“The world is full of so-called economists who are full of schemes for getting something for nothing.”

-Henry Hazlitt

Today you’ll hear a lot of excuse making. You’ll see a lot of finger pointing. The easiest thing to do will be huddling in the comfort of crowds that will tell you “nobody saw this coming.” While taking brokerage fees on that kind of advice may be convenient, that’s not a risk management process.

There will be no accountability from the Keynesians who have advised the Japanese to “print lots of money” (Paul Krugman). There will be no causality in the analysis. But there will still be an island economy that has levered itself up with 998 TRILLION Yen in leverage – that risk management compromise and the horror of this natural disaster will be something the Japanese citizenry will have to bear for a long time to come.

Of course our hearts and prayers go out to the Japanese, but we aren’t going to use their crisis as a crutch. It’s time to remind people that chasing US, European, or Japanese stock market returns for the sake of relative performance comes with major event risk. From deficit and debt spending to The Inflation born out of printing money from the heavens, getting Something For Nothing isn’t a perpetual return.

The Japanese stock market has lost -17% of its value in 2 trading days (biggest drop since 1987). If you go back to the week that fund flows into “Developed” Equity Markets peaked (the week of February 14th – see my Early Look titled “The Flows”), the Nikkei is down -20.7%. That’s called a crash.

Like America’s, the Debt/GDP crisis in Japan is obvious. In hopes of getting Something For Nothing, the Big Government Intervention bureaucrats of Japan have already jacked up sovereign debt to 210% of GDP – and that’s not including the projected 15 TRILLION in emergency stimulus they’ve already approved to spend on this disaster.

There comes a point in an economy’s money printing and leverage-cycle that disaster (including war) can no longer be financed with Fiat Fool paper. As we rightful grieve for the Japanese people this morning, this is a major structural consideration that the 112th Congress of the United States of America should consider when politicking about the risk/reward in raising America’s Debt Ceiling.

In the US, we’ve been calling for a 3-6% correction in US Equities since fund flows peaked in mid-February. As of yesterday’s SP500 closing price of 1296, we’ve already registered -3.5% of that. This morning we’ll see our Drawdown Line of 1271 tested on the downside (see my intraday risk management note from yesterday titled “Drawdown: SP500 Levels, Refreshed”).

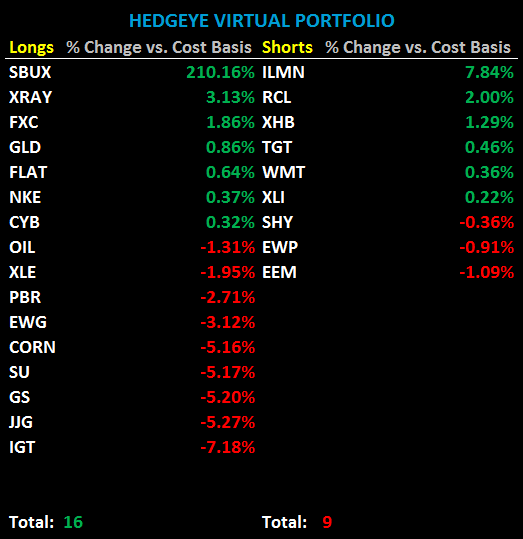

This is not to take a victory lap. I am long German Equities this morning and I am getting clocked in that position just as cleanly as you’ll get clocked in your long positions. This is a reminder however that having a large asset allocation to CASH is king if you proactively prepare for globally interconnected storms.

Yesterday I raised my allocation to CASH in the Hedgeye Asset Allocation Model to 49% from 43%. I sold down my US Equity allocation from 6% to 3% and I cut my exposure to Commodities from 15% to 12%. Again, not a victory lap – this is simply what I did.

What a lot of other people did is what they have been doing since US and Japanese Equities broke out to the upside in December – buy-the-dip. They’ll be accountable justifying that strategy with “valuation” this morning inasmuch as I will be to mine. That’s what makes a market.

Without a Global Macro risk management process this morning, I don’t know what price momentum traders are going to do – but I do know what I am going to do – and really, that’s all I care about. So here are my risk management lines and a plan:

1. ASIA

A) Japan’s Nikkei225 Index long-term TAIL line of support (10,219) is now broken, so we’re not buying that.

B) India, South Korea, Indonesia, Thailand, Singapore, etc. have been seeing Growth Slowing As Inflation Accelerates since November, so we’re not buying those either.

C) China outperformed most of Asia last night and looks most interesting to us on the long side, if only because we have been bearish on that market for the last year and there’s a mean reversion opportunity on the upside. The immediate-term TRADE line of support for the Shanghai Composite of 2851 held.

2. EUROPE

A) Germany’s DAX broke its intermediate-term TREND line of support of 7012 this morning – that’s bad and I need to take down exposure to that market no matter how bullish the fundamentals have been for the last year. Fundamentals change.

B) Britain’s FTSE and France’s CAC also broke their intermediate-term TREND lines of support of 5918 and 3959, respectively this morning. Another way to hedge my long Germany exposure will be to short one of these markets on the next bounce.

C) Spain (which I am short in the Hedgeye Portfolio) looks worse than the DAX, FTSE, and CAC as it has more price performance chasers long of it with a hope that Piling Debt-Upon-Debt is going to end well. Sorry leverage folks. This time is not different.

3. USA

A) SP500, Nasdaq, and Russell2000 all broke their immediate-term TRADE lines of support last week and 7 of 9 S&P Sectors are already broken as well. That’s not going to be new this morning, so don’t let an excuse maker tell you otherwise.

B) SP500’s critical line of drawdown support = 1271, so watch that line very closely in the coming days. Almost all of Asia and Europe have broken their intermediate-term TREND lines, so the call to “buy-the-dip” would imply that the US “decouples” from Global Growth Slowing, which you know we disagree with. US GDP growth estimates need to come down to where the market is pricing them.

C) Volatility (VIX) is threatening a long-term TAIL breakout above the 22.03 line this morning. That’s not a line that you get paid to mess with, and I suggest you respect the inverse relationship between the SP500 line of 1271 and VIX 22.03, acutely.

No one in New Haven said there was such a thing as a Big Government free lunch. No one here is going to beg for Something For Nothing this morning either. It’s time to get serious about fiscal and monetary policy. It’s time to strengthen the US Dollar so that we can tone down The Inflation. It’s time for risk management.

My immediate-term support and resistance lines for WTI crude oil are $95.43 and $103.52, respectively. My immediate-term support and resistance lines for the SP500 are 1271 and 1312, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer