.

DSW: This one had a rather solid quarter, but its guidance suggests a 1,000bp erosion in 1Qcomps. Are they up against some wicked y/y compares? Yes. Do they plan on beating expectations? Yes. But you can’t go guiding to comps like this and expect to walk away squeaky clean.

One thing to note is that it was about a year ago where we saw a 5-6 point negative diversion in comps at PSS vs BWS, DSW, and SCVL. Yes, this also led to PSS getting completely clocked (a painful day for us, a vindicator for the perma-bears, and an opportunity for the opportunist to buy on the capitulation). The point is that we’re about to comp up against those quarters. This is at a point where PSS’ has a better sourced-ratio, and has more boots, toning footwear, and believe it or not, higher prices. We’re not making a bull call on Payless, as we simply like the stability of its cash flow to fund growth in other brands. But let’s not be ignorant or wishful. The stock is going to trade on outsized changes in performances at Payless.